Coming in for landing in a heavy cross wind

Insight

There's been a lot of employment numbers out over the last 24 hours – for the US, the UK and Australia.

https://soundcloud.com/user-291029717/jobs-jobs-jobs-and-a-european-recovery-plan?in=user-291029717/sets/the-morning-call

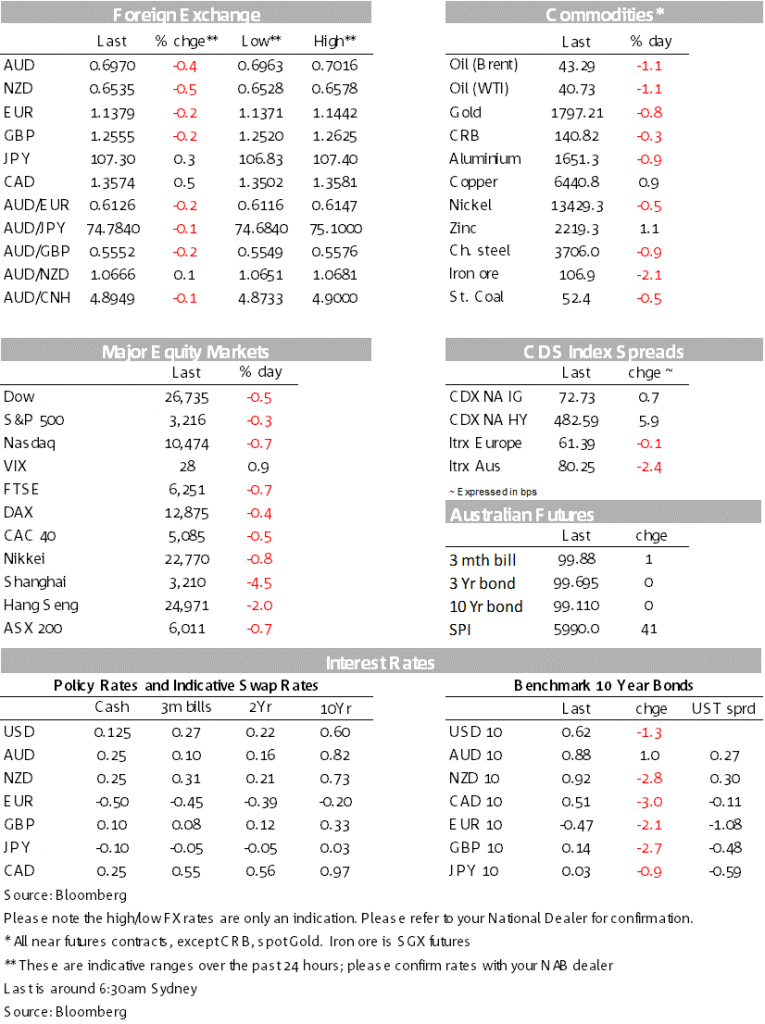

Cautious tone overall after the earlier sharp fall in Chinese equities (CSI 300 -4.8%) and miss in US Jobless Claims (1.30m v 1.25e). Netflix reported after the close and will likely reinforce the soft tone in Asia (Netflix down -9% after hours on weak Q3 subscriber guidance), while today’s focus is on the upcoming EU leaders meeting and whether an agreement on the recovery fund can be made – watch EUR. Amid the cautious tone the S&P500 fell slightly (S&P500 -0.3%), yields were largely steady (US 10yr -1.5bps to 0.62%), the USD rose (DXY +0.3%) and the AUD correspondingly fell -0.4% to 0.6971.

“Once I ran to you; Now I’ll run from you; Don’t touch me please – I cannot stand the way you tease; I love you though you hurt me so; Now I’m gonna pack my things and go”, Soft Cell 1981

“Tainted Love” spent 44 weeks in the US top 100 back in 1982 (then a record break feat). That track perfectly sums up the markets’ attitude to the Chinese activity numbers yesterday which helped drive the sharp fall in Chinese equities (CSI 300 -4.8%). Despite Chinese GDP beating expectations with activity now back to pre-COVID levels (Q2 GDP 11.5% q/q v. 9.6e), markets focused on the lack of a convincing retail rebound with retail sales still down -11.4% YTD y/y. The other factor driving Chinese equities lower over recent days has been commentary in state-owned press designed to temper optimism in the Chinese market after a sharp 22% rise since mid-June – the latest being a critical article over Moutai a large liquor maker and bellwether stock (its share price down 8%). The fall in the CSI set the weak tone overnight.

US equities fell slightly with the S&P500 -0.3%. Earnings were again mixed with little direction on net – of the major names reporting BofA -2.7%, Morgan Stanley +2.5% and J&J +0.7%. Netflix reported after the close with aftermarket trading seeing its stock down a sharp 9% and will likely provide a soft direction for Asia. Disappointing next quarter subscriber guidance was the driver (2.5m net subscriber additions are excepted for Q3 v 5.27m expected). The weak outcome by the first major tech stock to report will put the focus firmly onto the tech sector with all eyes on upcoming earnings reports from the other FAANGs.

But a miss on Jobless Claims largely dominated. US initial jobless claims disappointed at 1.30m v 1.25m, leaving the pace of initial jobless claims essentially unchanged over the past week and suggesting the improvement seen in the labour market over recent months is starting to plateau as indicated in the higher-frequency HomeBase hourly employees data. Retail Sales in contrast were better than expected in June following the record rise in May. Headline sales rose 7.5% m/m v 5.0% expected and followed the sharp 18.2% rise in May. The core control group also beat at 5.6% m/m v. 4.0% expected. The Philly Fed also beat at 24.1 v 20.0e and pointing towards little impact so far from the recent rise in COVID-19 cases on the manufacturing sector. Rounding it out, Homebuilder Sentiment surged to 72 from 58, not surprising given the 30yr mortgage rates has fallen below 3% for the first time since records began in 1971. Still the largely positive data seen overnight is in danger of being dated given the recent rise in COVID-19 cases and the re-imposition of some restrictions in the southern parts of the US.

The USD rose with the DXY +0.3% with broad-based gains. Commodity currencies have underperformed slightly but not overly so, the AUD -0.4% and NZD -0.5%. All focus today will be on the Euro (-0.2% overnight to 1.1379) with EU leaders meeting on the EU recovery fund. My colleague Gavin Friend noted overnight on balance markets sense some sort of agreement which could extend gains on confirmation. Here we’ve suggested the EUR could moves up from a broad 1.10-1.15 range to 1.12-1.17, but with ideas of 1.20 in 2021. If a deal is not in sight this weekend, any EUR pullback will be dependent on the degree of how far away a deal is. A deal on the EU Recovery Fund is still very likely even with the frugal four given how critical it is to the ongoing success of the EU project and the Euro in general. Accordingly we doubt EUR/USD will drop below the 1.250-1.13 area (email Tapas.Strickland@nab.com.au if you would like a copy of Gavin’s piece).

The ECB kept all its policy settings unchanged at its meeting overnight (including the deposit rate at -0.5% and pandemic bond buying programme at €1.35t). President Lagarde pushed back against talk that the ECB might dial back its bond buying in the face of recent data pointing to a quicker-than-expected recovery. Lagarde said the economic risks remained to the downside and it would require “significant upside surprises” for the ECB to stop short of its €1.35t target for bond purchases. Lagarde added that the ECB would continue to skew purchases towards the more vulnerable countries in the region, such as Italy.

The daily number of US cases remains high, in the mid-60,000s but is showing tentative signs of stabilising. Florida remains the current epicentre, reporting almost 14,000 new cases itself overnight.

Elsewhere, the Australian state of Victoria saw a daily record of 317 new cases yesterday while there were also new daily records in Hong Kong (67 new cases) and Tokyo (286 new cases yesterday).

The re-emergence of COVID-19 in places that were previously thought to have the virus under control, illustrates the difficulty in stamping it out, in the absence of a vaccine or effective treatment. AstraZeneca and Oxford are due to report results from their phase one trials on their experimental vaccine on Monday. The Times, Guardian and Nature all reported that the outcomes have been positive.

NZ CPI was a little higher than both market and RBNZ expectations, with quarterly inflation in Q2 falling by -0.5% (market: -0.6%, RBNZ -0.7%), taking the annual rate of inflation into the lower half of the RBNZ’s target range, at 1.5%. Most of the core measures of inflation moved lower as well although, interestingly, not the RBNZ’s favoured Sectoral Factor Model, which remained at 1.8%. My BNZ colleagues note they expect CPI inflation to keep easing in the coming quarters, with the annual rate falling below the bottom of the band by the end of the year before recovering in 2021. There was no market reaction to the CPI release, with investors more focused on the outlook for activity, both in NZ and offshore.

The Australian labour market report was stronger than expected, with employment rising by 211k in June, reversing some of the 870k job losses from the preceding two months, and hours worked rising by 4%. There was little immediate market reaction from the AUD, which trades this morning around 0.6970.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.