Asset finance and leasing is in a growth phase in Australia as organisations seek a capital-effective way to modernise and upgrade across a broad range of asset classes and industries.

US equities are on the rise as markets brush off concerns over the lack of progress on US China trade talks

https://soundcloud.com/user-291029717/markets-brush-off-all-yesterdays-news-rba-cut-expected?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s research support please let your company’s representative know.

It’s like I flicked a switch and now I’m feeling good (Bounce), No way to stop it, now you wish that you could (Bounce) – Calvin Harris

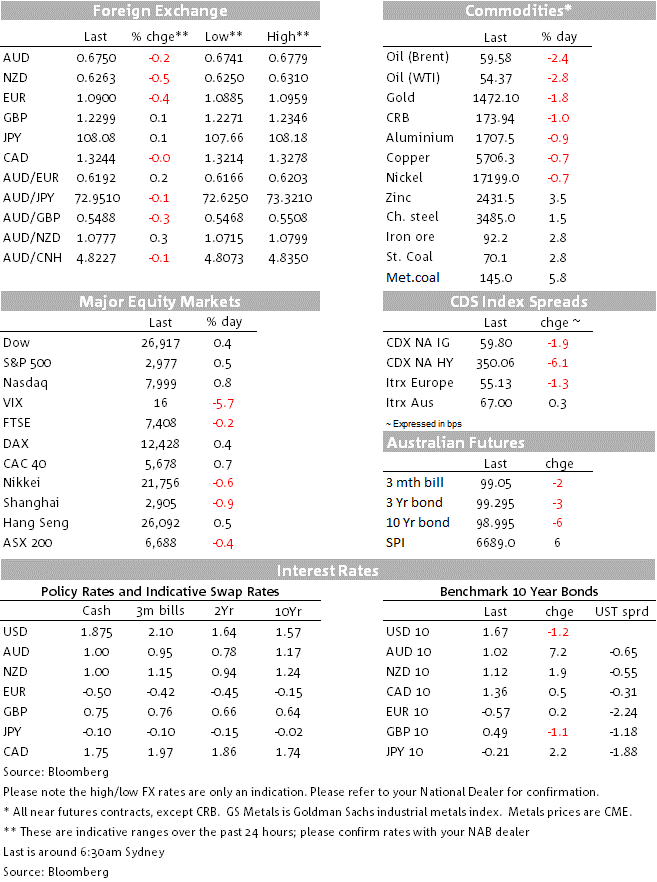

US equities continued their late Friday recovery closing the third quarter on a positive note. Sentiment was boosted by a weekend statement from the US administration denying plans to restrict US investments into Chinese companies. Core global bond yields were little changed while the USD strengthen again with the euro and kiwi the big overnight underperformers. Ahead of the ISM manufacturing tonight, US regional PMI underwhelmed and German data did little to change the dire picture in Europe.

The big news from the overnight session has been the recovery in US equity markets, following Friday’s decline on the back of a Bloomberg report suggesting the US was considering imposing restrictions on US investments on Chinese companies. Over the weekend the Trump administration issued a denial, saying “The administration is not contemplating blocking Chinese companies from listing shares BounceU.S. stock exchanges at this time,”.

The fact that the denial was not absolute in nature didn’t seem to trouble investors with major US equity indices closing the day in positive territory (S&P 500 +0.50%, Dow +0.36% and NASDAA +0.75%). The good news not only helped major US equity indices closed the month in positive territory (S&P 500 +1.72%, Dow +1.95% and NASDAA +0.46%), it also means that much of the August losses have now been reverse with the Wall Street Journal noting that the S&P 500 is now up close to 19% year to date its best performance in the first three quarters of a year since 1997.

On the other side of the Atlantic European equities also had a solid end to September with all regional indices up on the last day of the month, except for the FTSE 100 (-0.24%). Looking at the monthly returns, European equity markets had an even better month than their US counterparts up between 3% and 4.5% with the FTSE 100 the laggard up 2.79%.

The Nikkei has led the charger, up 5.08% in September ( down 0.56% overnight) while the Chinese equities ended the month in a sour note, sown almost 1% and closing the month with relatively modest gains between 0.66% and 1%.

UST curve is about 1bps lower in an almost parallel fashion with the 10y note closing the month at 1.6646% while in Europe 10y Bunds closed at -0.5710% (unchanged on the day). Overnight data releases were mostly on the soft side. Germany’s unemployment printed unchanged at 5%, but inflation in September slipped one tenth to 0.9. Meanwhile in the US, the Chicago PMI fell to 47.1 in September from 50.4 in August, below the 50.0 consensus and the Dallas Fed survey fell 1 from 2.7 in August. Looking at the month of September and bearing in mind the large declines in August, core global yields ended higher with the UST yields leading the move up. 10y bunds closed 12.9bps higher while 10y UST yields ended 17.8bps higher on the month.

So bearing in mind a picture where the US economy is still faring better than other majors (relative to their potential) and a month where UST yields have effectively increased their differential against other core global yields, then is should be little surprise to see the USD closing the month stronger against most pairs. On the day DXY (@99.40) and BBDXY (@1218.84) indices climbed 0.27% and 0.21% respectively and gained 0.47% and 0.18% on the month.

The euro and kiwi were the underperformers overnight with the former seemingly affected by the soft German CPI and reports a Reuters report that Germany’s leading economic institutes revised down their growth forecast to 0.5% this year. EUR now trades at a new year to date low of 1.0898 ( down 0.36% on the day and 0.80% on the month).

The NZD has underperformed over the past 24 hours and it is the second weakest currency in the G10 (above only the Swedish krona), down 0.6%. The headline business confidence reading in the ANZ survey fell to its lowest level in 11 years, with the RBNZ’s larger-than-usual 50bp OCR cut in August having failed to provide any lift to confidence (perhaps unsurprising given that businesses have a long list of concerns and interest rates are well down that list). This morning the NZ Q3 Business Confidence index (QSBO) didn’t do much to alleviate the concerns over the state of NZ business confidence with the headline index falling to -40 vs -34 in 2Q while the Own activity index fell to -11 vs -4 previously. All up, the QSBO survey is consistent with yesterday’s ANZ survey, with the RBNZ’s shocking August 50bps cut not supporting confidence but seemingly startling businesses instead. Although the counterfactual would suggest things could have been worst had it not been for the RBNZ rate cuts. Still the surveys suggest a period of sub-trend growth ahead lies ahead for New Zealand. NZD now trades at 0.6263, afte trading down to a ytd low of 0.6250 overnight.

The AUD had a relatively quiet night trading down to a low of 0.6741 and now it trades at 0.6750, 0.19% lower on the day, but 0.27% higher on the month. The RBA policy rate decision is the focus today, followed by the Governor speech tonight. We expect the Bank to lower the cash rate by 25bps this afternoon to 0.75%, but it is likely that Statement and Governor speech sounds relatively neutral, so there is a risk the AUD could trade higher this time tomorrow, particularly if the Governor chooses to emphasise the message that the economy may be at a “gentle turning point” ( more below)

We expect the RBA to cut the cash rate by 25bp to 0.75% today. This reflects our view that an underperforming economy requires more policy support, with Governor Lowe stating there had been “an accumulation of evidence” that unemployment can be lower and stressing that ignoring lower world rates would see a higher exchange rate. We expect the press release and comments from the Governor tonight will justify the decision, but not offer any guide to future moves, other than to say that rates are likely to stay low and that the Board will monitor developments to see if further easing is needed. The RBA commentary could also repeat that the economy may be at a “gentle turning point”.

Building approvals should post a modest rebound after last month’s steep fall. We forecast a 1.5% gain in total residential approvals August, following July’s sharper-than-expected fall of 9.7% (consensus: 2.0%). Apartment approvals likely rose moderately after the sharp 20% fall last month, while we expect another small decline in house approvals.

The Tankan Large Manufacturing Index is expected to drop from 7 to 2, if so this would be a sharp deterioration in business conditions. Meanwhile the non-manufacturing sector is expected to remain relatively buoyant with a headline index at 20, 3 points lower than the Q2 reading. Market focus is also likely to be on the outlook readings for both sectors ahead of the BoJ’s review at its next meeting late in October. Capex intentions and FX forecasts by large manufactures are also going to be a market focus.

Japan’s jobless rate is expected to have ease by one tenth to 2.3%.

The picture from regional manufacturing surveys is a mixed one, but the consensus view is for the September Manufacturing ISM to reveal a reading back above expansionary mode after dipping below the 50 even level in August.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Asset finance and leasing is in a growth phase in Australia as organisations seek a capital-effective way to modernise and upgrade across a broad range of asset classes and industries.

Growth in the major advanced economies bounced back in Q2

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.