Total spending grew 0.9% in June.

The markets anticipate the next development in the US-China trade talks.

https://soundcloud.com/user-291029717/markets-ignore-impeachment-they-want-the-trade-war-resolved?in=user-291029717/sets/the-morning-call

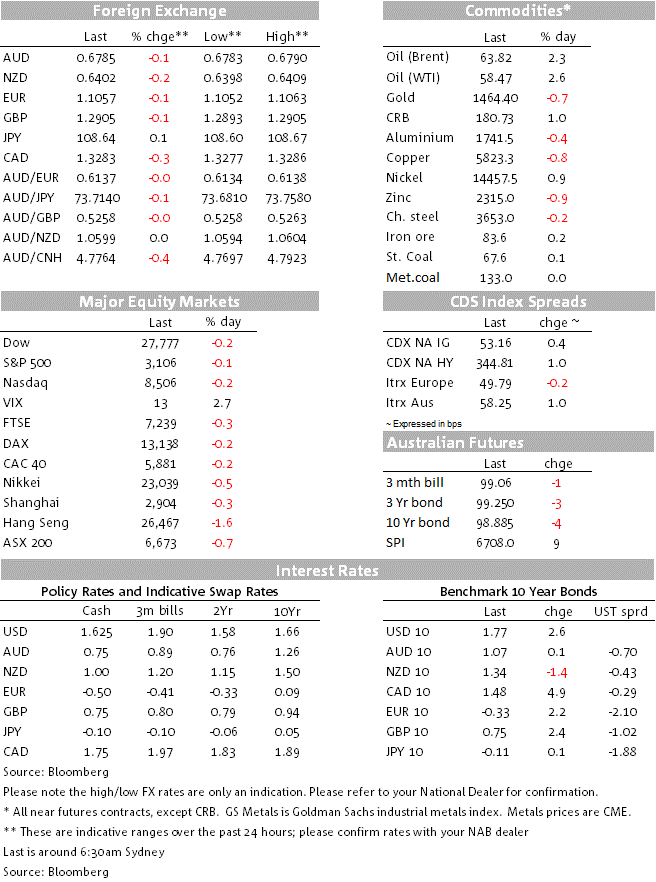

It was a quiet night overnight with limited market moves. Trade headlines again dominated, but on net the “glass-half-full” interpretation of a possible partial US-China trade deal continues with China inviting US negotiators to Beijing – inspiration for today’s title “Call Me Maybe”. FX was little moved outside of CAD with the USD (DXY) up 0.1% to 97.99, while US 10yr yields rose 2.7bps to 1.77%. Equities were also little moved with the S&P500 -0.1% to 3,106. Oil though rallied sharply with WTI +2.7% to 58.53.

A series of headlines overnight gave a degree of optimism that a partial agreement entailing a truce is still likely despite the HK Bill being seen as barrier to a more comprehensive trade deal. China’s Vice-Premier He said he was “cautiously optimistic” about reaching a phase one deal, while also outlining some domestic reforms which some interpreted as addressing some US concerns – though your scribe is more sceptical. The WSJ also reported that VP He had invited US negotiators for face-to-face talks in Beijing. The article also noted that Chinese officials hope the in-person negotiations can take place before next Thursday’s Thanksgiving holiday in the US, though US officials have not committed to a date (see WSJ for details).

China was said to be “watching Donald Trump’s response”, though it seems the signing of the bill is inevitable with the editor of the Global Times (seen to be close to Beijing) noting “US lawmakers have gone blind all together. Present Trump needs to sign the bill using braille”. Instead and as the SCMP writes, the bill probably prevents a more comprehensive deal, but a tentative truce is likely to hold and that is widely expected that the US will – if not remove – at least postpone the imposition of further tariffs that are scheduled to take effect on December 15 (see SCMP for details).

Data was sparse, though on a softer side in underlying terms. The Philly Fed Manufacturing Index rose to 10.4 from 5.6 (6.0 expected), though the details of the survey were weaker than the headline question with New Orders, Shipments and Employment all falling. Reweighting the Philly Fed according to the ISM weightings has the Philly Fed falling to a nine-month low. Jobless Claims also showed a soft edge coming in at 227k against 218k expected. Over the past couple of weeks claims have trended higher, but it is too early to assess what is driving the small uptick.

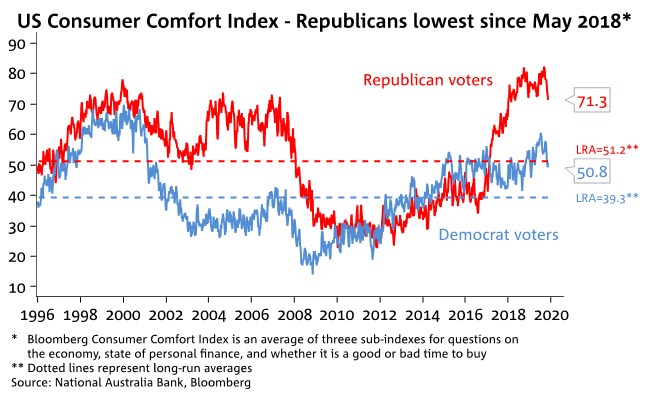

The Bloomberg Consumer Comfort Index showed consumer sentiment amongst Republican voters had fallen to its lowest level since May 2018 (see chart below). It is one tentative sign that some voters are feeling some headwinds, though as the chart below also shows confidence amongst Republican voters are still well above their long-run average level.

USD/CAD was the biggest G10 mover, -0.3% to 1.3281 with Governor Poloz pushing back on notions that the BoC had an imminent easing bias which had built earlier in the week. Governor Poloz stated: “we think we got monetary conditions about right given the situation” and that “we notice that the Fed has cut rates three times, now they are down to where we are….So the two economies are faring pretty similarly at this stage”. In other central bank news, the Fed’s Mester (non-voter, hawkish) reiterated the Fed is in a good spot.

The USD (DXY) rose +0.1% to 97.99 with correspondingly small declines in EUR (-0.1% to 1.1060), GBP (-0.1% to 1.2905), while USD/JPY rose +0.1% to 108.65.

There was little reaction to a late headline of the US Administration weighing a new trade investigation to justify tariffs on the EU as reported by Politico – a decision was expected to be made by Nov. 14 on whether to take action against imports of automobiles and auto parts from the EU with the passing of the deadline raising questions on whether he can continue to use s232 of the Trade Expansion Act to take further tariff action (see Politico for details).

The AUD was also little moved, down -0.1% to 0.6787 – though there was some intra-day movement alongside differing trade headlines with a high of 0.6814.

It’s PMI day with PMIs due from a number of countries including importantly from Germany – expectations are for bounce following improved investor confidence in the ZEW survey recently. Otherwise it is a fairly quiet day both domestically and internationally with only a speech by the ECB’s Lagarde of any interest.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.