Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

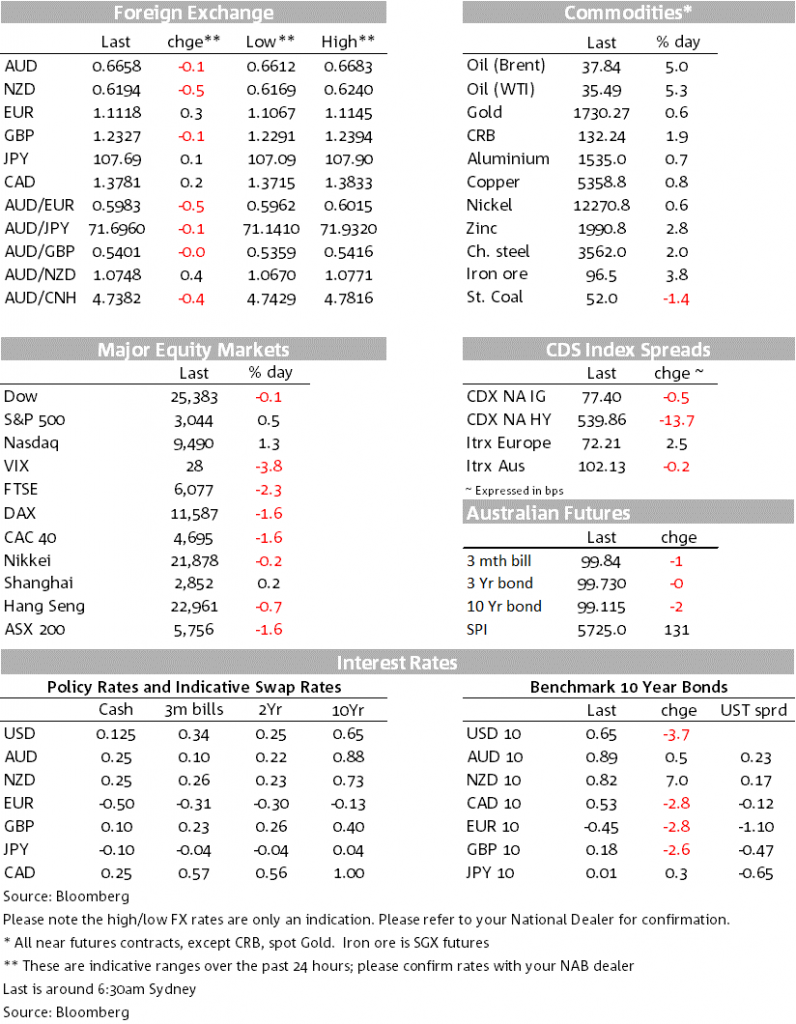

We’re seeing iron ore prices rise largely because of concerns over supply from Brazil.

https://soundcloud.com/user-291029717/less-shock-more-ore?in=user-291029717/sets/the-morning-call

“Now you’ve seen me at my worst; And it won’t be the last time I’m down there; I want you to know I feel completely at ease; Read me like a book” Crowded House 1991

Markets were relieved on Friday that Trump’s much anticipated press conference on Hong Kong did not contain anything further than Pompeo’s already flagged actions of removing Hong Kong’s favoured trading status. There are no new tariffs or broad sanctions and the Phase 1 Trade Deal remains intact. Rightly or wrongly some are concluding Trump’s need for farm purchases into November acts as a break to a more significant deterioration in the relationship and USD/CNH fell -0.4%. Risk assets rallied in relief with the S&P500 +0.5% and WTI Oil +5.3% and largely ignoring weaker than expected data that shows Q2 GDP Now at -51.2% annualised.

Global FX which had seen a cautious tone emerge into the press conference reversed moves with most FX pairs little changed over the day. Over the week though the USD is on the backfoot, down -1.5% with the biggest gains in the global growth/risk currencies such as the AUD +2.0%, NZD +1.9% and USD/NOK -2.9%, while the EUR finds its fiscal mojo and is up 1.8% over the week. Yields were moderately lower on Friday (US 10yr -3.7bps to 0.65%), though curves over the week have steepened as the conversation tilts towards yield curve control in the US (2/30s +4bps to 124.6bps) (see WSJ’s Timiaros for a recent piece). In commodities there has been a sharp rally in the iron ore price (+3.8%) from Brazilian production worries given COVID-19, which along with China’s PMIs showing fiscal stimulus traction, should see markets open the week with a positive tone.

Trump announced he is beginning “the process of eliminating policy exemptions that give Hong Kong different and special treatment [incl our extradition treaty, to our export controls and technologies]”. Importantly though there were no new tariffs or broad sanctions with the Phase 1 Trade Deal intact, with the outcome less feared. Some are drawing the link between President Trump’s need for agricultural buys to shore up the mid-west ahead of the November Presidential Elections (rightly or wrongly). In that vein Reuters noted that China threatened to reduce its agricultural imports if there was a severe response while China has been buying Brazilian soy over US since the trade war emerged. Trump also said he was ready to take action to mandate that Chinese and other foreign companies listed on U.S. financial exchanges abide by American accounting and audit standards.

US data continues to backseat, though April activity numbers showed painted a truly shocking picture with Q2 GDP Now sitting at -51.2% annualised from -40.4% before the data drop. Personal Spending fell by a sharp -13.6% m/m against -12.9% expected. Personal Income in contrast rose 10.5% m/m as a sharp rise in government payments more than offset the 8% decline in wages and salaries (excl. government payment boost personal income would have fallen -3.5% m/m). Consequently the savings rate soared to 33% from 12.7% in March and 8.2% in February. Inflation figures also painted a subdued picture with the Core PCE Deflator -0.4% m/m against -0.3% expected and is running at 1.0% y/y. The Chicago PMI which was expected to rise in May instead fell further to 32.3 from 35.4, while Consumer Sentiment was revised lower in the final read to 72.3.

Chinese PMIs on Sunday in contrast are showing indications of recovery with infrastructure spending picking up. While the Manufacturing PMI was 50.6 against 51.1 expected and 50.8 previously, the Construction PMI increased to 60.8 from 59.7 and the Steel PMI surged to 50.9 from 45.9 previously. Against that remains a weak external sector with New Export Orders in the manufacturing sector remains worryingly deep in contraction territory at 35.3 (from 33.5). The degree to which domestic stimulus can offset weak export demand will be key in determining the sustainability of the recent pick-up. The National Statistics Bureau noted while 81.2% of surveyed businesses had reached more than 80% of normal production levels in May, 54.6% of companies reported insufficient orders.

In Australia the housing market has emerged from lockdown with listings edging higher. CoreLogic reports preliminary auction results returned a 65.9 per cent clearance rate. The previous week saw 612 homes scheduled for auction and a final clearance rate of 62.7 per cent. One year ago, there were 1,661 homes taken to auction and a 58.0 per cent clearance rate. The AFR also reports a housing stimulus package is expected to be announced this week ($20K for first home buyers and direct grants for renovations).

It’s a big week domestically with the RBA (Tuesday) and Q1 GDP (Wednesday), though both are unlikely to faze markets too much given the backward looking nature of GDP and Governor Lowe’s comprehensive remarks at a Senate Select Committee last Thursday. At that hearing Governor Lowe said the economy was tracking between the RBA’s baseline and upside scenarios, pushed back on the prospect of negative rates, defined forward guidance as “not going to be raising interest rates until full employment is achieved and we’re sustainably within the 2-3% target”, and said his “main concern is that we don’t withdraw the fiscal stimulus too early” (see Hansard for details). As for GDP, NAB is forecasting Q1 to fall -0.1% q/q (consensus -0.4%). Before GDP are the usual partials of Net Exports, Company Profits & Inventories, and Government Spending – now all on Tuesday.

It is all about the ECB (Thursday), and US Jobless Claims and Payrolls (Thursday and Friday); note the Bank of Canada also meets on Wednesday. As for the ECB the consensus looks for a €500bn increase in QE via the Pandemic Emergency Purchase Program (already at €750bn). The ECB meeting is also the first since the German Constitutional court raised questions about the legality of QE. As for Payrolls, while they should show another sharp rise in the unemployment rate to 19.6% and the loss of 8m jobs, more interest could be with Jobless Claims given the first signs of a trough last week and the consensus looking for another decline in continuing claims. Focus will also remain on signs of activity lifting with the US ISMs for May (Monday and Wednesday) which receive the bulk of responses late in the month, as well as ongoing US/China tensions.

It is quiet domestically with only House Prices for May of note (though not usually market moving).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.