Online retail sales growth slowed in May following a fairly strong April

Insight

The US payrolls data was stronger than expected on Friday.

If it makes you happy, It can’t be that bad, If it makes you happy, Then why the hell are you so sad? – Sheryl Crow

The good news from Friday night was that the US labour market remains in rude health, but the not so good news was the negative reaction by UST yields and US equities. The solid US jobs report triggered a spike in UST yields and a pullback in Fed rate cut expectations effectively switching the Fed debate from a 25bps or 50bps rate cut to a 25bps cut or none. US equities closed the week mildly in negative territory, although they did recover most of the payrolls induced losses. The USD made broad gains with NZD losing almost 1% while AUD moved back below the 70c mark.

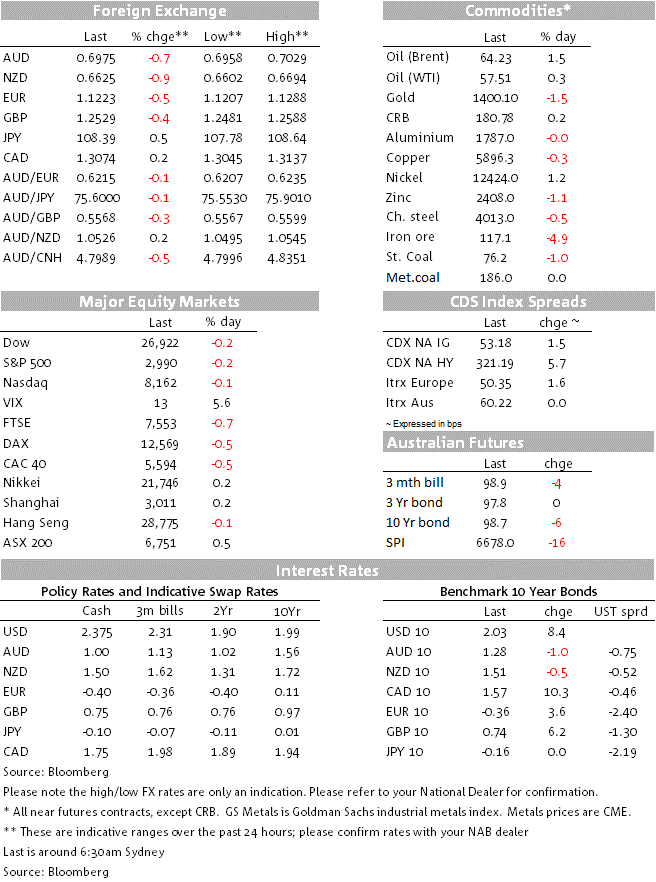

The June payrolls report revealed the US economy created 224k new jobs against expectations of 160k. For the past half year, non-farm payrolls have grown on average by 172K, down from last year’s average 223K average but in line with 2017’s average 180K gain. The unemployment rate edged up to 3.7% from 3.6% and average hourly earnings grew 0.2% in June for annual growth of 3.1%, a repeat of May’s readings. The consensus was looking for 0.3%/3.2%.

The solid US payrolls report dampened Fed rate cut expectations and severely dented the argument for a 50bps rate cut by the end of the month. Effectively the debate has now switched from a 25bps or 50bps rate cut to a 25bps cut or none. Although the US labour market remains in good health, NAB remains of the view that the Fed will look for a couple of insurance cuts ( 25bhps in July and another cut in September) in order to support the economy given subdued inflation and inflation expectations readings while the full negative impact from higher US and China tariffs introduced around the middle of May have not yet worked their way through the US economy.

Reaction to the data triggered a jump in UST yields with the move higher led by the front end of the curve. The 2y rate rose 10bps to 1.85%, while the 10 year yield rose 8bps to 2.03%, with both moving back into recent trading ranges. As for Fed rate cut expectations, the market is now pricing 27bps for the Fed’s meeting later this month, down from 33bps prior to payrolls and looking at rate cut expectations over the next year, the he market now prices 96bps of Fed rate cuts, down from 109bps previously.

Equity markets initially reacted negatively to the prospect of less aggressive monetary stimulus from the Fed. The S&P500 fell just under 1% from their intraday highs, before recovering over the remainder of the session to close only 0.18% lower on the day. Defensive stocks, such as real estate and utilities, which have been the beneficiaries of the recent falls in rates (as investors turn their attention to dividend-based stocks as an alternative to lower yielding fixed income) were the underperformers on the day. In contrast, The KBW bank index was up 0.8%, with the prospect of less aggressive Fed easing perceived as more favourable for bank net interest margins.

The move higher in UST yields triggered broad based gains for the USD with the DXY index moving back above the 97 mark ( +0.54% and now at 97.29) while BBBDXY gained 0.44% to 1195.16. USD indices also made gains for the week and they have effectively now moved back to the top half of their trading ranges over the past year.

Looking at G10 pairs, the CAD was the best performing currency only losing 0.2% against the USD. The loonie’s resistance to the USD gains was largely driven by a solid Canadian employment report which showed a much stronger than expected increase in wage growth (3.6%yoy vs 2.7% yoy). Canadian employment growth was flat on the month, but this followed six months of very strong gains. The market pared back its expectations of rate cuts by the Bank of Canada, but one remains fully-priced over the next 12 months.

EUR, JPY and GBP lost about 0.4% on Friday while the AUD was down 0.70%. Ahead of the US payrolls report the AUD meandered around the 0.7020 mark with many wondering whether a soft print could be the trigger for the pair to eventually break above the 0.7050 resistance that has proven to be a tough nut to crack. In the end it was not to be with the AUD starting the new week at 0.69777. Iron ore was a big mover on Friday, falling 5.4% after the China Iron and Steel Association asked regulators to investigate whether “non-market factors” were behind the recent rise in prices, but as it has been the case for a while AUD showed little sensitivity to the decline in iron prices, similar to the stratospheric jump in prices seen since the start of the year. After peaking around $123, iron ore closed the week at $117, so prices remain elevated.

The NZD underperformed most of the G10 on Friday, and closed down 0.9%, at 0.6630, leaving it back in the lower-half of its trading range for 2019. In the domestic rates market, the 10 year swap rate fell 1bp on Friday, reaching a fresh record low of 1.715% (on a closing basis). NZ rates will open higher, and the curve steeper, today.

On the trade-front, White House Economic advisor Larry Kudlow confirmed that US and Chinese negotiators had recently restarted dialogue over the phone and that a face-to-face meeting was likely “at some point in the near future.” Whether the negotiators can find a solution to the difficult structural issues that remain between the two sides is another matter, and Kudlow cautioned there was “no timeline” to reach an agreement.

Geopolitics may also be a focus at the start of the week following news on Sunday that Iran had breached the nuclear deal’s cap on its stockpile of low-enriched uranium. So far US-Iran tensions have not had a material impact on markets, but if tensions escalate it could be a different story.

Speaking to CNBC, President Trump’s Fed Board nominee Judy Shelton expressed reservations about the Fed’s actions, noting that the Fed shouldn’t put the US at a competitive disadvantage with the rest of the world, where zero-interest policy rates are common. “When you consider that more than half of American households are invested through mutual funds and pension funds in the market, I don’t want the Fed to pull the carpet out from under them by taking a position that is not conducive to further providing the liquidity for this growing economy,” she said.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.