Coming in for landing in a heavy cross wind

Insight

There’s a risk that next week’s US election is more contestable than we might have considered a week ago.

https://soundcloud.com/user-291029717/is-the-biden-trump-gap-closing?in=user-291029717/sets/the-morning-call

“You better knock, knock on wood, baby; Baby; I’m not superstitious about ya; But I can’t take no chance; You got me spinnin’, baby; You know I’m in a trance”, Amii Stewart 1979

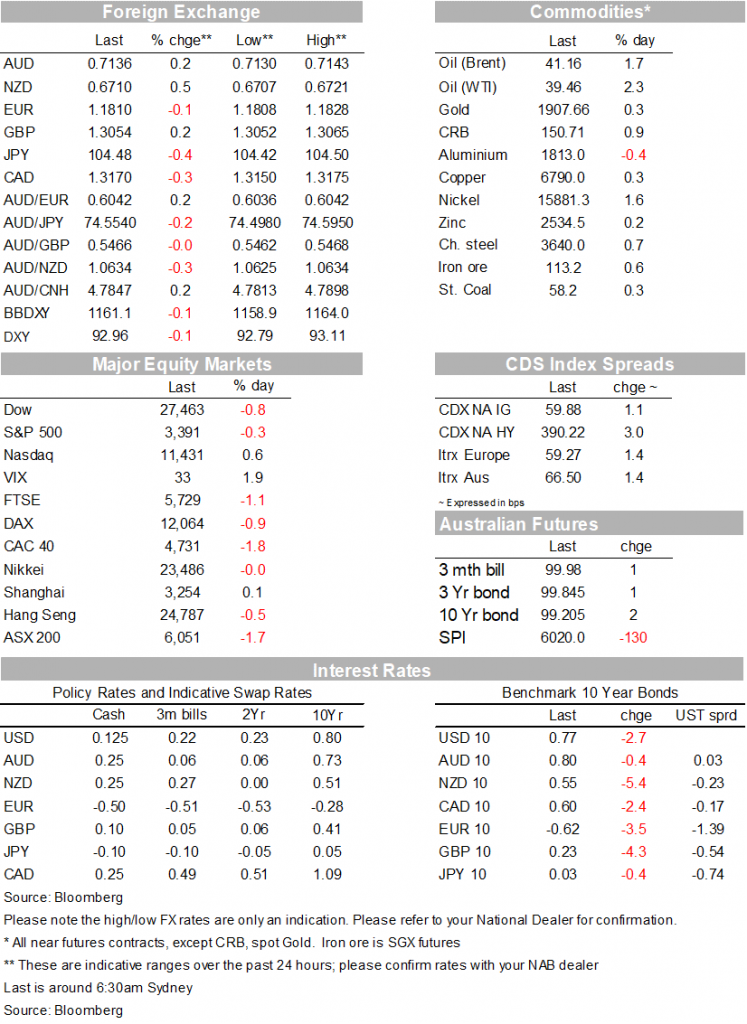

Markets remain in a cautious mood given rising hospitalisation rates may require tougher restrictions to contain the spread of COVID-19 and ensure hospitals do not become overwhelmed. CNBC notes in the US, hospitalisation due to COVID-19 rose 5% over the past seven days and curfews and restrictions have been declared in parts of Illinois and Texas. Vaccine hopes though remain with Pfizer noting results from its trials are now likely after the election. As for fiscal stimulus, hopes have faded this side of November so the focus on those hopes rests to after the election. Some 60m Americans have already cast their vote, though a few commenters are noting a late polling surge for Trump which could create the potential for a contested election.

US tech outperformance though has meant a less dramatic decline in the US equities with the S&P500 down -0.3% (after yesterday’s -1.9%) compared to -1.2% for the Eurostoxx50. Note the S&P500 IT sub-index rose 0.5% compared to a -2.2% for the Industrials sub-index. Microsoft reporting at the close beat expectations at 1.82 a share v. 1.54 with shares up 1% in extended trade. The caution tone was also seen in rates markets with yields lower across the board. The US 10yr yield fell -2.7bps to 0.77%.

US data ahead of Q3 GDP on Thursday was mostly stronger than expected. Core Capital Orders rose 1.0% m/m v. 0.5% expected with the level of orders now some 3.3% above pre-COVID trends. Core Durable Goods Orders also beat at 0.8% m/m v 0.4% expected. Partly on the back of that data the Atlanta Fed’s GDPNow tracker was revised higher to 36.2% annualised, which if realised would be a remarkable bounce from Q2’s -31.4%. Also out overnight was the Richmond Fed Manufacturing Index (29 v. 18 expected) with firms reporting improving conditions and growing order backlogs. Interestingly firms said they struggled to find workers with necessary skills. Consumer confidence figures were the exception to the data beats, with the conference board measure at 100.9 v 102.0 expected.

It was a story of USD weakness with the DXY -0.2%. There were signs of cautiousness with USD/YEN -0.4%, so the USD weakness story appears to be secular. In recent days a number of asset managers have stated their view of a secular decline in the USD with BlackRock the latest saying they see 1-3 years of moderate dollar weakness based on expectations of unprecedented fiscal and monetary stimulus regardless of who wins the US election.

Meanwhile the NZD continues to show puzzling resilience amidst the deteriorating global backdrop with NZD +0.5% and best performing G10 excluding Scandinavian currencies. A higher oil price has no doubt helped commodity linked currencies a little with the AUD +0.2% and USD/CAD -0.3%. As for oil, Brent is up 1.7% on the back of the weaker USD and as Topical storm Zeta approaches the US gulf with producers shutting down almost half of their output – landfall is expected in Louisiana on late Wednesday.

Finally in Europe and ahead of the ECB on Thursday, it appears credit conditions are tightening. The ECB’s quarterly survey of banks showed a tightening of credit standards on loans to firms in Q3: “indicating credit risk considerations due to the coronavirus pandemic”. That may suggest the need for further stimulus which NAB expects in December. The Euro though was little moved, down just 0.1%.

Q3 CPI figures would normally dominate markets, but given the RBA’s explicit forward guidance, it is unlikely to be as market moving as previously. Offshore it is very quiet with only US Trade Balance/Inventories scheduled, while the Bank of Canada meets with no change expected. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.