Online retail sales growth slowed to almost flat in March

Insight

The markets attempted a bit of a rebound earlier but it hasn’t lasted long.

https://soundcloud.com/user-291029717/markets-grab-a-short-breather?in=user-291029717/sets/the-morning-call

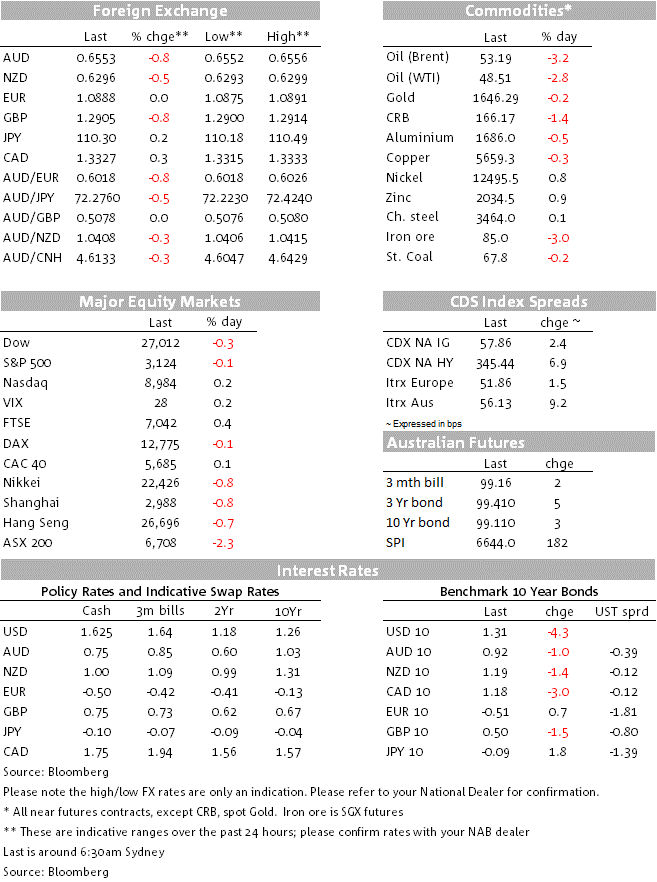

Markets remain cautious over COVID-19 amid reports of further cases internationally. There has been little data of significance and markets are largely trading on news headlines. Equities initially opened in the green by some 1.7%, but have more than fully reversed with the S&P500 -0.1% 3,124. Yields also continued to trend lower with US10yr Treasury Yields ‑1.5bps to 1.3%. The AUD remains the favourite whipping boy, both as a China and a global growth proxy, with the AUD -0.7% to 0.6557. The other big G10 FX mover was GBP -0.8% to 1.2912 and reversing yesterday’s gains. The USD (DXY) is up 0.1% with EUR steady and USD/YEN +0.3%.

National health authorities are becoming more concerned about the spread of the virus: German Health Minister Spah stated Germany was now looking to be at “the beginning of a coronavirus epidemic”, while the US CDC said “it’s not so much a question of if this will happen anymore, but rather more a question of exactly when this will happen and how many people in this country will have severe illness”. Overnight Brazil, Greece and Macedonia confirmed new cases with an increase in cases in Italy, Iran and South Korea. Even with the mortality rate being on the low side of recent virus outbreaks, the potential for the virus to strain health systems remains considerable.

Interestingly, the World Health Organisation (WHO) notes that the rate of new infections seems to be slowing in China, while it is rising in the rest of the world. Indeed the WHO found that the epidemic peaked and plateaued between the 23rd of January and the 2nd of February and provides some hope that containment measures could help stem the spread of the virus. In that context China has started implementing travel restrictions from a number of countries into China to prevent re-infection. Despite fears of a pandemic, a pandemic has not been called, with the WHO noting that China has fewer than 80,000 cases in a population of 1.4bn and in the rest of the world there are 2,700 cases in a population of 6.3bn.

Central bank rate cut pricing has extended further with 2.7 cuts now priced for the US Fed by the end of the year (up from 2.4 previously). RBA pricing has also extended with April now moving close to 50% chance of a cut and 1.6 rate cuts priced by the end of the year (up from 1.5 previously). Governments are also drawing up fiscal stimulus plans to offset the economic impact of the virus with Hong Kong drawing up plans worth over 4% of GDP (including cash handouts to permanent residents), while German press report Germany plans to temporarily suspend the limit on public borrowing.

Signs are also emerging of China gradually getting back to work with traffic congestion and pollution levels starting to rise. TOMTOM notes that traffic congestion in Shenzhen is now around 6-8% below the levels they were this time last year, a vast improvement from last week when it was 48% below 2019 levels. Shanghai is also seeing a pickup in traffic, though congestion data is still running 20-25% below this time last year. The length of time for activity to pickup in China will be very important in terms of how long global supply chains could be impacted.

Australian Q4 construction data yesterday had little impact on markets given COVID-19 is dominating market sentiment. The figures themselves though suggests downside risks to Q4 GDP figures out next Wednesday with the private investment components down -4.2% q/q and dragging some 0.4%points of Q4 GDP.

All focus will continue to be on COVID-19 and its emerging spread. Domestically the Capex survey is out where downside risks to the consensus are likely after yesterday’s weaker than expected construction figures. Also be on the alert for the government to soften up travel bans with the AFR reporting the travel ban may be eased for Chinese students with the government fearful of the impact of the virus on economic growth (see AFR for details). Across the Ditch, the ANZ Business Survey for February will be closely watched for possible COVID-19 impact on business sentiment, while in the US the most significant piece is Durable Capital Goods Orders with downside risks given the woes at Boeing.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed to almost flat in March

Insight

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.