We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Everyone is seeing the silver lining, but clouds could be forming.

https://soundcloud.com/user-291029717/look-out-for-the-cloud-in-the-silver-lining?in=user-291029717/sets/the-morning-call

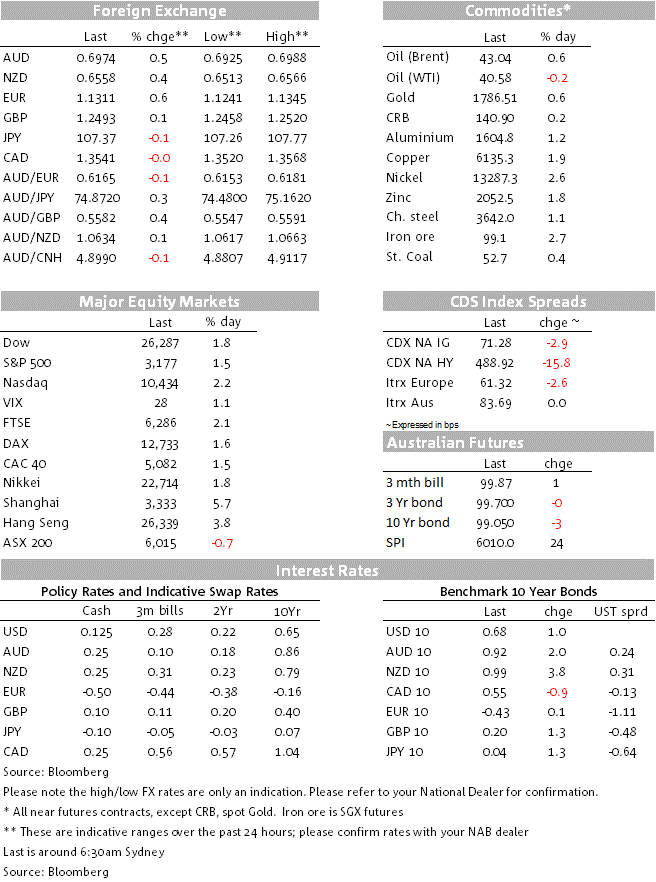

Much better than forecast US non-manufacturing ISM at 57.1 feeds the risk rally begun by Shanghai’s 5% Monday gain. USD softer across the board but AUD (high of 0.6988) and NZD (0.6566) still inside prevailing ranges. US bond yields step back a little from their APAC session gains.

The strength of the Chinese stock market has been the standout feature at the start of the new week, Monday’s 5.7% gain for the Shanghai Composite index bringing the rally so far in July to some 13% and to its best level in two years. Last week’s China PMI numbers, the non-official Caixin versions in particular, have provided a fundamental pretext for the run up, but there is little doubt that the urgings of the Chinese government have also played a part. Yesterday’s state-sponsored Securities Journal ran a front page editorial saying that “fostering a healthy bull market after the pandemic is now ever more important than ever”. Shades of John F Kennedy’s “Ask not what your country can do for you” inauguration speech here and as close as you might get to a Chinese government ‘put’ as anything the Fed has done to date vis-à-vis the US stock (and credit) markets.

Has been the US non-manufacturing ISM (and remember services makes up about 88% of the US economy). The 57.1 headline print significantly exceeded the 50.2 consensus estimate and the 45.2 May print, ostensibly meaning the sector was in outright expansion mode last month. New orders (61.6) and Business Activity (66.0) drive the improvement in the headline reading, though employment at 43.1 (from 31.8) suggests that employers were shedding not adding jobs last months, in which respect the likes of the flattening out in weekly jobless claims in the last couple of weeks is hinting that the gains in employment in May and June may suffer something of a setback in July and/or August.

Was German factory orders, where the 10.4% rise was much less than the ~15% expected and after a 26.2% April drop.

There has been nothing to cheer in latest COVID-19 news, not that that has any bearing on the performance of risk assets at the moment. The 7-day average of new infections in the US reached a new record yesterday, New Jersey’s Rt crept above 1.0, and in Victoria the number of new infections reported yesterday rose to 127 having been in the 60-80 range in previous days.

The technology company that is undoubtedly benefiting most from the crisis and social distancing strictures, Amazon, saw its share price rise above $3,000 for the first time, a 6% gain for the day and now up 13% month to date. Even more impressive, the world’s most valuable car company, Tesla, saw its stock up 13% on Monday, to be a heady 43% up on its June 16 local low. Together, these stocks helped propel the NASDAQ to a new high (+2.2% on the day) with the S&P ending +1.6%. Earlier, the Eurostoxx 50 added 1.7%.

The ASX was the clear laggard Monday, down 0.7% and where the combination of the Victoria COVID-19 news and the Weekend Australian report saying the Government was expecting further retaliatorily trade actions by China following its public opposition to the new Hong Kong security law, both weighing.

The negative correlation between the US dollar and risk sentiment remains in place, the narrow DXY index down 0.4% and the broader BBDXY -0.3%. AUD (+0.5% to a high of 0.6988) and NZD (0.35% to a high of 0.6566) have been outpaced by the EUR, SEK and NOK and keep both antipodean pairs trading beneath their recent range highs (broadly defined as 0.66 for the Kiwi and 0.7050 for Aussie).

Where the 10 year US Treasury yield slipped back a basis point or so after rising over 2bps during Monday’s Tokyo trading, just closing in New York +0.7bp at 0.676%. Commodities are mostly higher, with Brent crude up 0.6% (WTI -0.2%) gold +0.6% and base metals stronger across the board (aluminium, copper. nickel and zinc all up by between 1% and 2%. A similar story for steel (1.1%) and iron ore futures (+2.7%).

The RBA this afternoon can confidently expected to be on hold as it continues to assess the outlook, where even in its best-case upside scenario, full economic recovery will take years. Further, Governor Lowe has emphasised that the economic recovery depends on health outcomes and how quickly confidence is restored, where the recent COVID-19 outbreaks in Victoria have presented an additional downside risk.

RBA Governor Lowe and Deputy Governor Debelle have both emphasised in recent remarks that the economic outlook remains highly uncertain, even though recent data has shown a smaller initial economic hit than first feared. In particular, Governor Lowe has emphasised his concern that the recovery may be stymied if fiscal stimulus is withdrawn too abruptly.

The government’s decision on how to taper its assistance programmes – to be announced on 23 July – will be key to the outlook. Currently, most of its economic crisis measures are slated to end in September, including the JobKeeper wage subsidy. A large 3.3 million workers are currently supported by the $1500 per fortnight JobKeeper payment ($39,000 pa) and an unknown proportion of these workers will fall into unemployment when the subsidy ends. Unemployment benefits are also currently set to revert to $566 a fortnight ($14,700 pa), which points to a large hit to household incomes if the government does not extend support.

Before the RBA this evening we get the AiG Performance of Services index (last at 31.2) and weekly consumer confidence and offshore early this evening German May industrial production (seen +10.5%).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.