Total spending grew 0.9% in June.

The ECB’s Philip Lane expressed concern about the tightening of credit standards which could impede the European recovery.

https://soundcloud.com/user-291029717/astra-zeneca-re-run-lanes-credit-concerns?in=user-291029717/sets/the-morning-call

It’s oh so quiet, Shh shh, It’s oh so still

Shh shh, You’re all alone, Shh shh

And so peaceful until…. – Björk

It’s been a relatively quiet market session overnight with the US out celebrating Thanksgiving.

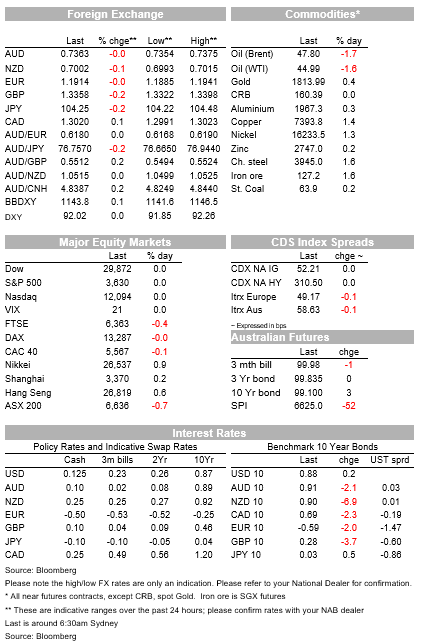

Regional European equity indices closed marginally in the red while US equity futures are mixed, S&P 500 mini down 0.26% while the NASDAQ 100 mini is up a couple of bps.

COVID-19 infections print a new record in Germany and continue to rise in the US while AstraZeneca comes under pressure after acknowledging errors in initial trials.

US Treasury futures and the USD are slightly higher with NOK the big underperformer in G10, following the move lower in oil prices.

There has been a bit of focus on COVID-19 news with Germany making undesired headlines after surpassing 1 million COVID-19 cases since the start of the pandemic. Infections have tripled since the start of October and, as a result, the number of people with the disease in intensive care has climbed to record levels. Merkel also called on Europe’s ski resorts to close this winter to halt the spread of the illness.

Bloomberg reports California and Texas broke daily infection records, while an outbreak is accelerating in the Southwest and Rocky Mountain regions. An estimated 50m Americans are travelling around the States during a pandemic that has seen an explosive rise in daily case numbers of COVID19 over the past couple of months.

With that in mind it is hard to see the current wave of new case numbers moderating anytime soon, and the bigger risk is that in a couple of weeks reported figures deteriorate from the current run-rate of 1.25 million per week in the country.

AstraZeneca has come under pressure as experts criticised the lack of detail on the clinical trial results and the Company’s acknowledgement that the group with 90% effectiveness came as a result of patients accidentally given a lower dose than intended. The head of the US vaccine program said the group showing the higher level of effectiveness was tested in a younger population. The lower rate of effectiveness (62%) when the vaccine was applied with two full doses was achieved in a group included participants aged over 55. None of this information was disclose in AstraZeneca’s original statement.

S&P500 futures are only down slightly for the day and the Euro Stoxx 600 index only fell by 0.12%. Astra Zeneca’s share price in London fell just 0.7%. US 10-year Treasury futures are slightly higher.

The USD has edged a little bit higher in index terms with the DXY reversing yesterday’s small loses to be unchanged at 92.018 while BBDXY is marginally higher at 1143 (+0.08%).

NOK is once again the big mover retaining it high level of sensitivity to the decline in oil prices, Brent and WTI are down around 1.6%, although prices are still up just over 7% over the past 5 days. NOK is down 0.5% and now trades at 9.8788.

The market is starting to wonder about OPEC’s next move.

Bloomberg reports Iraq’s deputy leader this week criticized OPEC, saying the economic and political conditions of member countries should be considered before they are asked to withhold production. OPEC’s president said Thursday the group must remain cautious, with internal data pointing to the risk of a new oil surplus early next year.

UK-EU trade negotiations remain tortuous and the latest suggestions are that agreement is unlikely before the end of the weekend and more likely sometime next week, continuing the ever-shifting “deadlines”.

My BNZ colleague, Jason Wong, noted a headline in his daily “Thousands of sheep stuck in limbo over Brexit regulations”, which illustrates a familiar theme applying to other goods, even with a skinny trade deal. This is the cost of the UK leaving the EU.

The AUD and NZD are unchanged over the past 24 hours currently trading at 0.7365 and 07007 respectively.

Both antipodean currencies have essentially consolidated their recent gains, NZD is up 1.26% over the past 5 days while the AUD is up 1.04%.

The euro has eased to 1.1916.

Virus news, specially from Germany have certainly not helped. But development surrounding the ratification of the EU Recovery Fund and Budget are also a consideration. Poland and Hungary have stepped up their opposition to the linkage of budget finances and the rule of law.

PM Orban and Moraweicki said “The proposed conditionality circumvents the Treaty, applies vague definitions and ambiguous terms without clear criteria on which sanctions can be based and contains no meaningful procedural guarantees,” Orban and Moraweicki also reiterated their readiness to veto the fund and budget in their current form.

EU government envoys in Brussels will debate the deadlock over a non-public meeting on Friday, where the impasse in Brexit talks will also be discussed. If Poland and Hungary don’t yield, the EU could adopt the rule-of-law conditions for the EU budget by a qualified majority, effectively bypassing Hungary and Poland’s opposition while also excluding them from much needed funding.

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.