Total spending grew 0.9% in June.

On a quiet day on the markets (due to Martin Luther King Day in the US) the main focus has been, again on Brexit.

https://soundcloud.com/user-291029717/stalemate-for-brexit-and-trade-talks-imf-reduces-forecasts-again

With the US out for martin Luther King Day so cash stocks and bonds both closed, and UK PM May’s ‘Plan B’ for Brexit essentially the resoundingly rejected Plan A but with an intent to go back to Brussels and try find a different solution to the Irish border conundrum, not much has happened in markets.

There’s also not much on the calendar today to excite the pulses – the German ZEW survey tonight is the pick of a sparse crop and can offer a hint of what the more important IFO survey will show on Friday and perhaps even the preliminary German PMIs on Thursday. But ZEW, remember, is just a survey of a large bunch of financial analysts – e.g., this scribe was since a survey participant in the UK – and what do we know?

Things will hot up later this week, starting with New Zealand CPI tomorrow then Australian labour market figures, the various Eurozone flash PMIs and the ECB, who are due to publish new forecasts as part of the first gathering of the year for the Governing Council.

Overnight the IMF has downgraded its global growth forecasts for the second time in three months, to 3.5% from 3.7% last October. Downgrades within the Eurozone, to France and Italy but more significantly Germany – Europe’s ‘growth engine’ – and by a chunky 0.6%, are largely responsible for the downgrade, as too Turkey in the Emerging Markets universe.

As well as the downgrade, the IMF sees the balance of risks to its outlook skewed to the downside, citing trade tariffs, a renewed tightening of financial conditions, a “no deal” Brexit and a deeper-than-anticipated slowdown in China.

Frankly, all factors which could look a lot less troublesome in the coming few months if for example, the US and China strike a trade deal, equity markets maintain the gains seen since late December (so easing financial conditions) Article 50 gets extended for the UK (highly likely) and the nascent signs of a China growth pick up evident in yesterday’s December activity readings, prove sustainable.

Against this glass half full interpretation of developments, US stock market fortunes took a small hit during our day yesterday on reports that the US trade representative had briefed US lawmakers on the lack of progress on the issue of alleged theft of Intellectual property China (who of course deny it occurs and demand proof).

Also noteworthy are reports, courtesy of the Xinhua newsagency, that President Xi Jinping yesterday warned China top leaders that the party is facing “sharp and serious dangers of a slackness in spirit, lack of ability, distance from the people, and being passive and corrupt,”. It notes that while such warnings aren’t new, the mention of “serious” threats to the party’s “long-standing rule” appeared to be.

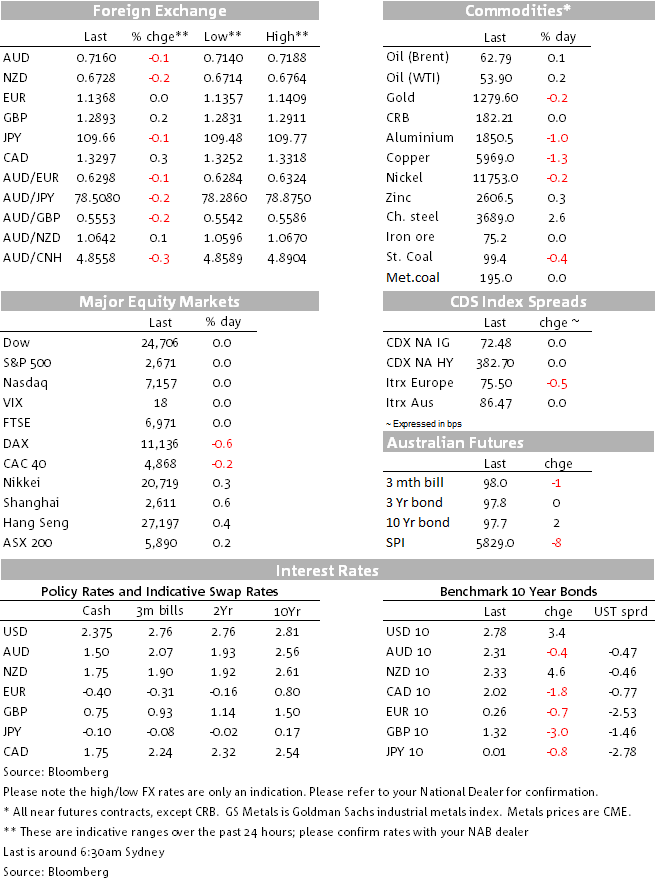

Not much movement to note in FX markets even though they didn’t enjoy the luxury of the MLK Day holiday. AUD/USD sits a little lower than where we left it yesterday at just below 0.7160. It made an overnight low of 0.7140, its weakest since 9th January and the bottom edge of what some technical analysts are regarding and an important support zone. Thursday’s labour force survey will be an important fundamental test now (and too to some extent tomorrow’s NZ CPI figures, where significant softness would be seen as likely to translate through to next week’s Austrian Q3 numbers).

CAD and NZD are both weaker in the last 24 hours though NZD is, at 0.6727, up on where we left it yesterday. SEK, followed by GBP, are at the top, albeit barely 0.1% stronger than Friday night’s NY close. GBP has been helped by ongoing optimism that a hard Brexit will be avoided on 29th March.

In this respect, a group of cross-party lawmakers, including members of PM May’s Conservative Party and the opposition Labour Party, have just proposes a bill to force PM May to delay Brexit if agreement can’t be reached in Parliament by Feb. 26. There’s a good chance this gets up. If so, it further flattens the tail risk of a hard Brexit on March 29, though note all 27 EU nations will need to agree to an extension, so it wouldn’t eliminate the risk completely.

The US Cash Bond market has been shut though bond futures prices are a touch higher consistent with slightly weaker stock futures. In Europe, both Bunds and Gilts have rallied; Bund yields some 0.7bp lower and gilts a bigger 2.9bps at 10 years.

European equities finished lower, the Eurostoxx 50 by 0.3% led by a 0.6% drop in the German Dax, while the FTSE was flat. S&P futures are off about 0.3% and the NASDAQ by 0.5%

Commodity prices are mixed with oil up 10 cents or so but copper and aluminium both off by just over 1%. Iron ore futures are flat and gold $2 lower.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.