NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The markets somehow expected more from the Bank of Japan but there was swifter market reaction to news that the US and China might restart trade talks.

https://soundcloud.com/user-291029717/japans-little-tweaks-chinas-new-talks-and-canadas-closed-door

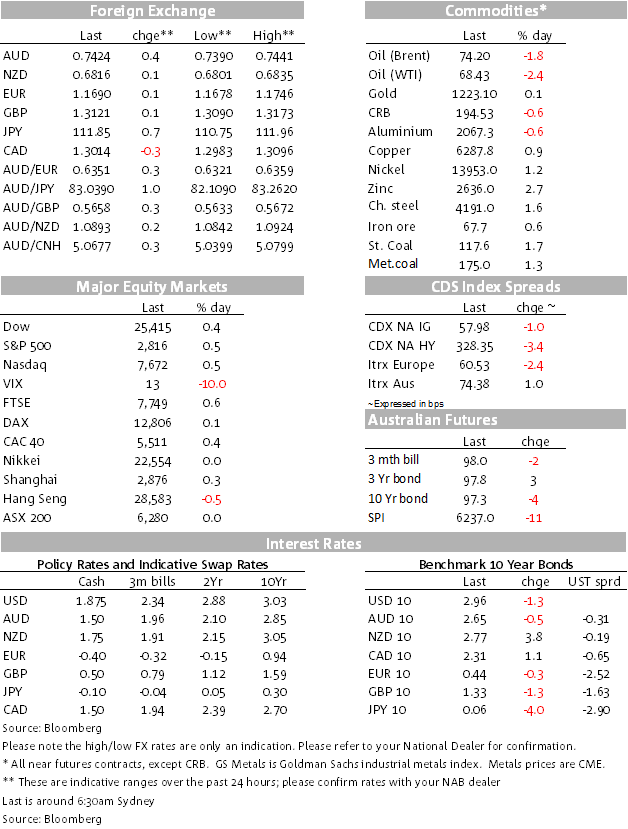

There’s been quite a lot of event and data risk over the past 24 hours both in the APAC session and overnight, and with still more on the slate. When all is said and done, the AUD/USD sits higher on net this morning, likely aided as much as anything by some press reporting that US-China trade talks are back on. In an interview with CNBC last week, US Treasury Secretary Steve Mnuchin said there were some “quiet conversations” in train, Bloomberg reporting that the US and China are trying to restart talks to avoid a full-blown trade war, with US Treasury Secretary Mnuchin and China’s Vice Premier Liu are having such communications. (Running against that grain in the past hour or so has been another news story suggesting not much progress, the AUD having receded a little late in the NY session from intra-day highs around 0.7440.)

Wire services are reporting the US is trying to secure certain concessions and if China agrees, it is possible the US would back off from additional tariffs. While unsourced and perhaps a little bit of smooth track in what’s been and may continue as a long and winding road, it seems to have been enough to support commodity/China exposed currencies. The NZD and the CAD appear to have also benefitted in the backwash, the Kiwi after the soft activity and confidence readings from yesterday’s ANZ Business Survey. For the CAD, it’s had some headwinds from Canada ostensibly having been locked out of the current US-Mexico NAFTA negotiations and weaker oil prices overnight. Canada’s monthly GDP for May though was stronger than expected, supporting the CAD and Canadian yields.

The data flow yesterday was mixed for the AUD, AU Building Approvals bouncing in June, Credit in line, China’s PMIs softer than expected but its Manufacturing component Steel PMI bouncing (big for iron ore and met coal especially), up from 51.6 to 54.8, indicative of a lift in momentum and suggesting the early year sag was more seasonal than enduring. The bulks commodities were higher overnight.

It was yesterday’s downgrade of the BoJ’s inflation outlook and persistence with broadly similar policy settings that on the day that was something of a catalyst supporting global bond markets over the past 24 hours.

The BoJ downgraded their inflation forecasts for the current and next two Japanese fiscal years by 0.2-0.3%, the BoJ now expecting the CPI ex fresh food (core CPI) to be 1.1% this year (-0.2% downgrade from 1.3%), up to 2.0% in F19 (-0.3%) and 2.1% for FY20 (-0.2%). That superficially is inflation at 2%, but take out the forecast impact of next year’s hike in the consumption tax and core CPI is forecast to be 1.5% in FY19 and 1.6% in FY20, still below 2%. No surprise then that BoJ Governor acknowledged that achievement of the target will be “beyond our [three-year] forecast timeframe”. The tax is scheduled to rise from 8% to 10% next October and its effect on the consumption and the economy is something the BoJ will also be watching closely (as a Japanese Government task force has been examining), also a point of emphasis in yesterday’s BoJ statements. Also for the JGB market, the BoJ stated they will be more tolerant of movements in the 10 year yield around the 0% guidance.

Speaking of inflation, the flash Eurozone CPI for July surprised on the higher side for both headline and core by a tenth, headline at 2.1% against an unchanged 2.0% expected, while core CPI rose from 0.9% to 1.1% higher than the 1.0% tipped. The first estimate of EZ GDP for Q2 showed yet another quarter of GDP growth (the 21st) if a tenth less than expected at 0.3%/2.1% after 0.4%/2.5% in Q1.

The US personal income, spending and PCE deflators report revealed a one tenth miss in annual growth of the core PCE deflator at 1.9%, the same as in June and even though monthly growth was as expected at 0.1%, down from 0.2% in June. The Employment Cost Index for Q2 also missed market expectations, up 0.6% after 0.8% in Q1 and 0.7% expected. So no killer blows to bonds from those releases. US real consumption grew another 0.3% in July and the Atlanta Fed has pegged its very early estimate of US GDP for Q3 at a tidy 4.7%. There’ll be another update tonight after the ISM Manufacturing report.

Meanwhile in a further sign of positive economic conditions, the US Consumer Confidence report was another strong reading (127.4), consumers seeing the best jobs opportunities since 2001, a further rise in the net Jobs Plentiful index. Ahead of the ISM tonight that’s expected to print at 59.3, the Chicago PMI came in at 65.5, up from 64.1. Overnight inflation and activity report add more to the case of the Fed moving ahead with the gradual rate lifting strategy, no change in rates expected from the Fed tomorrow morning. The statement though will be examined for further indications on the “for now” addition to gradual policy tightening, indications the Fed is well on the road toward a neutral Fed funds rate and likely acknowledging tariff/trade war possible disturbances.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.