Price growth edges lower despite reasonable economy

Insight

Equities were boosted overnight by the positive (temporary) deal between the US and China.

https://soundcloud.com/user-291029717/is-us-china-deal-euphoria-hiding-the-real-picture

I can feel it coming in the air tonight, oh Lord – Phil Collins

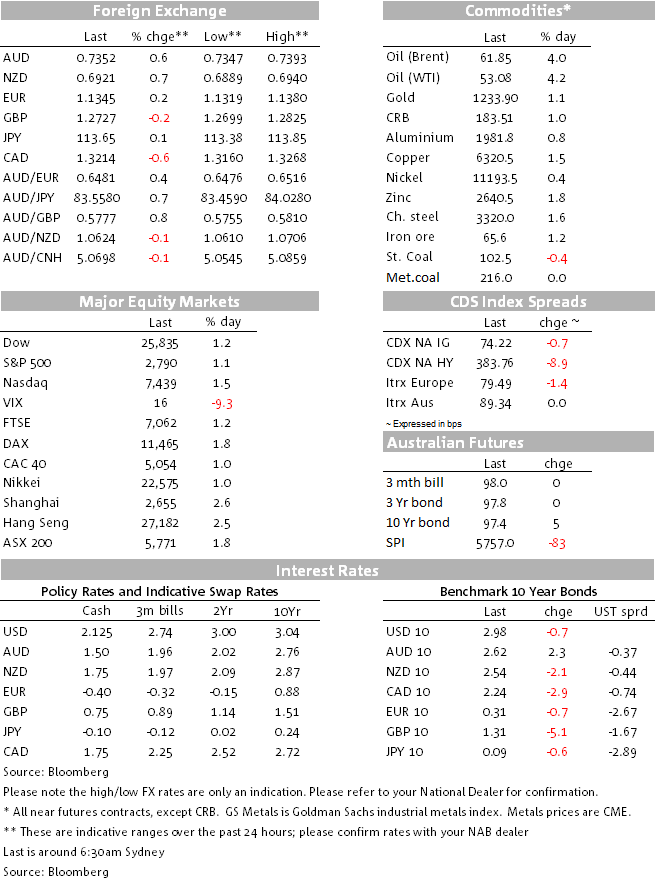

The market has hold on to early gains from the US-China trade armistice. All major equity markets have started the new week with positive returns, risk sensitive currencies are higher and gains in commodities have been led by higher oil prices. Looking at the intraday charts, however, initial gains faded as the night went by reflecting a sense of cautiousness given lack of details from the ceasefire agreement and conflicting reports. The ISM manufacturing shot the lights out and even though prices paid ease, policy sensitive front end UST yields rose, flattening the curve.

After yesterday’s tweet by President Trump announcing that China had agreed to “reduce and remove” tariffs on American-made vehicles. Overnight US Treasury Steven Mnuchin confirmed China has agreed to eliminate tariffs on imported automobiles but failed to give details. A few hours later in a Briefing, China’s foreign ministry spokesman Geng Shuang declined to comment on any car tariff changes, leaving the market wondering if car tariffs are part of a broader deal. This morning Trump’s Economic Adviser Lawrence Kudlow said he was ‘cautiously optimistic’ about progress in trade talks with China and the US President named US Trade Representative Lighthizer to head trade negotiations, who is a known hard-liner that has been pressing for more tariffs against China. Worth noting too that officially China has not acknowledged the conditionality of the trade truce, the 90 day deadline has also been omitted. So overall trade news overnight have probably left the market with more questions than answers, can the US and China really resolve their differences in 90 days? It seems that more details and signs of progress will be needed if the initial trade truce warm fuzzy feeling is to be sustained.

Relative to yesterday’s opening levels the USD is weaker against most currencies with the improvement in risk appetite the main factor at play. GBP is one exception a tad weaker after erasing early gains amid more Brexit developments. That said as noted in previous commentary, USD indices are still hovering very close to their year to date highs. DXY now trades at 97.02 and BBDXY is at 1206.18.

Risk sensitive and commodity linked currencies have led the gains against the USD with NOK (0.97%), SEK (0.91%), NZD (0.84% ), CAD (0.77%) and AUD (0.71%), leading the gains in G10. CNY has also been a key beneficiary of the trade war ceasefire with USD/CNY down more than 1% to 6.8830.

Looking at the AUD in more detail, the pair traded to an overnight high of 0.7391 early in the session, but as US-China trade news raised some questions and equity markets faded, the AUD gave back some of its early gains and now trades at 0.7350. Yesterday, the AUD also struggled to retain early gains with domestic data releases printing on the softer side of expectations. Housing market indicators continue to slow in November and Q3 GDP partials came out softer than expected, pointing to downside risks to Q3 GDP on Wednesday. Inventories were flat in the month against expectations of a +0.4% rise, meaning inventories will likely subtract around -0.26%points from quarterly GDP growth and company profits rose 1.9% q/q (weaker than the 2.8% consensus).

The NZD has not only hold on to the initial gains recorded at yesterday’s open, overnight the pair managed to edge up a little bit more, although gains have eased a little in the past couple of hours. The kwi traded to an overnight high of 0.6940 and now trades at 0.6920. Jason Wong, our BNZ market Strategist, is cautious in predicting a further strong rally in the NZD after the 5½% gain in November and Monday’s gains, with BNZ’s short-term fair value estimate is currently sitting just below 0.67. Jason notes the NZD has moved from very cheap to moderately expensive in a very short space of time and is now overdue for a period of consolidation.

Amongst the other majors, JPY is flat against the USD with USD/JPY at ¥113.68 while GBP/USD is a bit softer (-0.1%) at 1.2724. The UK Attorney General confirmed that Britain will not be able to cancel the Irish backstop clause without approval from the EU, as he gave legal advice to MPs May’s Brexit deal. EUR is up 0.3% to 1.1350, perhaps supported by incrementally positive news on the Italian budget standoff with the EU, although mixed PMI result didn’t help the union currency (more below)

The US ISM manufacturing beat expectations with domestic new orders more than offsetting the decline in export demand. That said and perhaps more importantly for the market, the prices paid index fell by 11 points to 60.7, to be now slightly above its 20y average. Overall the data supports the notion that US inflationary pressures are easing, in line with the sharp falls in the oil price and the recent rise in the US dollar and thus the Fed can afford to be patient.

The ISM did not elicit a material reaction on the USD, however policy sensitive shorter dated UST yields rose after the data release, suggesting the market paid more attention to the rise in the headline numbers rather than the decline in prices. The 2y rate ended the day 4.1bps higher at 2.837% while the 10y rate is essentially unchanged relative to yesterday’s opening level at 2.989%. 10y UST yields traded to an early overnight high of 3.0498%, but with oil prices easing, trade uncertainty rising and a decline in ISM prices, the tenor embarked on a steady decline erasing all the gains for the day.

Italy’s 10-year rate fell to a 2-month low, declining 6.7bps to 3.14% with one paper reporting that PM Conte is convincing Salvini and Maio to lower the deficit to meet EU demands. Data releases probably also paid a part with Italy’s PMI falling to 48.6 and the weakest read since April 2013.

The S&P500 opened up 1.4% higher, but gains has since been pared down to 1.09%. The Dow (+1.20%) and NASDAQ (1.39%) also look set to start the week on a positive note and early in the session all major European indices closed in positive territory with the STX Europe 600 closing at 1.03%.

Oil prices opened stronger and Brent crude was up as much as 6.6% at $62.60 at one stage, before paring gains to 5.3%, now trading at $61.93. In addition to the trade truce improvement in risk sentiment, the “high 5” that Putin and the Saudi Crown Prince gave each other was seen as a sign of cooperation that OPEC and friends.The two countries agreed to extend into 2019 their deal to manage the market, although neither have yet to confirm any fresh output cuts.

Other commodities have started the week with gains, albeit not quite to the same degree as oil. The LMEX index is +1.27%, iron ore is 1.24% and gold is 0.90%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.