A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

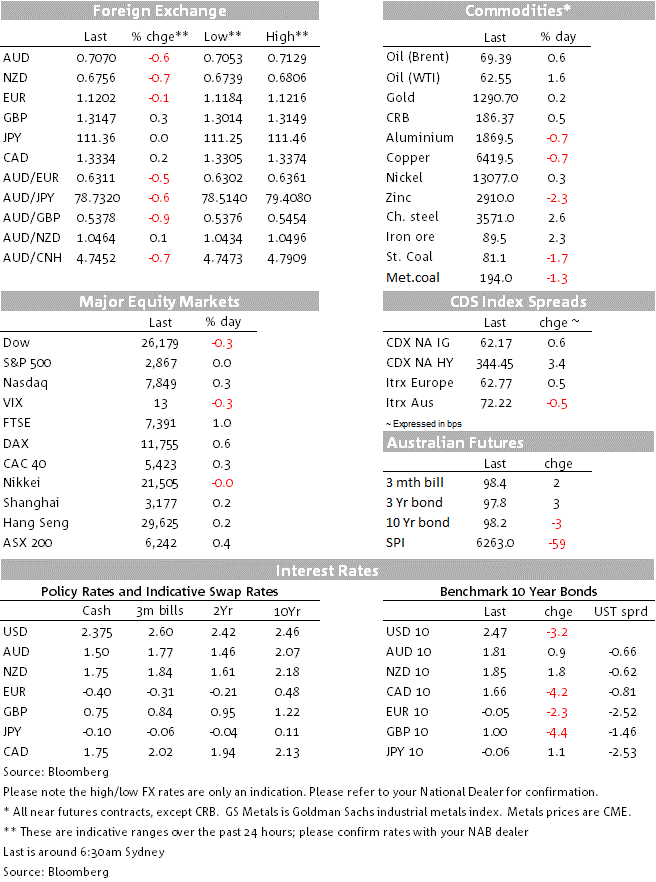

The markets are a lot calmer after yesterday’s rally in shares and sell-off of bonds. And the Kiwi and Aussie dollars have taken the biggest hit out of the major currencies.

https://soundcloud.com/user-291029717/markets-calmer-aussie-takes-a-hit-theresa-reaches-out

It has been a relatively quiet night for markets.US equities began the session on the back-foot, but have closed the day just above positive territory, marking a fourth consecutive day of positive returns. After yesterday’s sell off, UST yields have steadied overnight and the USD is a tad stronger largely reflecting NZD, AUD and CAD weakness. As is normally the case, the Australian budget presentation elicited little reaction in the AUD or Aussie bond futures. The new budget effectively marks the start of the 2019 election campaign.

US equities didn’t have a good start to the overnight session with an earnings warning from retailer Walgreens not helping the cause. In the end however gains in IT and Communications were more than enough of an offset to the decline in consumer staples. European equities had a decent night with carmakers leading the gains despite concerns over US-EU trade talks amid speculation of an impasse on climate change.

After yesterday’s big sell-off in UST yields which saw 10y UST yields climbed 10bps, it has been a relatively calm overnight session with yields drifting lower across the curve. 10y UST yields now trade at 2.47%, 2.7bps lower relative to yesterday’s level while the 2y rate is at 2.30%, down 3bps.

The USD dollar is a tad stronger largely reflecting commodity linked currencies’ weakness. In index terms DXY and BBDXY are still very close to the top of their ranges held since mid-2017. A look at the G10 currencies leader board reveals much of the USD strength has come from NZD, AUD and CAD domestically driven weaknesses. That said it’s probably worth highlighting that although the euro is only 0.14% lower, Brexit uncertainty against a soft EU economic backdrop has the currency under pressure with the pair trading to an overnight low of 1.1185. The currency now trades back above the figure, support around 1.12 continues to be tested, but from a technical perspective there is a lot of thin air below this key support.

After yesterday’s dovish RBA statement the AUD has continued to drift lower overnight and now trades at 0.7069, after trading to an overnight low of 0.7053. Two changes in the Statement left the sense of a dovish tilt. The Bank has acknowledged for the first time that the housing downturn is weighing on consumption and we also got a re-write of the final paragraph for the first time in ages. The RBA deleted language about holding the stance of monetary policy. In its place, the bank “will continue to monitor developments and set monetary policy to support sustainable growth”, which the market has interpreted as a nod to being open about considering future rate cuts. A full 25bps cut is priced by August.

Yesterday the NZD fell after the QSBO survey which showed weaker confidence and activity indicators and continued to drift lower overnight before finding some support around 0.6750 mark. The GDT dairy auction showed a smaller gain in prices (+0.8%) than expected, but the price index continues to trend higher. Whole milk powder prices fell by 1.3%.

Rounding off a bad day for commodity currencies, CAD weakened after a report that home sales in the metro Vancouver region fell to the lowest March levels in over three decades – some 46% below the 10-year March sales average and with prices down 7.7% yoy. Domestic concerns are weighing on the currency even with oil prices continuing to trend higher, reaching a four-month high, supported by declines in OPEC production and Venezuela output falling. The threat of additional US sanctions is hanging over Iranian supply – the White House is expected to decide early May whether to extend waivers allowing some countries to keep buying oil from the rogue nation.

GBP fell yesterday morning after parliament voted down all measures designed to break the Brexit impasse. The pair traded to an overnight low of 1.3014, before embarking on a complete reversal after PM May announced a plan to work with the Labour party and look for a “single, unified approach” to Brexit and accept that the government will abide by parliament’s decision. This might raise hope for the “customs union” solution, a softer Brexit than May’s plan, which the Labour party supports and which only lost by 3 votes yesterday. It remains unclear whether the two parties can find a compromise, early this morning Labour’s leader said “We recognize that she has made a move, I recognize my responsibility.”

Last night, the Australian Budget came and went with little surprise or market reaction. The budget is forecast to be in surplus in 2019-20 for the first time since GFC. Income tax offsets and energy assistance payments are expected to be approved by Parliament this week. The budget effectively marks the beginning of the 2019 election campaign The media reports the election will be announced on Friday, where the Prime Minister supposedly told his MPs that he hadn’t decided between 11, 18 or 25 May – see our economists’ budget analysis for more details.

We think retail sales data are likely to paint a weak picture for consumption in Q1. A weak rise in sales in February (NAB: 0.2%; mkt: 0.3%) would confirm two out of three months of softness in the March quarter

ISM Non-Manufacturing Index is expected to print at 58, down from 59.7 in February – So down to a still pretty health;y level from a roar and not sustainable level.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.