Total spending grew 0.9% in June.

Stocks, currencies, bonds and commodities have all felt the impact as China responds to US tariffs.

https://soundcloud.com/user-291029717/markets-hit-as-china-bites-back?in=user-291029717/sets/the-morning-call

We only communicate when we need to fight, But we are best friends right? – Amy Winehouse

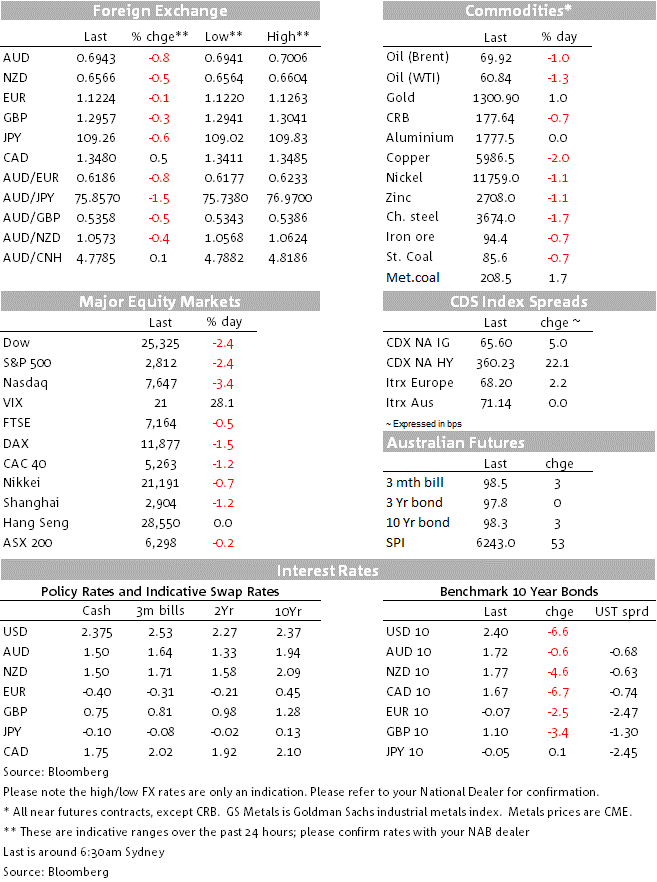

Following last week’s US decision to lift tariffs on $200bn worth of China imports, China has retaliated by increasing tariffs on $60bn of US imports by up to 25%. The news triggered a broad sell-off across equities, commodities and risk sensitive currencies including the AUD and NZD. Core global yields rallied with shorted dated UST yields leading the decline. The 3m-10y UST curve, a US recession barometer, briefly inverted overnight and now a Fed rate cut is more than fully priced for December. Late in the session, President Trump confirms his intentions to meet President Xi at the G20 late in June, helping arrest US equities decline.

Although a retaliation by China was expected, news that China intends to lift tariffs on $60bn of US imports by between 10% to 25%, with more than half the goods subject to the higher tariff rate, triggered a sharp sell-off in equities. Early in the session, European equities opened lower, taking on the negative lead from Asia, but China’s retaliation news around 10 pm Sydney time accelerated the decline. US equities opened sharply lower with the S&P 500 down to 2.77% at one point before pairing some losses a couple of hours before the close following comments from President Trump suggesting that he would meet President Xi at the G20 Osaka summit late in June.

Tech shares have led the decline in US equities with the NASDAQ index down 3.41% while the IT sector in the S&P 500 index closed -3.71%. The Utilities sector in the S&P500 was the only sector that managed to record positive returns (1.11%), reflecting a shift in demand for non-cyclical stocks as the market ponders the economic impact from the escalation in US-China trade tensions.

The VIX index closed last week at 16.15 and now it is back above 20 reflecting the increase in market anxiety. Meanwhile simmering in the background, the May 18th deadline for President Trump to decide on EU and other countries auto tariffs is approaching fast and last night EU Trade Commissioner Malmstrom said the bloc was working on a list of €20bn worth of goods that would be subject to retaliatory tariffs in the event the US chose to go ahead with its tariff threat. President Trump has the ability to extend the deadline for another 180 days, but at this stage it is unclear whether he has the appetite to escalate his trade war on two fronts.

In currency land, the USD has had a volatile session but it is essentially unchanged in index terms. The initial reaction to China’s retaliation news saw the big dollar move sharply lower with the euro, JPY and CHF the main beneficiaries. Gains in the euro, however (overnight high 1.1263) proved to be short lived, the unwind of EM carry trades may have been a supporting factor, but it seems that in the end a reassessment of what an escalation in US-China trade tensions could mean to the Union and in particular to the export led German economy became the overwhelming force. The Euro now trades at 1.1226, pretty much at the same level where it was at Sydney’s closing time yesterday.

Gains in other traditional safe haven currencies, namely JPY (0.59%) and CHF (0.52%) have proven to be more resilient. USD/JPY now trades at ¥109.31and from a technical perspective it has a lot of free room to make its way towards the ¥108 area.

Meanwhile, AUD has yet again reflected its risk sensitive attributes leading the decline within G10 (-0.81%) and now trading at 0.6944 (overnight low of 0.6941). US-China trade tensions has seen an acceleration in USD/CNY and USD/CNH recent rise. USD/CNH now trades at 6.9112 ( CNY at 6.8774) and early in May the pair was trading around at 6.74. The market now looks to be contemplating whether or not Chinese officials will look to “weaponise “ the CNY and allow it to trade above the 7 mark. Allowing some CNY depreciation would help mitigate the impact from US tariffs, but such a move does not come from free, as CNY deprecation runs the risk of triggering capital outflows and instability in China’s domestic financial markets. So in addition to the uncertainty of a potential global growth slowdown from trade tensions, the risk of instability in China’s currency and financial markets is an additional concern for EM currencies and for the AUD, given the latters preeminent EM/China proxy status within G10 currencies. Thus the AUD looks vulnerable to further declines and ahead of the Asia open today, we also have the NAB Survey to look out for. The RBA has acknowledged the importance of the survey as a tool that could help resolve understand the current tension between weak growth and a strong labour market. So in addition to the headline numbers, details in the report are going to be important, particularly those related to the labour market.

The NZD has fared slightly better, and is 0.4% lower on the day to 0.6568. The risk of an escalation in the US-China trade conflict is also a major downside risk to the NZD. The next key support is the October 2018 low of 0.6425.

Bond yields have fallen, unsurprisingly, amidst a broad-based flight to quality. The 10 year Treasury yield opened 4bps lower in Asian trading yesterday and it has continued to slide since, falling 6bps to 2.4%. The 2 year Treasury yield has fallen slightly more, by 7bps to 2.19%, as the market has increased expectations of the Fed cutting rates. The market now prices a 50% chance of a rate cut in September and a total of 30bps by the end of the year. The Fed’s central scenario is to keep rates on hold this year, but were financial conditions to tighten significantly in the event of an all-out trade war, the market will look for a policy response from the Fed. Dallas Fed President Kaplan noted that higher tariffs would “have some chilling effect on business” although the impact on the economy would depend on how long the uncertainty persisted. Meanwhile, the closely watched 3m10y Treasury curve, which is one curve segment that has historically been a leading indicator of US recession, is again flirting with inversion.

Last but not least, the escalation in US-China trade tensions has not been a good night for most commodities. Gold is up around 1%, but copper and metals are down between 1.5% and 2%. Oil prices are about 1% lower and news from the Middle East are somewhat unsettling. Saudi Arabia said that oil tankers were the targets of sabotage on Sunday adding to regional tensions as the US increases pressure on Iran.US Secretary of State Mike Pompeo made an unexpected visit to Brussels, crashing a European foreign ministers meeting to push for a united transatlantic front against Iran.

In March Business Conditions printed at +7 and Confidence fell to a 5 year low of zero. On many occasions the RBA has emphasised the role of the NAB survey in understanding the current tension between weak growth and a strong labour market. Thus we believe the Bank and the market will be closely watching the details in the Survey’s April edition

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.