Online retail sales growth slowed in May following a fairly strong April

Insight

Markets have dipped sharply on the back of rising COVID cases.

https://soundcloud.com/user-291029717/markets-hit-by-the-delta-blues?in=user-291029717/sets/the-morning-call

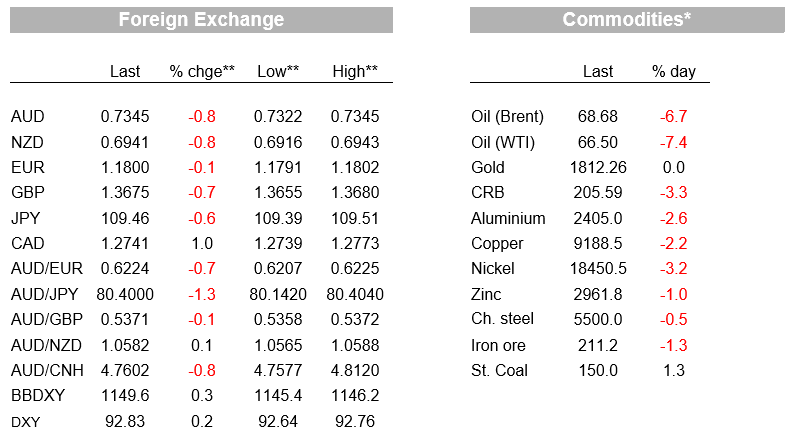

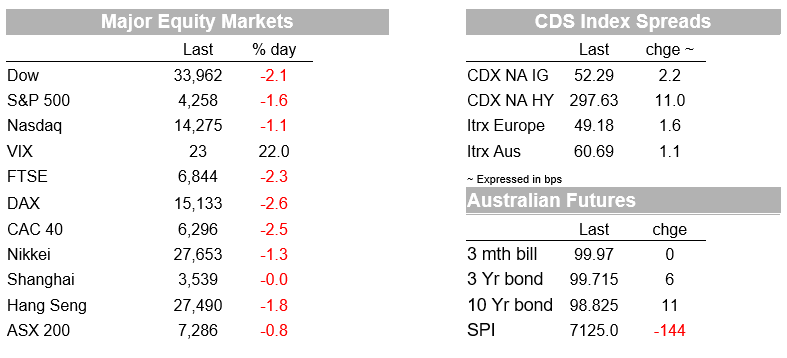

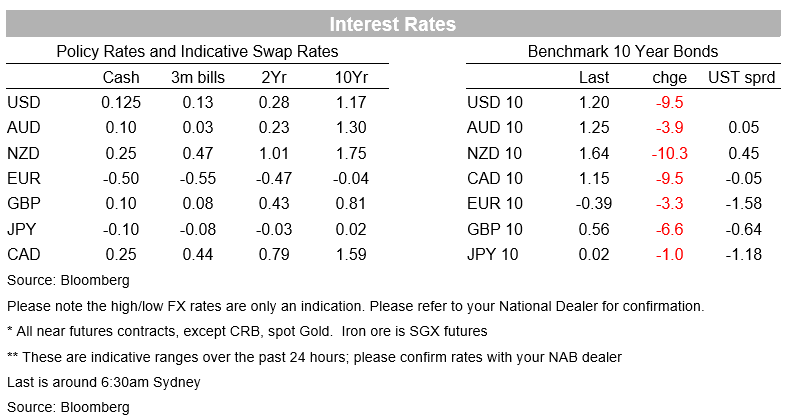

Virus concerns rattle markets in what was supposed to be ‘Freedom Day’ in the UK where most virus restrictions have now been repealed. It is also ironic that on ‘Freedom Day’ the UK PM finds himself in self‑isolation and the US CDC is warning against travel to the UK. It is worth noting virus concerns around the delta variant have been growing over the past few weeks as evidenced in bonds and FX, and today it has been reflected in global equities with the S&P500 -1.6% and the EuroStoxx600 -2.3%. Also contributing at the margin has been some concerns around the narrowing of the recent equity rally and the US and its allies publicly calling out China on state-sponsored hacking. Bonds have rallied sharply in this environment with the US 10yr yield -9.5 bps to 1.20% (low 1.1723%) and the German 10yr -3.3bps to -0.39%. It is unclear how positioning and the US and European summer holiday season is exacerbating price action. FX has seen classic risk-off moves with USD/Yen -0.6% and commodity currencies such as the AUD (-0.8%) and NZD (-0.8%) falling sharply to at or close to year-to-date lows.

As for virus concerns, there has been a global surge in the delta variant with emerging markets in particularly vulnerable. What is likely concerning markets now is that there is also a surge in infections occurring in developed markets with high levels of vaccination, underscoring that fully vaccinated people while being protected from severe cases and hospitalisation, can still transmit the virus. That suggests virus restrictions may need to be in place for longer (or even re-introduced) until vaccination rates lift further and full vaccination is available to everyone who wants it. The good remains that vaccines work. The data from the UK shows two doses of Astra Zeneca is 93% effective against hospitalisation, but only 60% effective against infection. The same is for the Pfizer/BioNTech which is 96% effective against hospitalisation, but again could offer less protection against infection. The findings are also supported by recent hospital admissions in the US with the WSJ noting that AdventHealth, which manages 41 hospitals across seven largely Midwestern and Southern states, said about 97% of roughly 12,700 Covid-19 patients treated this year were unvaccinated or partially vaccinated (see WSJ for details).

Adding to the risk-off tone overnight, during the morning session of European trading, the US government made the first public calling out of Chinese state-sponsored hacking, – stating that China’s Ministry of State Security employed criminal contract hackers “to conduct unsanctioned cyber operations globally, including for their own personal profit. ”. The UK, EU, Canada, Australia, NZ, Japan and NATO also added the support. While no sanctions against China have been announced, it also suggests tensions between China and the West are unlikely to abate, which also mean Australia-China tensions are unlikely to ease. NZ, which has so far pivoted between China and the US appears to be drawing closer to the US and Australia, which may have implications for the NZ-China relationship. Such questioning is a likely factor for why the AUD is being seen less as a China proxy by some analysts and has been cited as one reason why the AUD has been trading below where short-run models of the currency would suggest.

FX markets have seen safe-havens lift with Yen and CHF rallying. USD/YEN is down -0.6% to 109.60, and USD/CHF is 0.1%. The USD itself well supported (BBDXY +0.3%) and even EUR is showing some safe-haven characteristics, barely falling at -0.1% to 1.18, which has moderated the rise in the USD indexes. GBP has underperformed, -0.7% to 1.3675, with any positive vibe from “Freedom Day” steam-rolled by the surge in COVID19 cases and threat of a return to restrictions. It is also ironic that on Freedom Day the UK PM is in self-isolation and the US CDC has warned against travel to the UK because of the surge in the delta variant.

Commodity currencies which are also global growth proxies have fallen sharply. The AUD is down -0.8% and traded to a fresh year-to-date low of 0.7322 and is currently trading at 0.7345. Reflective of the risk-off tone the traditional risk-off FX play of AUD/JPY is down a sharp 1.3% to 80.40. The NZD has also seen similar moves to the Aussie, down -0.8% to 0.6941, after reaching a low of 0.6916, just below last-week’s year-to-date low. USD/CAD was hit even harder +1.0% to 1.2741. Also likely adding to the moves in commodity currencies was the sharp fall in the oil price with Brent down -6.7% to $68.68 on a combination of the OPEC+ deal gradually increasing supply and worries over growth given the delta surge in emerging markets, particularly in Asia. Other commodities also saw sharp declines with copper -2.2% and nickel -3.2%.

Economic news has been muted, but one interesting headline was the NBER declaring the US pandemic-driven recession as being officially over, with the recession only judged to have lasted for two months through March-April 2020. That would make it the shortest recession on record, which followed the longest expansion on record of 128 months or since June 2009 (see NBER Business Cycle Announcement for details). Should the US succumb to recession again, the NBER states it would be dated as a separate recession. Given the very short nature of the recession, it is no surprise why there is such a heated debate about the appropriateness of policy.

Finally, in Australia two press articles suggest the RBA is trying to send smoke signals about how it may react should the Sydney and Victorian lockdowns continue into August. The AFR’s Kehoe notes in RBA to rethink QE taper on delta lockdown that a virtual meeting was held on Monday between PM Morrison, Treasurer Frydenberg, RBA Governor Lowe and Deputy Governor Debelle. The article is well-sourced and suggests if the Reserve Bank of Australia knew two weeks ago the COVID-19 delta variant would force more than 11 million people in Sydney and Melbourne into hard lockdowns, it would not have announced plans to reduce the size of its QE program.

The RBA has two weeks until the August meeting to decide what it will do. No doubt the RBA will weigh up the potential for any permanent damage to the economy. NAB’s view is that the lesson from prior lockdowns is that activity bounces back and that we are unlikely to see an prolonged period of elevated unemployment as was the fear when QE was first unveiled back in November 2020. Since then the unemployment rate has swiftly fallen to a decade low of 4.9%. Similar sentiments were reported by The Australian’s James Glynn in RBA likely to bench QE taper.

Relatedly the same question is being asked about the RBNZ and prior expectations of a rate hike as soon as August. My BNZ colleagues note while this is possible, virus concerns could easily blow over in a month or two while NZ inflation will still be heading higher and the economy will still be over-heated.

A quiet day for data with only the RBA Minutes. Offshore it is also very quiet with no top-tier data scheduled: Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.