Online retail sales growth slowed in May following a fairly strong April

Insight

There's rising hopes that a US fiscal stimulus deal is imminent.

https://soundcloud.com/user-291029717/imminent-fiscal-deal-a-narrow-path-to-brexit-and-a-fed-waiting?in=user-291029717/sets/the-morning-call

I believe, I believe, In progress, in progress – Public Service Broadcasting (from a concept album about the progress and decline of the Welsh coal mining industry, in case you wondered. It doesn’t feature near the top of my Greatest Hits Spotify playlist)

The Fed has just delivered its final policy statement of 2020 where as well as keeping the policy target rate unchanged at 0-0.25% says that ‘The Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage-backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee’s maximum employment and price stability goals’.

The tweak from prior statements is the inclusion of ‘substantial further progress’ which is the widely anticipated nod toward outcome-based guidance regarding the longevity of its QE bond buying programme.

The median Fed ‘dot’ for the anticipated Fed Funds rate target remains at 0.125% through 2023.

What hasn’t happened today (and which was also in line with consensus) is that there is no decision to skew its bond purchases towards longer-dated maturities.

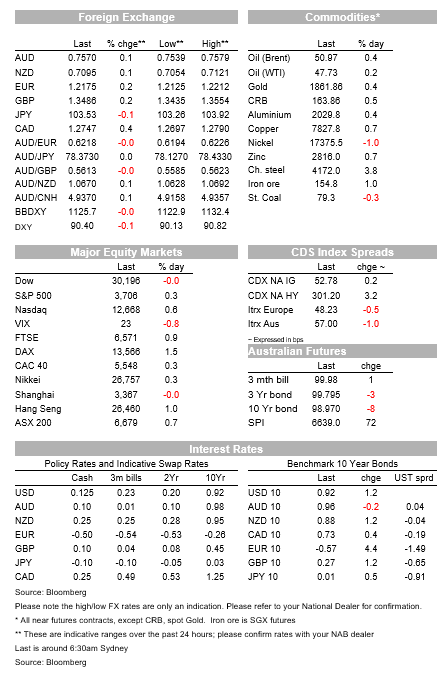

A decent minorly of market participants expected them to announce something on this as early as today, hence the knee-jerk 3bp rise in 10-year US Treasury yields, blip up in the USD (+0.3% in the DXY index) and quarter percent drop in the S&P500 versus pre-announcement levels..

Pre-Fed and as far as the big drivers of sentiment in the past couple of days go, yesterday we noted the ‘buzz’ around Westminster that an agreement on a post-Brexit trade dal was close.

The buzz in Washington now is that US lawmakers are on the verge of agreeing to a fiscal stimulus package that excludes the most contentious issues, but which still in the order of $900b (not the ~750bn doing the rounds yesterday.

The deal would reportedly include stimulus payments to individuals (around $600-$700 each) and supplemental unemployment insurance (around $300), while excluding the two most contention issues of direct aid to state and local governments and liability protections for businesses. We might have some formal announcement in coming hours.

Sources point to some resolution of the “level playing field” issue, with the UK accepting the idea of “managed divergence”, or increasing its standards on welfare and labour if and when the EU does so in the future.

EC President von der Leyen said that fishing rights were now the last major hurdle to a trade deal.

We remain optimistic that a deal will be reached, as evidently does the foreign exchange market where GBP/USD made a new post-May 2018 high of $1.3550 or thereabouts but has since peeled back a cent or so, only in part on the knee jerk USD gains on the Fed statement.

The EUR received a decent boost, EUR/USD popping above 1.32, on much better than expected Eurozone PMI number from France, Germany and then pan Eurozone, the latter printing 55.5 for manufacturing up from 53.8 (53.0 expected) and services 47.3 from 41.7 and 42 expected (so services still contracting as you would expect given lockdowns, but at a much slower pace than prior months).

German manufacturing at 58.6 from 57.8 (56.5 expected) was its highest since mid-2018, driving by surging export orders and where China’s ongoing strong recovery, evidenced in Tuesday’s activity readings, plays a very large part. Even France’s manufacturing sector was back in expansionary mode at 51.1 from 49.6.

But by less than expected in services. Services activity up to 49.9 from 47.6 against 50.7 expected.

Manufacturing activity jumped to 57.3 from 55.6 and versus 56.0 forecast. .

But should they really have been given the inevitable impact on restaurant and bars, and clothing sales, from the tighter social distancing restrictions across many states?

Headline sales fell by 1.1% much worse than the 0.1% rise expected, weakness led by a 4% fall in food service sales and clothing (‘apparel’) down by an even bigger 6.8%.

Sales ex-autos fell by 0.9% also against 0.1% expected.

The Control Group which excludes some of these very weak items, was down 0.5% against +0.2% forecast.

With less than an hour of NYSE trade to go the Dow and S&P 500 are both about flat and the NASDAQ +0.6%. Earlier European bourses finished mostly in the green, led by a 1.5% rise for the Gran DAX.

10-year US Treasuries have already given back half of their knee jerk rise but are still +2bp up on the night at 0.93%.

European bonds were all higher by between one and five basis points, Germany’s 10-year Bund 4.4bps higher at -0.57% and following their stronger than expected PMI numbers.

It’s been a very mixed performance for G10 currencies, with NOK currently leading gains (+0.3%) amid further (modest) gains in oil prices, with GBP back from its $1.3559 highs to $1.3480 now but still +0.15% up on the day.

CAD is the weakest at -0.4% and continuing to lag AUD and NZD on the commodity currency front. Incidentally Canada November CPI came in at 1.7% much as expected by way of averaging the three core measures.

AUD and NZD have not seen much action since we went home, both currently little changed on Tuesday’s NY close at 0.7568 and 0.7093 respectively, the kiwi finding the air above 0.71 thin (its back from a high of 0.7120).

Note the Swiss France is slightly weaker despite the US formally labelling Switzerland as a “currency manipulator” for the first time in the latest Treasury foreign exchange report. With a forthcoming change in Treasury secretary under the Biden Administration, the report has little implication. The Swiss National Bank swiftly denied the label. The only real surprise is that it is taken this long for the US Treasury to label the country as a currency manipulator, as it has been actively buying foreign currency for years to hold back appreciation of CHF.

Bitcoin is still on its latest tear, up nearly 7% to $20,762. I still don’t want one for Christmas.

For NZ GDP (08:45 AEDT) our BNZ colleagues anticipate a rebound of 14.0% (RBNZ +13.4%) after the fall of 12.2% in Q2.

For AU Employment, we expect another strong set of numbers given Victoria’s re-opening and JobSeeker numbers falling sharply over mid October to mid-November. NAB looks for employment of +30k and unemployment unchanged at 7.0% (consensus is similar at +40k and 7.0% unemployment).

Today’s MYEFO to be delivered by Treasurer Frydenberg is expected to show the budget looking better given the sharp rebound in activity and a record high iron ore spot price.

Internationally, the Bank of England meets for the last time in 2020 and is expected to leave its key policy measures unchanged. Any commentary related to the likelihood or otherwise of negative rates next year will be one point of interest.

Data wise, there are no top tier releases scheduled (US Housing Starts and Philly and Kansas Fed manufacturing surveys the pick of the crop).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.