Online retail sales growth slowed in May following a fairly strong April

Insight

There’s been a market rebound on the hope that some sort of stimulus deal in the US is still possible before the election.

https://soundcloud.com/user-291029717/markets-bounce-back-on-piecemeal-stimulus-hopes?in=user-291029717/sets/the-morning-call

“Girl, you really got me now; You got me so I don’t know what I’m doin’, yeah; Oh yeah, you really got me now” Van Hallen 1978

Risk sentiment bounced sharply overnight after President Trump surprised markets by tweeting that he would support one-off stimulus for particular sectors, after having earlier shocked markets late Tuesday that he was unilaterally ending stimulus negotiations.

It is still very unclear whether Democrats and Republicans could agree to passing piecemeal stimulus measures, though markets have gone with the sentiment.

Also likely driving is polling suggesting a Democratic clean sweep come November is more probable (Real Clear Politics has Biden 9.4 points ahead nationally and extending leads in certain battleground states such as Florida), which means that even if there was no slimmed down stimulus package, there is a greater chance of a larger stimulus package later.

The Fed Minutes although not market moving, play into the view of the Fed willing to do more if necessary along with a Fed paper that suggests the Fed would need to double QE done to date to ward of a pro-longed U-shape.

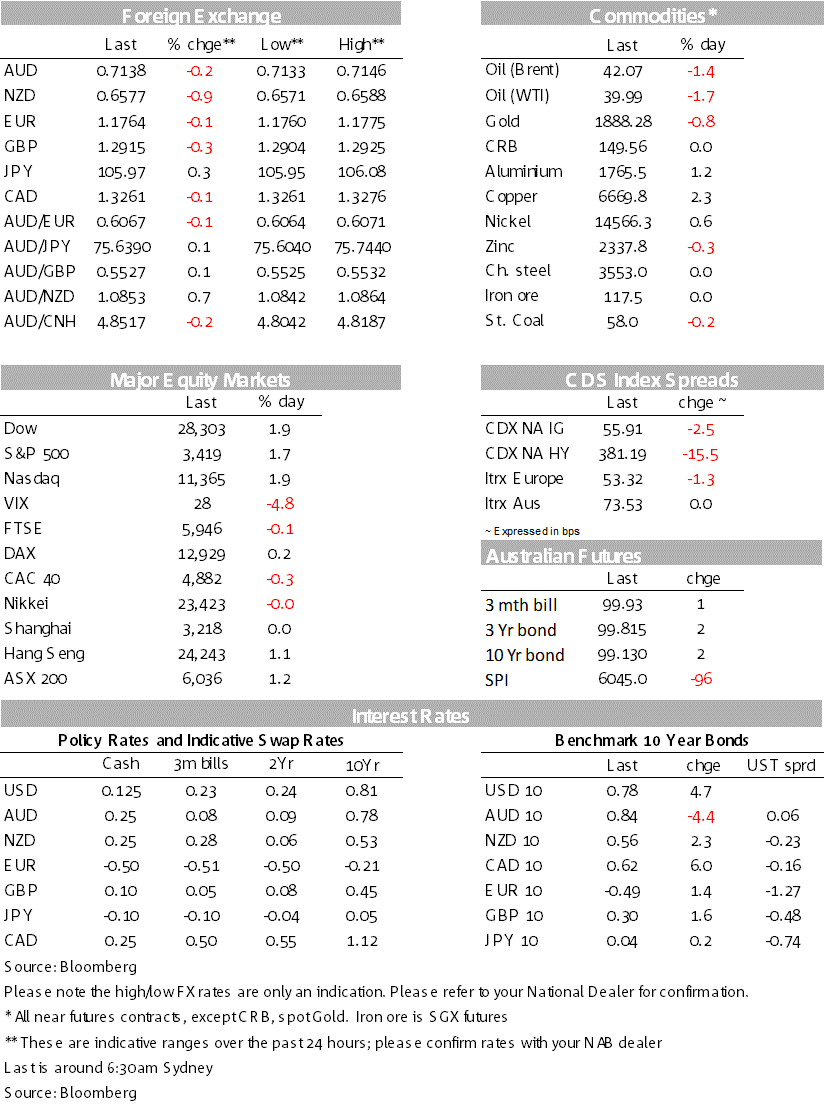

The S&P500 rose 1.7% with cyclicals leading the charge (industrials +2.2%, materials +2.6%, consumer discretionary +2.5%). The NASDAQ also lifted 1.9% despite some concern that big tech could face stricter antitrust laws under a Biden Presidency after the US House Antitrust Subcommittee released a report saying tech dominance has stifled competition. Meanwhile, yields have reversed Tuesday’s moves with US10yr +4.8bps to 0.78%. The USD (DXY) has also fallen -0.2%, reversing around half of the appreciation yesterday. Oil in contrast is lower with Brent -1.4% after US crude inventories rose 500k last week.

He said he would support a one-off bill for another round of $1,200 stimulus checks to US households, along with targeted stimulus for the airline industry ($25bn) and US small businesses ($135bn for the paycheck protection program), with unused funds from the CARES act. (full tweet for the record: “If I am sent a Stand Alone Bill for Stimulus Checks ($1,200), they will go out to our great people IMMEDIATELY. I am ready to sign right now. Are you listening Nancy?”).

Democrats are opposed to a piecemeal approach to stimulus because it reduces their leverage in negotiations, in which they are trying to convince Republicans to provide more funding for state and local governments. White House economic advisor Larry Kudlow told CNBC that the chances of one-off stimulus bills passing was “probably….low probability stuff.” House Leader Pelosi also played down the prospects for agreement, stating “it’s hard to see any clear, sane path in anything that he’s doing.”

While not market moving, hints that the Fed is willing to do more if necessary and opens the door to post-election easing if necessary. Note this nuance did not come across in Powell’s post-meeting press conference nor in recent speeches. The Minutes noted that “many” participants had “assumed additional fiscal support and that if future fiscal support was significantly smaller or arrived significantly later than they expected, the pace of the recovery could be slower than anticipated.” “Some” also thought it would be appropriate to “further assess and communicate how the Committee’s asset purchase program could best support…maximum employment and price-stability goals.” (see Minutes for details).

It’s worth noting that the Fed’s Mester on Monday said she might support shifting asset purchases to more longer-dated bonds. A Fed paper modelling a policy response to an output shock of 10% finds that when rates are near zero, a sizable QE program an help prevent a prolonged U-shaped recession. The paper modelled that a QE program that amounted to $6.2 trillion (or 30% of GDP) would help support a recovery. Note Fed purchases to date amount to around $3.0 trillion (see Fed paper for details).

Brexit negotiations continue ahead of the key October 15 EU Summit. Bloomberg reported that the UK was prepared to walk away from trade negotiations (i.e. prepare for a ‘hard Brexit’) if there was no clear “landing zone” for a deal at the Summit. Negotiators remain stuck on the issues of fishing rights and state aid amid reports earlier this week that the EU was not prepared to make compromises ahead of the Summit. Despite the uncertainty, GBP has been relatively stable and rose 0.2% alongside US dollar weakness to around 1.2914. The EUR up a similar amount overnight, to around 1.1764.

While most currencies have gained against the USD over the past 24 hours, except the safe-haven JPY, the NZD has underperformed notably. The NZD broke below 0.66 yesterday morning, after Trump’s tweet that he was calling off fiscal stimulus talks, and it has stayed down, despite the USD weakening and equity markets recovering. The NZD is trading around 0.6575 this morning, down 0.2% on the day, and has lost ground on all the key crosses, except NZD/JPY. The AUS/NZD has also risen 0.6% to 1.0851, though with little obvious catalyst for NZD underperformance. The AUD itself is up 0.6% from the lows of yesterday and currently trades at 0.7138.

A quiet day domestically with nothing of note scheduled.

Across the Ditch, the ANZ Business Survey will dominate and further afield China has the Caixin Services PMI – though China itself remains out given the Golden Week Holidays that run October 1-8.

US Jobless Claims will continue to set the tone given a slowing in the pace of recovery as stimulus measures fade, while there are a number of central bank speakers including the BoE’s Bailey and Fed’s Rosengren and Bostic. For more details, please see below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.