NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The RBA announced cuts to interest rates and a $100bn bond buying program yesterday.

https://soundcloud.com/user-291029717/lowe-goes-heavy-us-stocks-run-hot-on-biden-hope?in=user-291029717/sets/the-morning-call

“Please, please, Mr. Postman; (Why’s it takin’ such a long time); Oh yeah; (For me to hear from that boy of mine); There must be some word today” The Carpenters, 1975

Please Mr Postman was a two time number one hit on the Billboard Top 100 (the first for the Marvelettes in 1961 and then Carpenters in 1975). While many of our readers will not even know who The Carpenters were, there is a fair chance President Trump and Presidential hopeful Biden do given the importance postal ballots are likely to play in today’s election. Around 64.7m mail-in ballots have been cast and returned according to the US Elections Project , with a total of 100.6m Americans likely to have cast their vote prior to the official election day. Those mail-in votes are likely to take a couple of days to process in many states (particularly the battleground state of Pennsylvania) so we may not know a clear result later today (polls start closing at 11.00am AEDT). It is still possible that later tonight looks like President Trump in the lead, only for that lead to be reversed as the mail-in count starts with mail-ins favouring Biden. The biggest risk for markets remains a contested election and whether the Democrats are able to gain a Senate majority.

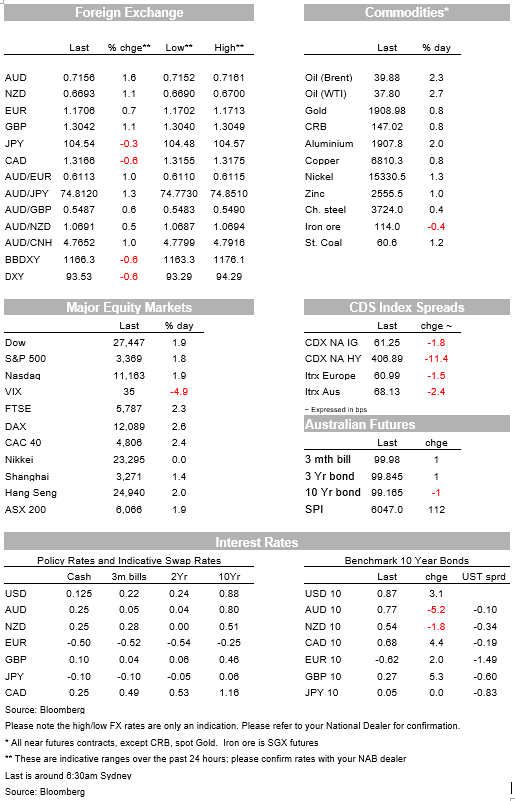

Markets appear to be up and running with a Biden win and pricing towards a Democratic Senate majority given polling. US equities rose strongly overnight with the S&P500 +1.7% with outperformance by financials (+2.4%) and cyclicals (industrials +2.6%, consumer discretionary +2.1%). Yields have also risen with the curve steepening (a driver of the outperformance of financials) with US 10yr yields +3.9% to 0.88%. Earlier in the night 10yr yields hit a high of 0.8959% (a four month high) with a Democratic Senate majority seen as cementing a ramp up in fiscal spending. Note the risk of higher yields also needs to be weighed against the hand of the Federal Reserve who would likely act to keep longer-run rates in check via extending QE and twisting purchases towards the longer end. On that note the FOMC meets Thursday (announcement and presser from 6am Friday AEDT). If the US Fed fails to push back on the movement in rates and a Democratic Senate looks likely, a further move up in rights is likely.

The USD fell sharply on the risk rally with the DXY -0.6%, with EUR +0.6% to 1.1706, GBP +0.9% to 1.3017, and USD/YEN -0.3% to 104.58. Negative UK-EU trade headlines had little impact with markets firmly concentrated on the US election (FT had a story saying the EU’s Barnier was going to signal to leaders a lack of Brexit breakthrough on key issues). Global growth proxies outperformed with AUD +1.4% to 0.7138, NZD +0.9% to 0.6678 and USD/NOK -1.6% to 9.4248.

The AUD also clearly outperformed on the crosses with AUD/NZD +0.5% and AUD/YEN +1.1% and highlights that the RBA’s policy easing yesterday was well flagged and barely caused a ripple as far as FX markets. Central banks are clearly stepping up around the world again as the second wave of the virus takes hold. The ECB signalled that last week and the BoE meets on Thursday along with the US Fed. While more QE and other innovations could have further impacts on rates, for FX the impact should be limited. It’s the classic case of if everyone else is doing it – or as the Red Queen said in Alice in Wonderland “it takes all the running you can do, to keep in the same place ”. Accordingly by FX colleagues remain of the view that the AUD remains in the hands of global forces and the fate of the USD, which means we maintain a stronger AUD/USD view over coming quarters.

As for the RBA meeting yesterday, the RBA largely met expectation of cutting the cash rate, 3yr YCC and TFF rate for new borrowing by 15bps to 0.10%, as well as undertaking a QE program of $100bn with maturities of around 5-10 years over the next six months. Three slight surprises did see yields fall in the wake of the RBA meeting, though with little impact on the currency. With the lift in yields overnight, 10yr Futures have also mostly reversed the yield moves seen after the RBA (10yr Future +1bps). The three slight surprises were cutting the rate on Exchange Settlement deposits to 0.00% (most had expected a rate between 0.01-0.05), the QE program including state government bonds (purchases are split at 80% ACGBs and 20% Semis), and the QE target being slightly more aggressive in the near-term (6m $100bn program v. market expectations of same over 12m). Note the RBA also signalled it could do more if needed.

RBA Governor Lowe spoke soon after the meeting and hinted the risk is the RBA will need to do more after noting in Q&A that the RBA’s forecasts include the policy package and those forecasts still sees unemployment only falling to 6% by the end of 2022, while core inflation remains below the 2-3% target band at 1½% in 2022. As for what the RBA would be willing to do, if further stimulus was need, Dr Lowe seemed resigned to more QE, again ruling out negative rates unless the US Federal Reserve went to negative (“the Board continues to view a negative policy rate in Australia as extraordinarily unlikely”; “it is certainly possible for us to increase the size of our bond purchases…if we need to do more, we can and we will”). One side note for market participants is that the 5-10yr bond purchases are broadly based on bonds in the futures basket, so will include bonds of a greater maturity of 5-10 years at times.

More reports that China is set to bar some Australian exports from Friday. The South China Morning Post reported late yesterday that “ from Friday, barley, sugar, red wine, timber, coal, lobster, copper ore and copper concentrates from Australia, are expected to be barred from China even if the goods have been paid for and have arrived at ports. The ban on wheat is likely to follow, although a date has not yet been set, sources said. It is understood that Beijing will communicate the bans to all Chinese state-owned and private traders by Tuesday. Traders who have already been notified said no formal document was issued nor were reasons provided.” (see SCMP for details).

Overnight the halting of the listing of Ant Group in China and Hong Kong, which was set to be the world’s biggest IPO. The news could weigh on Asian equities with Alibaba who owns around a third of the company down as much as 6.7% in pre-market trade. As for An Group, at the last minute, Chinese regulators have decided on new capital requirements, which will change the “economics” of the business for this fintech firm, with some claiming political interference.

Finally in terms of data it was a quiet night with only final versions of the PMIs and a final read of US Durable/Capital Orders.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.