Long-term signal vs. Short-term noise

Insight

There’s a strong risk-on mood in the markets this morning.

“I’m burnin’ through the sky, yeah; Two hundred degrees; That’s why they call me Mister Fahrenheit; I’m traveling at the speed of light; I wanna make a supersonic man out of you; Don’t stop me now, I’m having such a good time”, Queen 1978

Risk sentiment continues to surge as activity lifts following the gradual easing of containment restrictions around the word, while vaccine hopes remain high with 10 different vaccines currently at the human trial stage – the latest being Novavax in Australia. Playing into hopes of a sharp lift in activity, the Fed’s Bullard noted “the third quarter very likely, right behind the worst quarter, will be the best quarter of all time on the growth perspective.” (see FOX Business interview). Also adding to sentiment is some notion that widespread lockdowns are unlikely to be repeated (at least in the US) with research showing little correlation between the restrictiveness of lockdowns and virus transmission, while the easing of lockdowns so far has seen little pick-up in the rate of transmission (the hypothesis being people are smart enough to self-isolate and not everyone needs to isolate to reduce transmission). A late report of the US administration considering sanctions on Chinese officials regarding Hong Kong though did see some moderation in sentiment towards the close.

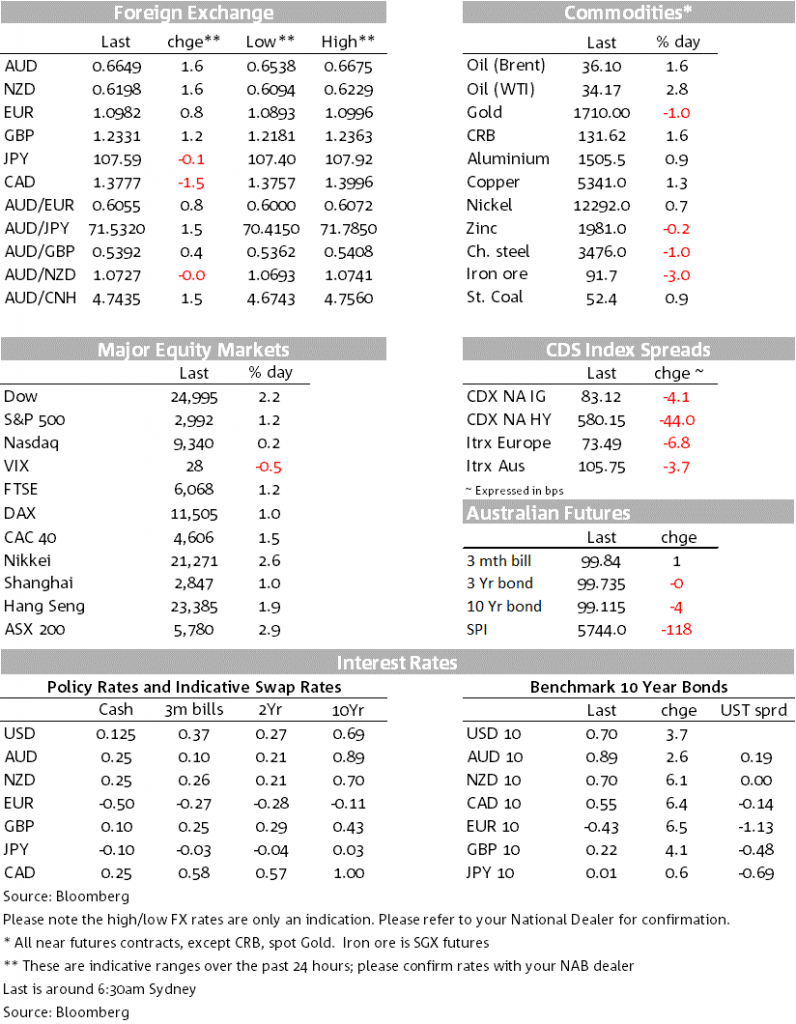

Equities surged with the S&P500 +1.2% to 2,992. The S&P500 looked to be set to close above 3,000 until the late headline that the US was considering a range of sanctions on Chinese officials and businesses should China go ahead with its legislation regarding Hong Kong. The extent of those possible sanctions is uncertain but the White House press secretary did say President Trump is “displeased” and that “it’s hard to see how Hong Kong can remain a financial hub if China takes over.” The comments come after Chinese Official media played down the prospect of US actions (calling it a “nothingburger”) and that any US action on Hong Kong would hurt US multinationals.

Global growth/commodity FX retained their strong lift with the AUD +1.7%, NZD +1.6% and USD/CAD -1.5%. Highlighting the risk-on mood both the USD (DXY -0.8% to 99.00) and Gold fell (-1% to $1,710), while USD/Yen was broadly flat (-0.1% to 107.59).

The other major pairs were also sharply higher with EUR +0.8% and GBP +1.2%. Helping out GBP was some backtracking on the prospect of negative rates in the UK with BoE Chief Economist Haldane stating: “reviewing and doing are different things and currently we are in the review phase, and have not .. reached remotely yet .. the doing”. Bank profitability and willingness to lend is a worry under negative rates (“What will the consequences be of a further lowering of rates into negative territory for the financial sector? We would expect that to cause some squeeze on the margins between their lending and deposit rates”). For the EUR, the EU pandemic fund looks closer to getting off the ground with the European Commission set to unveil its proposal on Wednesday. An MNI sources report quoted one official stating “There’s quite a lot of important symbolism around the recovery fund proposal, I don’t think the objections from The Four can stop that” and that there may be some tweaking of grants/loans and conditionality to get the frugal four across the line (note frugal four being Netherlands, Austria, Denmark and Sweden).

Though not hugely so in the US where 10yr yields are +3.7bps to 0.69%. In contrast, Gilts and European bond yields have lifted a little more, likely tied to some downplaying of negative rates by the BoE, and reports of recovery in Germany where there are plans to lift travel warnings for 31 European countries.

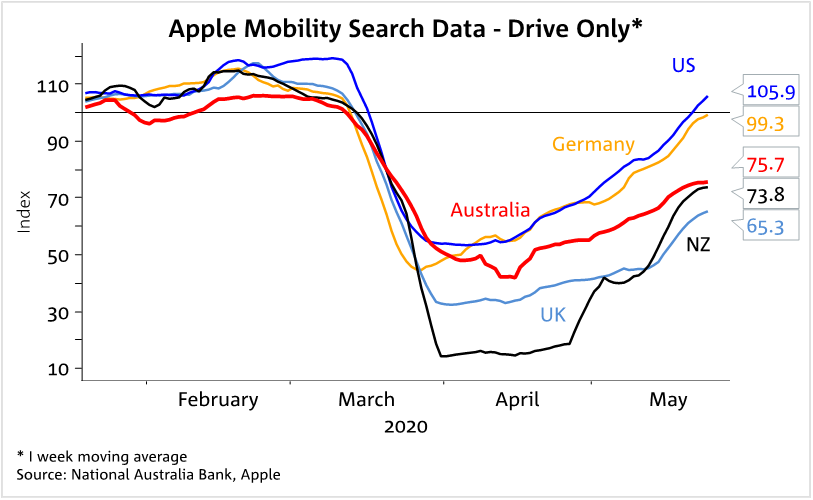

On hopes of activity picking up following rollback, softer survey data in the US is starting to bottom out and turn. The Dallas Fed Manufacturing index was a lot better than expected at -49.2 from -73.7 and -61 expected. Notably the New Orders index rose 38 points to -30.6, its highest reading in three months, with more than 20 percent of manufacturers noting an increase in orders. Employment also looks to be turning a corner with the Employment index rising to -11.5 from -22.0 to -11.5 with eight percent of firms saying they are going to increase net hiring. The Conference Board Consumer Confidence Index also rose to 86.6 from 85.7, broadly as expected (consensus 87.0), and its also worth noting confidence has fallen by a lot less than during the GFC. The WSJ also ran a piece noting a number of high-frequency data points were lifting, while Apple Mobility searches for driving directions are at pre-pandemic levels now (see chart below).

Weekly Consumer Confidence rose has now risen for eight consecutive weeks. Foot traffic is picking up with GPT reporting in its portfolio that foot traffic is now around 75% of where it was at the corresponding period last year for most centres – note it was 65% two weeks ago and is up from 50% in April (see AFR for details). Major banks are also reporting a pick-up in credit and debit card transactions with ANZ reporting spending is up 2.3% on the same week last year and for CBA its 4% (see AFR for details). Spending is likely to increase further as pent-up demand is satiated following the gradual lifting of containment measures – though some caution should be noted around the figures given the low level of cash transactions likely occurring.

There are now ten currently in human trials which should lift the probability of finding a successful vaccine. Novavax is the latest starting human trials (this one in Australia). The CEO of Merck was the latest casting some doubt on a timeframe, stating the 12-18 month timeframe to develop an effective COVID19 vaccine is “very aggressive” and “it is not something I would put out there that I would want to hold Merck to”, adding that vaccines should be tested in “very large” clinical trials that take several months if not years to complete.

Domestically Q1 construction figures will be watched closely as a pre-GDP partial (note Q1 GDP is out on June 3), though for markets the data will likely be seen as dated. Elsewhere it is relatively quiet with only Chinese Industrial Profits, ECB’s Lagarde and the Fed’s Bullard/Bostic of note. Key releases in detail:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.