Price growth edges lower despite reasonable economy

Insight

Again, it seems markets are ignoring the bad data of which there’s plenty.

“I just can’t; I just can’t; I just can’t control my feet”, The Jacksons, 1978

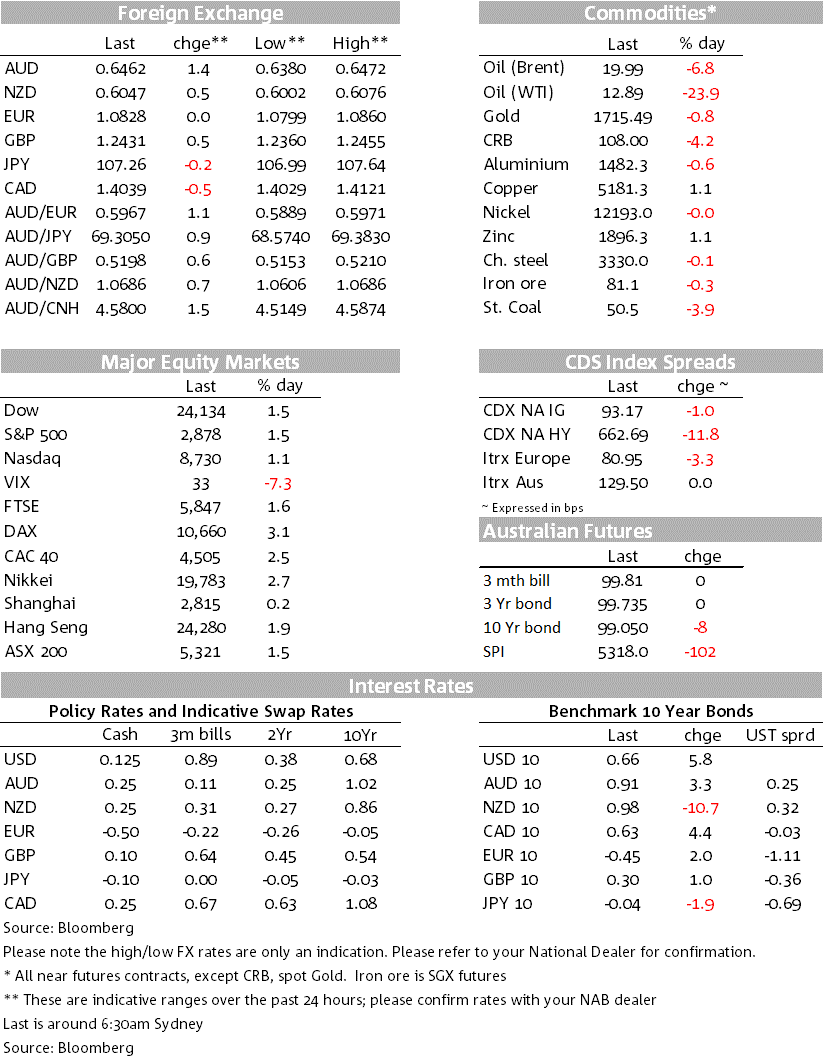

Optimism remains the catchcry of markets with risk assets rallying overnight, while Deutsche Bank’s earnings beat also helped financials outperform. Equities are up with the S&P500 +1.5% and is up 28% from its late March low. Yields also rose with US 10yr yields +5.7bps to 0.67%. In FX the global growth proxies rallied led by the AUD up an impressive 1.4% to a high of 0.6472 (currently 0.6462) on what seemed to be little new news apart from WA and QLD easing up on restrictions. An MNI sources added to the optimism, noting the “RBA is increasingly confident that the domestic economy will recover more quickly than initially expected from the coronavirus-driven downturn” and that “Australia’s relative epidemiological successes allowing an earlier return to normal economic activity”. Gains in the Aussie helped drag the Kiwi higher with NZD +0.5%. With risk rallying, the USD (DXY) was on the backfoot -0.3%, though was mixed with EUR 0.0%, GBP +0.5%, USD/Yen -0.3% and USD/CHF +0.3%. The flat EUR appears to be driven by speculation amongst a minority of economists that the ECB could boost its QE program this week. Oil bucked the positivity with WTI June -23.9% with the US Oil ETF stating it will roll its June exposure over the next four days.

Most of the gains occurred during the Asian timezone with liquidity thinner than usual given the NZ public holiday. While no single driver, the move reflected growing optimism that containment restrictions will be lifted in Australia come May 11 with WA and QLD announcing an easing in restrictions on Sunday. There is also a notion that Asia has controlled the virus more effectively than the US and Europe – Hong Kong has seen no new cases over four over the past eight days; Taiwan has seen no locally transmitted cases for 15 days and NZ declared victory on Sunday. An MNI sources piece last night also played into that view with the RBA “increasingly confident that the domestic economy will recover more quickly than initially expected from the coronavirus-driven downturn” and “Along with China, South Korea, Taiwan and New Zealand, the RBA sees Australia’s relative epidemiological successes allowing an earlier return to normal economic activity…[and] sets up the Asia Pacific region for a more rapid recovery, fuelled by China…”.

The Bank of Japan (BoJ) said it would make its Japanese government bond purchases ‘unlimited’ and more-than doubled its limit on corporate debt purchases (to ¥20 trillion, ~US$185b). The change to an ‘unlimited’ government bond QE programme is purely symbolic because the BoJ operates a 10-year yield target of 0% and it has already committed to buying unlimited quantities of bonds to enforce that target. It has finally gotten rid of its previous ¥80 trillion annual ‘target’ for government bond buying, which it has fallen well short of for several years now. Tellingly, the BoJ again chose not to cut rates to more negative levels, a sign that it views the side-effects of such a policy as outweighing the benefits. The BoJ also chosen not to increase its equity purchases (via ETFs). There was little impact on Japanese government bond yields while the JPY appreciated slightly, suggesting the market was underwhelmed by the policy measures.

The Fed and the European Central Bank (ECB) have their own monetary policy meetings this week. A minority of economists expect the ECB to boost its QE programme this week and the market also pricing in around a 30% chance of an ECB rate. The ECB announced last week that it would accept bonds from issuers downgraded to high-yield (so-called ‘fallen angels’) as collateral in its operations until at least September next year. That could be a precursor to the ECB announcing this week that it will also buy these downgraded bonds as part of its QE programme (which would bring it into line with the Fed). Recent ECB action has been a key reason for Italian debt to rally (overnight 10yr BTP yields -7.8bps) with S&P noting “The ECB’s current financing backstop enables Italy to refinance its debt at real interest rates of around 0%,” “In nominal terms, and absent a significant deterioration in borrowing costs, Italy will pay less to service its total debt stock this year and into 2021-2023, than it paid in 2019.” Also being mooted in Europe is some easing of bank capital relief with a possible announcement on Tuesday.

Data continues to take a back seat with China’s industrial profits largely ignored by markets yesterday. For the record profits fell -34.9% y/y in March, a slower pace of decline than the 38.3% y/y fall in the Jan-Feb period. Looking forward, it is hoped profitability will improve given a further pick-up in industrial activity as seen in high-frequency indicators such as geosatelite imagery, air pollution and traffic congestion. A pick-up in infrastructure and fixed asset investment should also help. Nevertheless, industrial profits are likely to remain under pressure given an uncertain global demand environment and doubts over the strength of the Chinese consumer.

US data was also largely ignored with only the Dallas Fed Manufacturing Survey at -73.7 v. -75e and -70 previously of note. Weak prints in US data are to be expected given the scale of the lockdowns and it seems the US Administration is preparing markets for a very weak jobs report in May. Kevin Hassett yesterday noted “The unemployment rate for the first week of May, we’re going to see a number that’s going to be 16, maybe 17%…for second quarter GDP it’s going to be the biggest negative number that we’ve seen since the Great Depression”.

Reports of more US states easing lockdown restrictions also helped buoy risk assets overnight even as earnings season has seen earnings down by 22.7% in aggregate according to Factset’s tracking of the 122 S&P500 companies to have reported first-quarter numbers. US states of Georgia, Oklahoma and Alaska have started loosening restrictions and Texas has announced it will also loosen from Friday. Treasury Secretary Steven Mnuchin said he expected the U.S. economy to bounce back in the months after June, once the lockdowns are dismantled.

Oil continues to come under pressure with WTI -23.9% and Brent -6.8%. The moves were driven by an announcement of the US Oil ETF that it was going to start rolling its exposure to the June contract over the next four days and buy from July 2020 to June 2021. More specifically the fund has said it will invest approximately 30% of its portfolio in July contracts, 15% in August, 15% in September, 15% in October, 15% in December and 10% in June 2021.

A very quiet day data wise with little domestically apart from weekly consumer confidence. International focus will be on earnings with Alphabet and Caterpillar reporting (amongst others), while the last of the US pre-GDP partials are out including the trade balance and inventories (Q1 GDP is out on Wednesday with the consensus at -3.9% annualised).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.