We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Ray discusses the possible scenarios that could play out in Australian politics today and what the market impact will be – it’s already hit the Aussie dollar quite markedly.

https://soundcloud.com/user-291029717/malcolm-moves-on-the-market-impact

No shortage of contenders for today’s song title, with Genesis’ Land of Confusion, OMC’s ‘How Bizarre’ and Barry McGuire’s ‘Eve of Destruction’ all worthy contributions from my colleagues. The plaudits though went to my muso daughter for the Queen song that immediately tripped off her tongued when asked; not bad considering it was penned more than 15 years before she was born. Go Freddie.

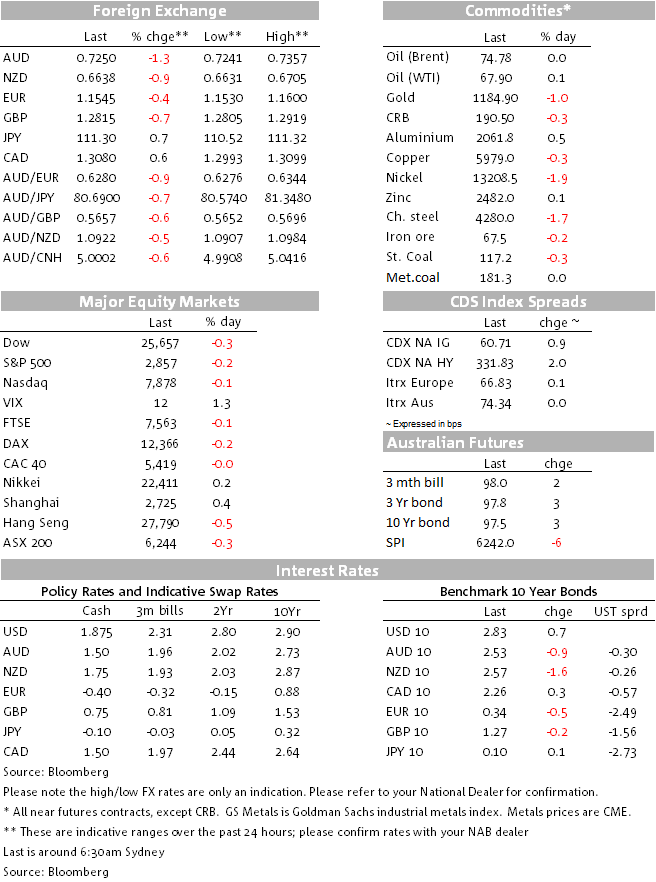

Looking across markets, not much to say about international equities or bonds overnight where the S&P is closing down about 0.2% and Treasury yields are little changed, albeit the US Treasury curve is another 2bps or so flatter led by a pick-up in yields at the front end. All of the action is in currencies, led by a 1.35% drop in the AUD to currently sit around 0.7250, amid a generally stronger USD.

Sky News us reporting that Peter Dutton has the required 43 signatures demanded yesterday by Malcom Turnbull in order to call a party room meet/vote today, while the Sydney Morning Herald has just reported that Peter Dutton has released new legal advice stating he is unequivocally entitled to sit in parliament. We need to hear the latter directly from the Solicitor General’s mouth, but assuming this is the case then odds on Peter Dutton winning a party room vote today and being the new Prime Minister by lunchtime will likely be holding below $2.0 ($1.90 late yesterday afternoon) Scott Morrison was sitting at about $4 last night and Julie Bishop $6 (but she has since come in to nearer $4).

Assuming so, then perhaps worth noting that one point of policy differentiation between a Dutton led-Liberal government and a Turnbull/Morrison/Bishop one, is that Ditton has already signalled a reduction in immigration. If implemented, this is something that would likely lower growth, but may also slow growth in the labour supply. Dutton is also thought to be more of a policy hawk when it comes to China. He also floated a number of alternative policy proposals, though we would expect him to take some time to formulate his policy direction more fully.

It is also worth making the point that unless the Liberal party’s poll standing quickly improves under a Dutton-led government, that market belief both that the election is more likely to come sooner than May next year, and that a change of government is more likely than not, might limit the ability of the AUD to rebound, at least on domestic political factors.

AUD was under pressure from mid-morning time yesterday but not just on domestic political shenanigans. The latter news came at about the same time that Australian security forces were reporting that they opposed the involvement of China’s ZTE and Huawei in the roll out of the 5G network in Australia. Last night a China foreign ministry spokesman urged the Australian government to abandon “ideological biases”.

AUD/USD fell from around 0.7350 to the high 0.72s in our time and has fallen further, to a low of 0.7244, these latter moves coming in the context of fairly broad-based USD strength that sees EUR/USD off half a cent (EZ PMIs were fairly flat and not a market mover) and the British Pound 0.75% lower. GBP has not been helped by the latest government report on the implications of a no deal/hard Brexit, which highlighted potential disruption to banking services, pension payments, higher prices and the step-up in red-tape that would be required regarding trade with the EU as “non-preferential, World Trade Organisation” terms would apply.

Emerging market currencies have also been under pressure, the South African Rand still suffering from Trump’s twitter intervention yesterday saying he has asked Secretary of State Mike Pompeo to ‘closely study’ South African land, farm seizures and ‘large scale killing of farmers’, an accusation the South African President Ramaphosa has strenuously denied. ZAR is 1.7% lower, as is the Brazilian Real as political (election) concerns continue to mount.

US 10yr Treasuries are up 1bp at 2.83%, unaffected by the slightly risk-off tone in equities. 2yrs have sold-off 2bp to 2.61%, leaving the 2s10s curve at yet another cycle low of 20.5bp.

Kansas Fed President George said overnight that Trump’s criticism of the Fed won’t influence the central bank’s decisions. A known hawk, she expected two more hikes this year and thought the neutral rate was 3%, just over 100bps higher than the current Fed Funds rate. She suggested it was a difficult debate about how much to raise rates before pausing its upward march. We’ll hear more from the Fed tonight when Chair Powell addresses the Jackson Hole conference.

The S&P 500 is 0.17% down at the close, the Dow -0.3% and NASDAQ 0.13%. Energy, materials and financials have led the S&P decline, down 0.5-0.75%. Earlier European stocks ended with even smaller declines than the US, while yesterday the ASX (-0.34%) was an underperformer and where the political news did appear to be taking a toll, financial and real estate leading the decline. Is the latter a reflection of perfections Labor may now be closer to being in power and given its stated policy on negative gearing?

Oil is little changed on this time yesterday. Gold is down another 1% and base metals mixed with aluminium up 0.5%, nickel down 1.9, iron ore -0.2% and China steel prices off 1.9%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.