Online retail sales growth slowed in May following a fairly strong April

Insight

Friday’s non-farm payrolls numbers in the US surprised on the downside.

https://soundcloud.com/user-291029717/inflation-debate-over-bidens-stimulus-as-jobs-growth-disappoints?in=user-291029717/sets/the-morning-call

Weekend News

Coming Up

Future uncertain but certainly slight…The devil inside – INXS

When bad news is good news. Friday’s US labour market update disappointed with details in the report painting an even grimmer picture. President Biden noted the report highlighted the risk of doing “too little”, reaffirming his commitment to get a big stimulus done with or without Republican support. US equities closed modestly higher, encouraged by the idea of more fiscal spending. The UST curve steepened a little bit more with an uptick on inflation expectations driving the move up in longer dated yields. The USD was broadly weaker, the AUD ended the week close to its overnight high and the euro climbed back above 1.20.

January payrolls rose 49k, below the consensus for a 105k print meanwhile the December print was downwardly revised to 227k from -140k previously. The unemployment rate unexpectedly fell to 6.3% from 6.7%, well below the consensus for an unchanged outcome, but this was not good news given the decline was largely explained by a pullback in the participation rate (-0.1% to 61.4%), meaning about 405kk of workers left the market, a sign of discouragement. The move up in average weekly working hours to 35 from 34.7 was a positive. Its highest reading since 2006, suggesting some evidence of tightening pressure as those who are employed are working more hours.

Reacting to the US Labour market update, President Biden noted the report confirmed the necessity for the government to do more. “I believe the American people are looking right now to their government for help … so I’m going to act fast,” he said in a White House speech. While still calling for bipartisan support, the President said that “What Republicans have proposed is either to do nothing or not enough.” Adding that the stimulus will get done with or without Republican support.

On this last point, both chambers of US Congress on Friday passed a budget resolution and as expected the Senate voted along party lines, resulting in a 50-50 tie. Vice President Kamala Harris added her the decisive vote to make it 51-50. The passing of the resolution sets the wheel in motion for Democrats to get their fiscal stimulus plan approved without Republican support. House speaker Pelosi said her chamber will begin working on Monday on stimulus bills and “hopefully” send them to Senate in two weeks.

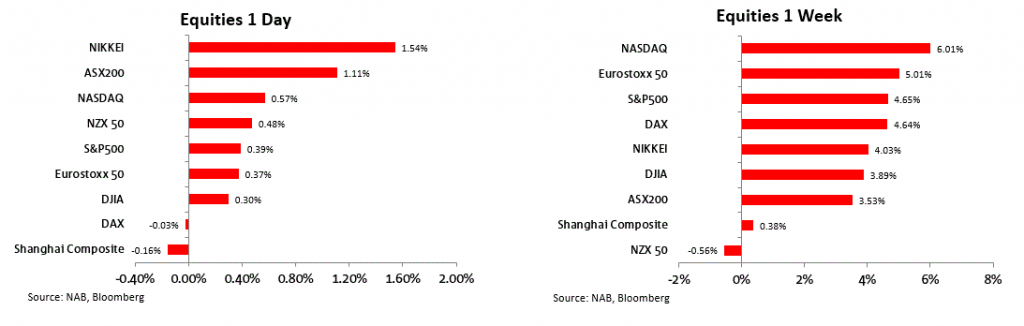

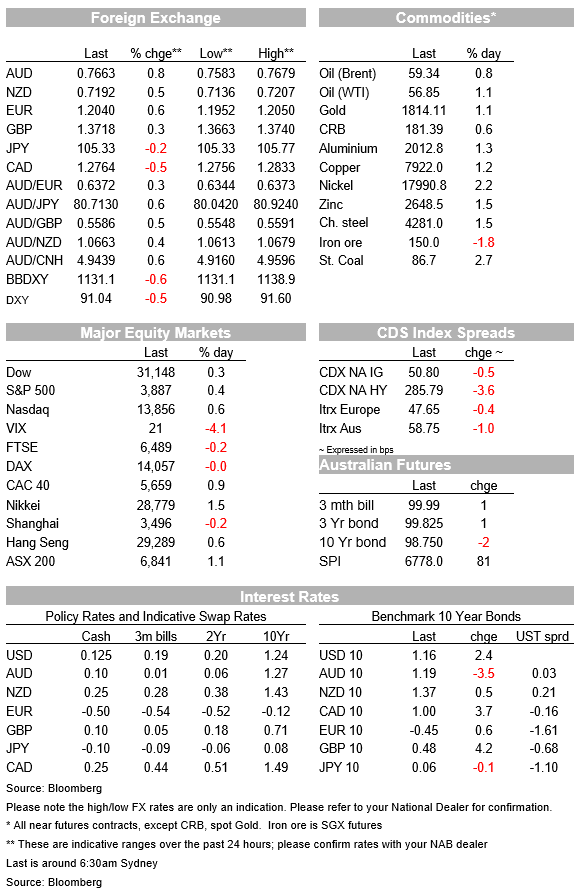

US equities managed to close Friday with modest gains. The S&P 500 closed up 0.4%, the Nasdaq gained 0.6% and the Dow added 92 points, climbing 0.3%. Looking at S&P 500 the in more detail, all sectors ended the day in the green with IT the one exception Semiconductor Equipment the big underperformers, down 0.9%. Looking at the week, it was an impressive one for US equities, all five days recorded gains and it was the best performing week since early November (S&P 500 +4.65% and NASDAAQ 6.01%). Solid company earnings reports were one driver for the gains in equities while rising hopes of a new big US fiscal stimulus was another. European equities were not far behind, also recording gains close to 5%, our FTSE/ASX 200 climbed 3.53% while China Shanghai Composite and NZX 50 were little changed.

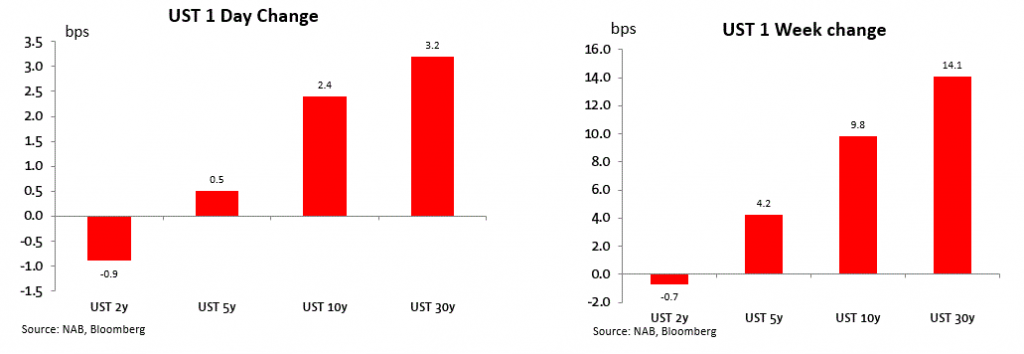

The 2y tenor closed 0.9bps lower, matching its all time low of 0.1013% while longer dated maturities edged a little bit higher continuing the recent steepening of the curve. The 10y UST note closed the week 1.164%, up 2.4bps while the 30y bond ended at 1.971% , 4,2bps higher. On the week the 10y tenor climbed 10bps while the 30y gained 14bps and the 5y30y curve moved above the 150bps mark for the first time since 2015.

Looking at the breakdown between nominal and real yields, the move up in both 10y and 30y UST yields is largely explained by an increase in inflation expectations, reflecting investors concerns over the mid to long term impact from the prospects of an uber- expansionary fiscal policy. 10y US breakevens closed the week at 2.1987%, its highest level since May 2018.

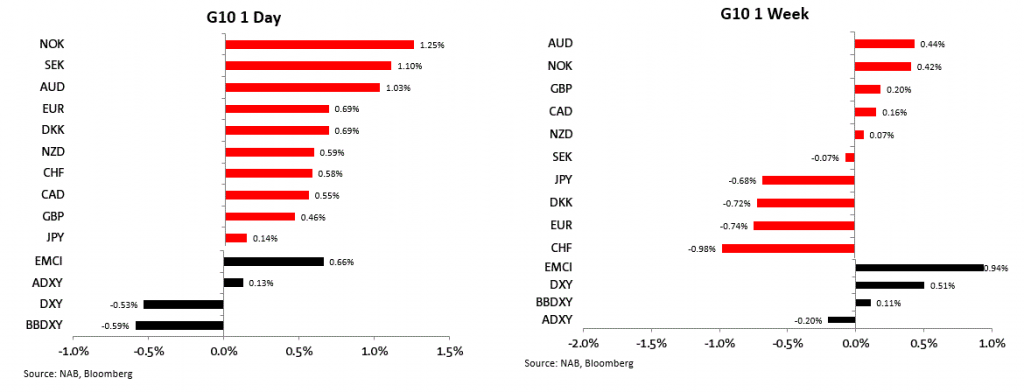

The big news from Friday was the impressive U turn in USD fortunes. The USD has been on a steady rise since around January 22 with its outperformance largely attributed to the expectations of the US economy performing better than others (ex China and especially Europe) at this stage of the recovery. Vaccine roll out and better economic data supporting this notion.

Friday’s underwhelming non farm payrolls report challenged this notion while the inflationary aspect of a super charge US fiscal plan also played a part on the USD pullback. BBDXY fell 0.59% while DXY was -0.53%. Looking at the week USD indices still managed to record gains for the week, so may be is a bit early to suggest the greenback is now on a new decline.

The flip side of the USD ‘s underperformance was reflected by decent gains for other currencies across the board. NOK SEK and AUD gained over 1% with the AUD ending the week at 0.7678, close to its overnight and weekly high. After a wobble at the open, the AUD now appears to be setting at around 0.7660.

NZD also had a good Friday, gaining 0.59% and briefly trading back above the 72c mark. The kiwi has started the new week at 0.7193. The euro was the other notable mover, gaining 0.70% and now trading back above the 1.20 mark, although the pair still lost 0.74% against the USD on the week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.