Online retail sales growth slowed in May following a fairly strong April

Insight

Markets have been fairly subdued on the back of soft inflation numbers in the US, and as investors hold off for any revelations from Jerome Powell as he addresses the Economic Club of New York.

https://soundcloud.com/user-291029717/markets-bide-their-time-with-soft-us-inflation-and-a-dovish-riksbank?in=user-291029717/sets/the-morning-call

“Don’t stop, stop, the music; The world will keep turning if you use it, get out there and; Don’t stop, stop, the music; People keep dancing; You can do it; Baby come on”, Rihanna 2007

US core CPI missed expectations overnight, suggesting the potential for a lift in inflation remains theoretical and very much contingent on further stimulus being approved.

Markets though can continue to price reflation given vaccine rollouts, while the Fed and the Riksbank overnight aren’t stopping the music and are ok with inflation above target for some time.

There was little new news on the proposed US $1.9 trillion stimulus package with most political focus on Trump’s impeachment trial.

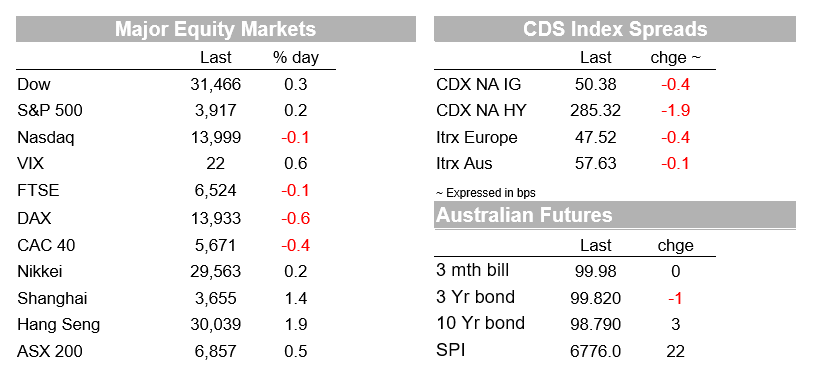

The S&P500 edged into the green, +0.2% after strong gains so far in February (+5.5% over the month).

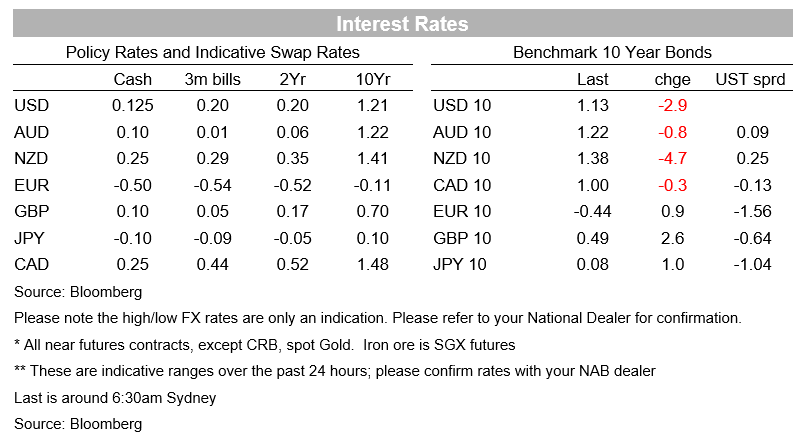

US 10yr yields fell 2.9bps to 1.13%, though inflation breakevens were largely unchanged at 2.20%.

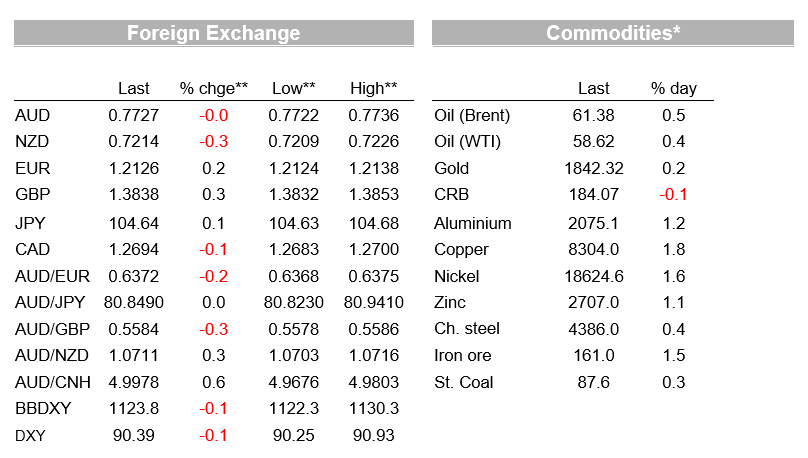

The USD (DXY) fell -0.1% with strength continuing in EUR (+0.2% to 1.2128) and GBP (+0.3% to 1.3840).

Our FX strategists remain a fan of GBP as one of the most under-valued G10 currencies, while the UK vaccination trajectory is better than many other countries. The AUD was little changed at just above 0.77 (currently 0.7729).

The big news overnight was the miss on US Core CPI which came in at 0.0% m/m against the 0.2% consensus, and annualising at 1.4% y/y.

Driving the lower than expected core print was ongoing subdued rents at 0.1% m/m, falls in used car prices (-0.9% m/m), new car prices (-0.5% m/m) and household furnishings (-0.3% m/m), along with a sharp decline in airline fares (-3.2% m/m).

It’s notable that many of the categories that saw higher prices during the later part of 2020 are now reversing. Virus restrictions may be one part, though it is also possible that there has been satiation of some pent-up demand that was focused on the goods side of the economy at the same time that goods production lifts.

For now it seems inflation fears post vaccines are theoretical and dependent on the rollout of further stimulus.

Note Headline CP was in line at 0.3% m/m driven by higher gasoline prices.

Similar themes were echoed in the Chinese CPI data yesterday where Headline CPI missed at -0.3% y/y against 0.0% expected.

The more important core measure excluding food and energy was also -0.3% y/y, though the changing base due to the Lunar New Year being in February this year may have also played a role. The core monthly measure was 0.0% m/m, little changed from last month and still suggestive of little in the way of inflationary pressures. In contrast, factory price pressures are on the rise with the PPI at 0.3% y/y, the first positive read since January 2020 and echoing the higher input prices shown in the PMIs recently. It appears manufacturers are taking this on the chin given subdued core consumer prices.

Chair Powell overnight pushed back on imminent inflation concerns in a speech titled “Getting Back to a Strong Labor Market” (see link). Chair Powell noted that “ employment in January of this year was nearly 10 million below its February 2020 level, a greater shortfall than the worst of the Great Recession’s aftermath” and that the effective unemployment rate was hovering at 10% (well above the current reported 6.3%) when including those who had left the labour force since February 2020. The economy prior the pandemic also showed an ability to sustain a strong jobs market without causing an unwanted increase in inflation.

Chair Powell concluded that policy will need to be accommodative and that the Fed’s new framework implies the Fed “will not tighten monetary policy solely in response to a strong labor market”. After a period of below target inflation “appropriate monetary policy will likely aim to achieve inflation moderately above 2 per cent for some time in the service of keeping inflation expectations well anchored at our 2 per cent ”.

Powell noted that the output gap is hard to estimate in real time, while he does not think pent-up demand will be large enough or sustained to drive sustained inflationary pressure.

Markets are likely to continue to price towards inflation risks given the possibility that the Fed errs on the side of complacency if there is a real surge in inflation.

Sweden’s Riksbank overnight also emphasised the global view that central banks are willing to leave policy accommodation in place for longer, with the greater worry at present around withdrawing monetary support too soon rather than too late. Governor Ingves stated that he’s in “no hurry ” to adjust policy guidance – of keeping the policy rate at zero into 2024. He added that he has no issue with inflation overshooting the target “for a period of time”.

Similar comments were echoed by the RBA Board Member Harper in a Bloomberg interview overnight: “The tendency of this to produce an asset-price bubble is way off where we’re presently headed” and that “There’s still plenty of excess capacity in the economy.” The comments emphasises the RBA is in no hurry to alter its policy package on the basis of asset prices (see Bloomberg interview for details).

Bloomberg reports on the BoJ’s monetary policy strategy review due next month. Officials are reportedly considering ways to communicate that the bank has room to cut its interest rate further below zero. The market currently doesn’t see a bigger move into negative territory as a “live” option, given the potential damage to bank earnings, but the BoJ is said to want to keep that option open.

No data domestically apart from consumer inflation expectations which is unlikely to stir any interest.

NZ has credit card spending for January.

China and some parts of Asia observe the Chinese New Year Holidays with China’s holidays beginning today and going through to Wednesday.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.