NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

There was a swift market reaction to President Trump’s announcement of further tariffs on imports from China

https://soundcloud.com/user-291029717/market-prices-us-china-trade-escalation?in=user-291029717/sets/the-morning-call

“But what a fool believes he sees, no wise man has the power to reason away” – the Doobie Brothers

Aftershocks from President Trump’s Thursday afternoon Twitter announcement of 10% tariffs on the remaining $300bn of Chinese imports, effective September 1st, continued to be felt on Friday – and are set to the dominate the global economic and financial landscape in coming weeks and months.

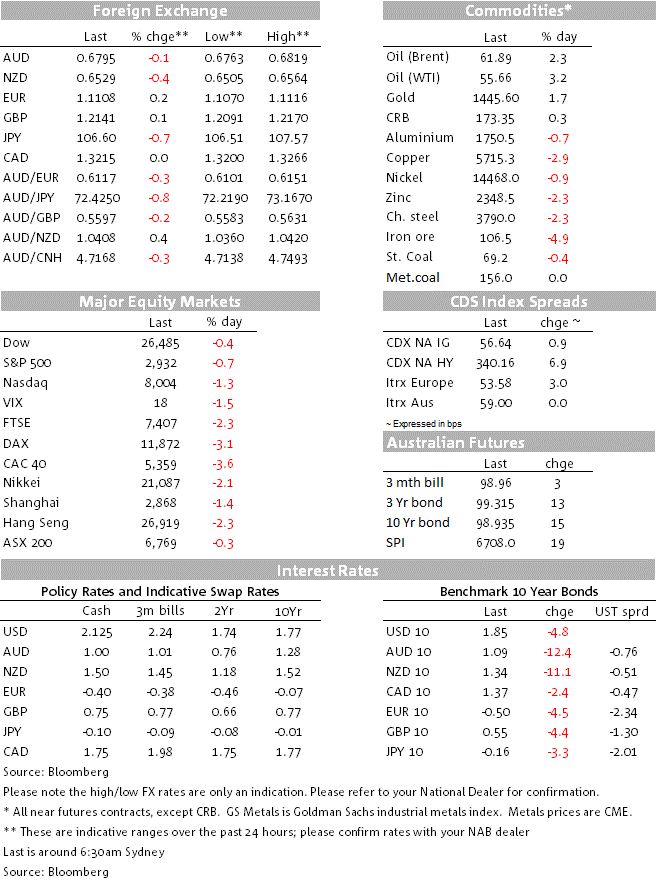

Thursday’s announcement came too late for European stocks markets to immediately respond, which they did on Friday in spades, the Eurostoxx 50 down 3.3% led by declines of 3.6% in France’s CAC-40 and a 3.1% fall in Germany’s Dax. It’s possible the scale of these losses owed something to reports that the White House would be making a statement about EU trade on Friday afternoon Washington Time, evidently arousing some fear that a tariff announcement against EU imports was imminent, bearing in mind the White House has been sitting on a report from the Commerce Department on whether auto imports could constitute a threat to national security.

As it turned out, there was no such announcement, though the New York Times reported that the subject of the announcement was to be US beef exports to the EU and an increase in the US’s share of the overall 45,000 tonne EU quota. If so, this could means fewer imports from other countries, though this is largely irrelevant for Australia, who has an EU quota of just 7.150 tonnes for high quality beef exports – effectively zero in the context of the 1.1 million tonnes of beef Australia exports each year (more than 300,000 tonnes of which is to Japan and over 125,000 tonnes to China).

This doesn’t of course mean that Trump won’t soon train his sights on the EU, as he persists in convincing his support base that tariffs on China are being paid by China (they are not) and that his tactics will succeed in getting his perceived economic foes to agree to new trade arrangements much sooner than otherwise (they won’t). What is true is that if Trump goes through with his threat to impose 10% tariffs on September 1st – with the threat of scaling up the tariff rate in short order – US consumers will be feeling the pinch via higher prices in fairly short order. Toys, sports equipment, footwear and clothing top the list of imported consumer goods that are 90-100% sourced from China. Anyone for tennis?

In response to Thursday’s Trump tweet, China’s Commerce Ministry issued a statement saying that China will have to take necessary countermeasures to resolutely defend it core interests, while a Finance Ministry spokeswoman said that “China won’t accept any maximum pressure, threat, or blackmailing, and won’t compromise at all on major principle matters”.

US stock markets fell further on Friday, the S&P by 0.7% and NASDAQ by 1.3% to bring their losses for the week to 3.1% and 3.9% respectively. In APAC, Shanghai was down 1.4% Friday (-2.6% on the week) the Nikkei -2.1% (-2.6% w/w) while the ASX was a relative winner, off just 0.4% Friday and -0.3% on the week.

In currencies, it was JPY and CHF, the markets two preferred safe-haven darlings, which showed the strongest response to the tariff news, CHF +0.8% and JPY +0.7% against the USD. As well as mechanically softening the DXY given their 17% combined weight, it was also the case that USD strength was curtailed by the further sharp fall in US bond yields. 2-year Treasuries fell another 2bps Friday to be 14bps down on the week and 10s by a bigger 4.7bps to be 22.4bps lower at 1.83% (the lowest since November 2016).

The US money market is not having a bar of Fed Chair Jay Powell’s claim of a ‘mid-cycle adjustment’, now pricing a terminal Fed Funds rate of 1.22% rate – 92bps below the current Effective rate.

AUD was surprisingly resilient on Friday (unlike NZD which lost another 0.3% to 0.6527). It finished flat on the day, through is 1.6% lower on the week and faring slightly worse than its trans-Tasman cousin, the latter -1.5%. Instructive here is that the JP Morgan EMFX index lost a similar amount (-1.5%). The latter, driven by a move up in USD/CNH to 6.9750 from 6.91 prior to the tariff news, will be pivotal to the AUD and NZD’s fortunes in coming weeks and months. If USD/CNY is going to be allowed to rise though 7.0 as looks increasingly probable, then more weakness lies ahead for AUD and NZD and NAB/BNZ’s earlier forecast for a modest recovery in both currencies into year-end will be in need of revision. Watch this space.

It would be remiss not to mention Friday’s US payrolls, as much as a non-event as this was. Payrolls rose by 164k, bang in line with expectations, though there was 41k worth of downward revision to the prior two months. The unemployment rate held at 3.7% against expectations for a fall to 3.6%, thanks largely to an uptick in the participation rate to 63% from 62.9%, though the U6 underemployment rate dropped to a new cycle low 0.7% from 7.2%. This represents the unemployment rate, plus marginally attached workers plus those who aren’t working a many hours as they’d like. Incidentally, the equivalent Australian rate is 13.4% and goes some way to explaining the lack of upward wages pressure here. US average hourly earnings rose by 0.3%, not the 0.2% expected with June revised up also to 0.3% from 0.2%. The annual rates I now 3.2% up from 3.1%.

Also out in the US Friday, the trade deficit was little changed at $55.2bn from $55.3bn in May and $54.6bn expected). The trade data nevertheless highlighted the reduced two-way trade flow between the US and China, with US exports to China down 18% y/y in the first six months of the year and imports from China down 12%. Factory Orders rose by 0.6% against 0.7% expected and the final University of Michigan consumer sentiment index held at the 98.4 preliminary rate.

Finally, commodity markets continue to feel the fall-out rom the tariff news as speculative longs bail out on reduced global growth and Chinese demand prospects. Iron ore futures were down 4.9% and copper 3.5%. On the week, iron ore is 0f 6.8%, steaming coal 6.9% and coking coal 4.9%.

Services PMI numbers today from China (Caixin version) the Eurozone and US. China and Eurozone numbers are seen little changed on last month (Caixin at 52.0, pan-Eurozone at 53) while the US non-manufacturing ISM is seen at 55.5 up from 55.1 in June.

Tuesday seen the RBA and Wednesday the RBNZ, where markets will be flabbergasted if the RBA cuts rate or the RBNZ doesn’t. For the RBA, keener interest will be in Friday’s Lowe parliamentary testimony and the SoMP. China trade numbers are on Thursday

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.