Total spending grew 0.9% in June.

Jobs data is confusing right now. How much is it influenced by government stimulus activity?

Do you wanna see the view from the top of the Empire State Building?

Definitely not, I’m afraid of heights – Wavves

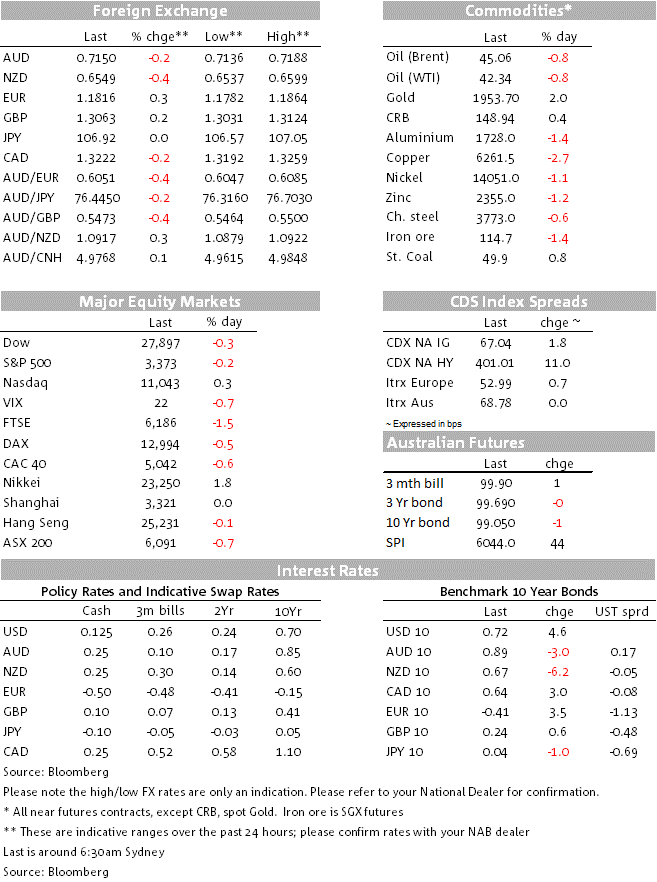

Well many say that the best treatment for altitude sickness is to stop and rest where you are. After making a new all-time high the S&P 500 was unable to sustained the move, ending the day marginally in negative territory. US political stalemate a likely drag as the US Senate next legislative session is set for September 8. A soft 30y UST bond auction has added further fuel the bear steeping theme in the UST curve and the USD has had a mixed night, losing ground against EU currencies, but a tad stronger against both the AUD and NZD. AUD now trades at 0.7149 and NZD at 0.6547.

The S&P 500 has ended the day down 0.2% while the NASDAQ closed 0.27% higher, with Apple share (1.77%) helping the tech heavy index stay above positive territory. European equities broke a four day winning streak with the Eurostoxx 50 index -0.60% while all major regional indices were down between 0.6% and 0.8%. The UK FTSE 100 was the worst performer down 1.50%.

The softness in Europe equities has been partly attributed to a series of disappointing earnings reports. Deutsche Bank fell on plans to accelerate job cuts while Aegon’s dived after results missed estimates. US-EU trade relationship has also been a concern following news that 24 European countries lodged a complaint with the US State Department this week over President Donald Trump’s expansive use of sanctions to help influence American foreign policy goals.

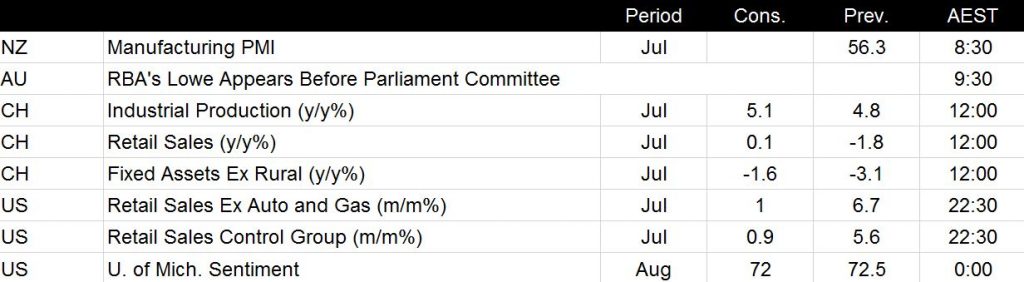

Before the US senate news (more on that below), the US equity market was boosted by positive US jobs data and still improving virus news. The rate of new COVID-19 cases continues to trend lower in the US, albeit from very high levels.

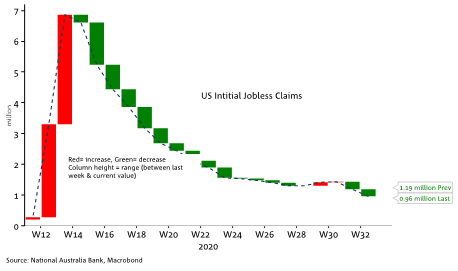

US jobless claims fell below 1 million for the first time since mid-March, pointing to a continued recovery in the US labour market (although the level of jobless claims remains very high, above that seen after the GFC). After stalling over several weeks, US jobless have began to decline again ( see chart of the day below), suggesting the US labour market is starting to improve, notwithstanding the economic impact from the containment measures introduced to combat the COVID-19 outbreak. Ironically, an improving labour market may ease the pressure on US politician to come up with a new stimulus plan.

While these positive news contributed to the S&P 500 record high move ( 3387.89), political news likely played into the dampening vibes late in the session. During the NY afternoon, Senate Majority Leader McConnell announced the Senate’s next legislative session will begin September 8, effectively killing any hopes for a stimulus agreement over the coming weeks. Highlighting the disparity in views, House Speaker Nancy Pelosi said she would be willing to meet with the Trump administration again “when they come in with $2 trillion,” plan and in response Senator McConnell described the Democrats view as “throwing spaghetti at the wall to see what sticks.”

Global rates have continued to track higher, with the US 10-year Treasury yield hitting its highest level in almost 8 weeks, at 0.72%. This morning’s record $26b auction of 30-year bonds came 2.4bps above pre-auction secondary market levels, helping to drive a steepening in the yield curve (5y +1bps, 10y +3bps, 30y +6bps). Market-implied inflation expectations also continue to push higher, with the 10-year ‘breakeven inflation’ rate reaching its highest level since January, at almost 1.7%. Market-based inflation expectations remain low in absolute terms but the trend higher is one to watch. Curve steepening is the other implicit theme, as front end yield remain anchored by central bank policy, the market will soon begin to wonder how much tolerance central bank’s have for the issuance driven rise in longer dated yields. On the week 10y UST yields are up 12bps while the 30bond is up 23bps to 1.4277%.

The USD is a tad softer in index terms (DXY -0.19% to 93.243, BBDXY -0.16% to 1177.21) with its weakness largely due to the strength in EU currencies. NOK is up 0.71% and the euro is up 0.26% to 1.1814.

NZD ( @0.6547) and AUD (@0.7149) are the two notable underperformers, down 0.44% and 0.17% respectively. RBNZ rhetoric a likely contributor to the Kiwi’s underperformance amid the usual flurry of media interviews from senior RBNZ officials post-MPS. RBNZ Chief Economist Yuong Ha reiterated that the Bank was actively seeking to drive bond yields lower with its frontloaded purchases. On the possibility of negative rates, which the MPS set out as the likely next policy step if required, Ha said it was dependent on the economic outlook, adding “it’s conditional. It’s not inevitable.” Ha said the Bank would prefer a lower exchange rate but acknowledged that they were limited in how much they could influence it.

AUD underperformance may have also been influence by the weakness in metal prices overnight. Copper has been a big underperformer, down 3.16%, its biggest decline since April, following new of an increase in output by Codelco, the Chilean state-owned mining company, noted a “quick” ramp-up at its Chuquicamata underground operation. The LMEX index closed 1.82% lower, iron ore lost .3% and gold gained .098%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.