Online retail sales growth slowed in May following a fairly strong April

Insight

Markets are in free fall as containment measures impact heavily on business.

https://soundcloud.com/user-291029717/markets-in-turmoil-as-virus-spreads-and-governments-fail-to-respond?in=user-291029717/sets/the-morning-call

Ha ha ha, Pump it,Ha ha ha, And pump it,

(louder),Pump it (louder), Pump it (louder),Pump it (louder) – Black eyed Peas

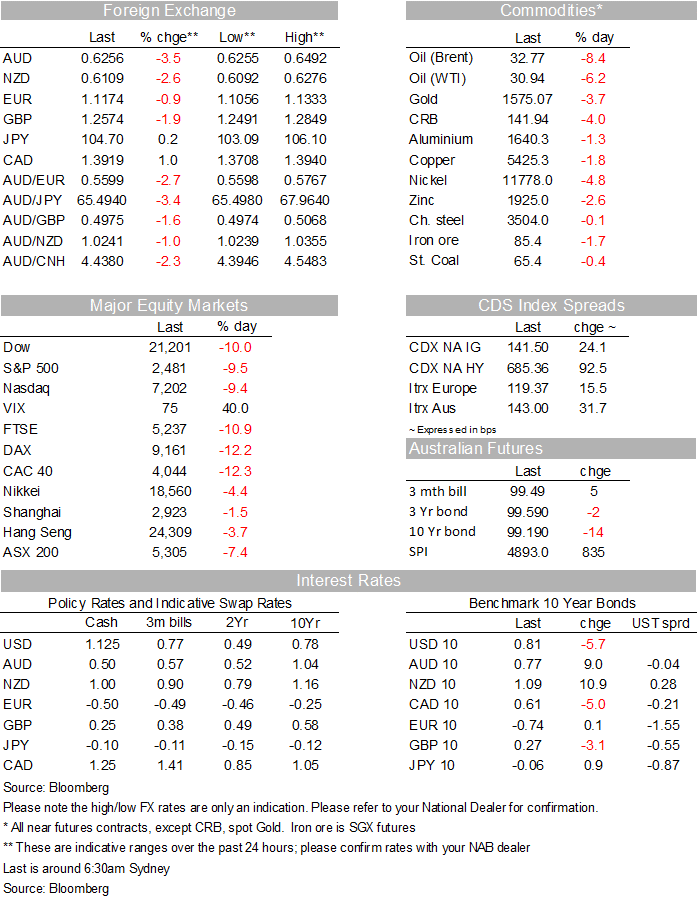

The turmoil in markets has moved up another notch over the past 24 hours with President Trump’s European travel ban and underwhelming stimulatory measures adding more fuel to the fire of uncertainty, instead of providing a dose of reassurance. Then overnight, the ECB did little to help the cause, effectively throwing the towel, keeping rates unchanged while increasing QE and lending options. Rout in equity markets extended into the NY session forcing the Fed to step in, announcing new repo facilities while also extending its Treasury purchasing programme to the whole term structure. QE 4 has arrived but it has done little to calm markets. Exit from risk assets has seen an increase for USD, we have seen wild moves in currencies with the AUD and NZD falling below 0.63 and 0.61 respectively, only to recover a little bit over the past couple of hours.

President Trump’s announcement during our APAC session yesterday did not have the intended consequences. Instead of providing a reassuring strategy in the face of a growing COVID-19 crisis, the President decision to suspend all travel from Europe (excluding the UK) to the US for the next 30 days (later revealed as meaning non-resident US folk) alongside underwhelming policy measures such as economic relief for workers and small businesses, spooked markets. Meanwhile hopes for a meaningful bipartisan policy response needed to prop up the economy remain deem amid ongoing squabbling in Congress.

The ECB rather than the FED was the one expected to provide a circuit breaker to the current market turmoil, especially with equity markets taking a battering from the open following President Trump travel ban announcement. But there was no shock and awe from the ECB. Instead the ECB held rates steady at -0.5%, prised open the Asset Purchase Plan with an additional EUR120bn of bond buying for the remainder of 2020 and focus its strategy on a new round of targeted loans to SMEs and the likes to keep the credit flowing. It lowered bank capital ratios, which will also help free up money to lend.

So a lot of cheap money has been thrown into the EU market, but the perennial problem in Europe is that there is no willing borrowers. Not surprisingly, ECB President Lagarde urged governments to form ”an ambitious and coordinated fiscal policy response” to match the ECB’s new injection of liquidity. That has been the right policy prescription for years and hasn’t happened so far, so the market rightly took the pessimistic view that nothing much will change. Bloomberg reports that German Chancellor Merkel’s government is prepared to abandon its long-standing balanced budget policy given the “exceptional circumstances” under the constitutional debt brake that allows for additional borrowing, although no official announcement has been made.

New containment measures to slow the spread of COVID-19 have increases the prospect of a severe global economic growth downturn. Over the past 24 hours we have had news of Italy’s government ordering almost every shop to close (the exceptions being pharmacies and grocery stores), India suspending most visas, Ireland closing schools and the cancellation of NBA games until further notice. Not long ago France announced plans to closes schools and universities from Monday, limiting public transport to a minimum with the elderly advised to stay at home.

The underwhelming ECB response and drastic COVID-19 measures, triggered a widening in Italian’s BTPS with the 10 year gapping up from 1.21% to 1.89% – a rise of 68bps before closing at 1.755%. The Euro continued its uprise almost touching 1.15 before heading lower as ECB Lagarde started her press conference. Then the extension of equity losses triggered a huge demand for USD with investors seeking the safety of cash in an environment where equities, credit and core global bonds were sold.

The Fed did not hesitate to act announcing an increase in size and term of its repo operations while also expanding its $60bn Treasury Bill programme to all Treasuries “match the maturity composition of Treasury securities outstanding”. So the Fed not QE programme has now officially morphed into QE 4. The aggressive move from the Fed makes it very clear that the Bank will not allowed USD liquidity to dry up. In terms of the details, the NY Fed will offer $500bn in a three-month repo today, with a further $500bn three-month and a $500bn one-month repo tomorrow. These will continue each week, in addition to the $175bn daily and $45bn two-week repos twice per week. Officially the Fed statement does not expand on the commitment to purchase Treasuries beyond April, but now that the QE box has been open again, it’s hard to believe the Fed will look to end the programme in a months’ time. We think an all-out policy accommodation is here to stay for a few months at least.

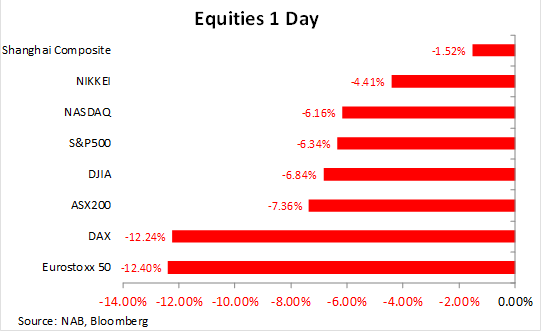

Main European equity indices closed the day with many recording record daily declines. The IBEX 35 ended -14%, the CAC 40 was -12.28% and the DAX closed at -12.24%. As I type US equity indices are down between 9% to 10%, the Fed announcement proved to be only a momentarily relief with equities reversing about half of their losses on the Fed news, from ~-8 to ~-4%), before resuming their decline.

Strong demand for USDs has been an overwhelming force with JPY losing its preeminent safe haven status, at least for the day anyway. USD/JPY got down to 103.09 soon after Trump’s address, and gained to as much as 106 overnight, the pair now trades at 1.475. EUR and GBP have also traded wide ranges in the order of 3-4 big figures, and both succumbing to USD strength.

The AUD traded to intraday low of 0.6266, it recovered a bit of ground after the Fed, but now is heading south again and currently trades at 0.6256. Similarly the NZD fell to a low 0.6095 and now trades at 0.6133.The Australian government’s fiscal easing announced yesterday (worth a temporary 0.9% of GDP) was a welcome development, but largely ignored by the market.

We are certainly in the midst of a severe global downturn and more drastic policy action from both central banks and governments should be expected (as I type the bank of Canada has announced an expansion to its repo operations). As my BNZ colleague Jason Wong noted in his daily, these volatile times are not likely to go away in a hurry. Thus risk and growth sensitive currencies such as the AUD and NZD have room to trade lower and for the AUD a move sub 60c can no longer be ruled out.

Equity rout accelerates

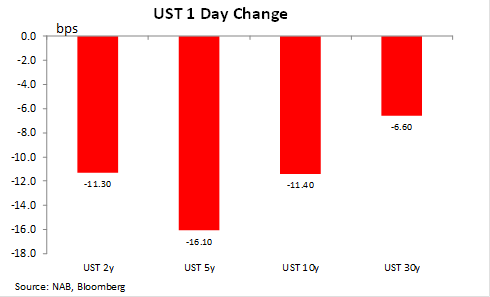

UST yields declines led by the 5y part of the curve

New Zealand gets its February Manufacturing PMI and the US releases the US. of Mich. Consumer Sentiment survey for March.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.