Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Markets are cautiously hoping the worst of the coronavirus is over.

https://soundcloud.com/user-291029717/markets-latch-on-to-falling-infection-rates?in=user-291029717/sets/the-morning-call

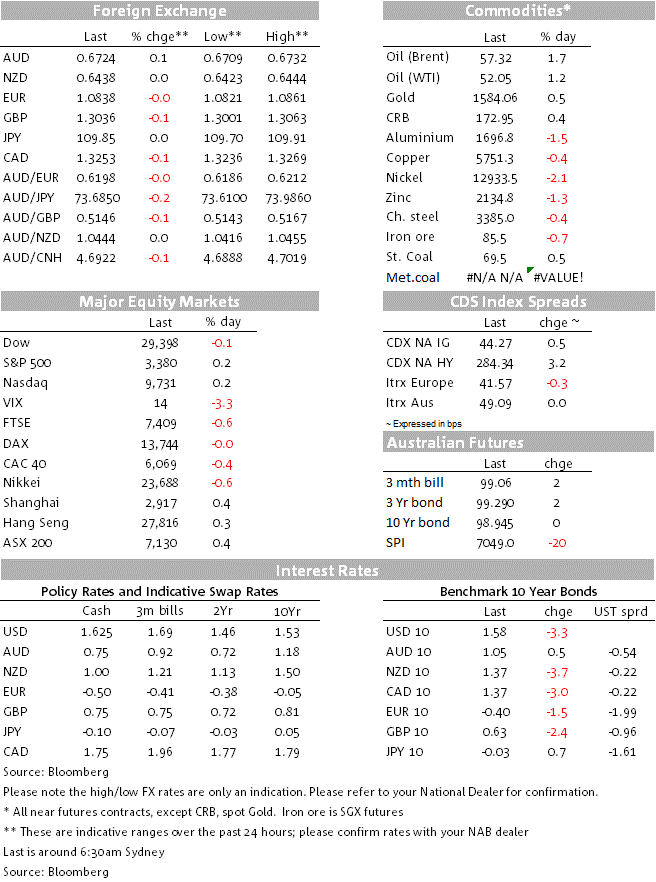

A couple of important economic statistics on both sides of the Atlantic came in weaker than expected on Friday – at zero – to largely cancel each other out from a markets perspective in what was a relatively quiet end to the week across currencies, bond and equities. The S&P500 nevertheless managed to scrape yet another record closing high at 3,379 (+0.2% on the day) in front of today’s US Presidents Day holiday when both stock and bond markets will be closed.

A drop in the number of new COVID-19 cases reported in China over the weekend – 2009 on Saturday against 2,600 on Friday – has seen the AUD open the week slightly firmer, 0.6724 versus Friday’s New York close of 0.6714. Announcements over the weekend from Beijing of tax cuts and reductions in government imposed charges on business, is also being greeted positively, while there is also an expectation of fresh monetary policy support this week with a possible reduction of 5bp when the monthly prime loan rate is set.

Germany’s Q4 GDP released on Friday printed at zero quarter-on-quarter against expectation of a 0.1% while the pan-Eurozone number was 0.1% as expected. Germany’s Q3 number was revised up to 0.2% from 0.1% (had it been revised down then given the -0.2% Q2 2019 print, Germany could have been classified as having falling into recession last year). On a work-day adjusted basis, Germany grew by just 0.4% in 2019, its weakest full calendar year growth rate since 2012.

The key US statistic was retail sales, where in headline and sales-ex-autos terms the rises of 0.3% were both as expected. What caught the market’s eye was the so called ‘control’ reading, which feeds into the consumption component of GDP and came in at 0.0% against the 0.3% consensus expectation. Here though, the story looks to have been weak clothing sales, which given the exceptionally mind US winter, is no real surprise.

It is hard not to conclude that the US consumer is in anything other than pretty rude health, buoyed by ongoing employment and stock market gains, in which respect Friday’s preliminary University of Michigan Consumer Sentiment Index of 100.9 up from 99.8 in December and 99.5 expected was the highest since March 2018 (before that you have to go back to 2000 to find a higher level). Also out Friday, US industrial production fell by 0.3% against -0.2% expected, with a bigger than expected drop in utility output (again warm weather related) largely responsible.

US bond markets continue to trade with a more cautious tone than equities, US 10-year Treasury yields down 3bps on Friday to 1.585% and 2s off 1.5bps to 1.43%. Bond yields were also lower in Europe, German bunds by 1.4bp to -0.404% and UK gilts giving back more than half of Thursday’s jump which had followed the hope of more fiscal stimulus as a result of the Chancellor (Finance Minister) being replaced, 10s -2.4bps to 0.624%.

Currency movements on Friday were minimal, in most cases by less than 0.1%. CAD (+0.11%) SEK (-0.5%) and CHF (-0.3%) were the only exceptions across G10 pairs. The DXY index added just 0.06%, but enough to deliver a new year-to-date high of 99.12, its highest since 8 October 2019.

It was a mixed day for commodities Friday, oil and precious metals (bar platinum) higher but base metals and iron ore futures all lower.

Thursday’s Australian labour market data are the key economic statistic this week (with the Wage Price Index for Q4 on Wednesday, seen +0.5% by NAB and the market consensus). RBA Governor Lowe has made clear that the trend in unemployment will determine if the RBA eases again, and will need to be rising for them to do so (last week he professed not to be obsessive about achieving the inflation target). NAB and the market consensus is for a return to a 5.2% rate after the unexpected fall to 5.1% in December. RBA Minutes are due Tuesday.

Internationally, COVID-19 development will again dominate (and where whether or not Australia lifts the travel ban on Chinese residents entering Australia on Feb 22, as currently scheduled, will be of note). Data and events wise, China is expected to announce further monetary policy easing on Thursday via a 5bp cut to the Prime Rate. ‘Flash’ February PMI data for the Eurozone and elsewhere (UK and US) are on Friday and which presumably will capture at least a little of the early impacts of the viral epidemic.

Today the NZ Performance of Services PMI is at 8:30 AEDT and Japan has Q4 GDP at 10:50 AEDT, expected to show a 1% fall on the quarter, in large part reflecting the hit from the October 1 rise in the consumption tax but weaker than expected rebound in activity in November and December, so an underlying slowing in activity.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.