NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

US equities finished last week on new highs on the hope the phase one trade deal between the US and China is close.

https://soundcloud.com/user-291029717/markets-living-on-high-apple-pie-in-the-sky-hopes?in=user-291029717/sets/the-morning-call

Woah, we’re half way there,Woah, livin’ on a prayer

Take my hand, we’ll make it I swear – Bon Jovi

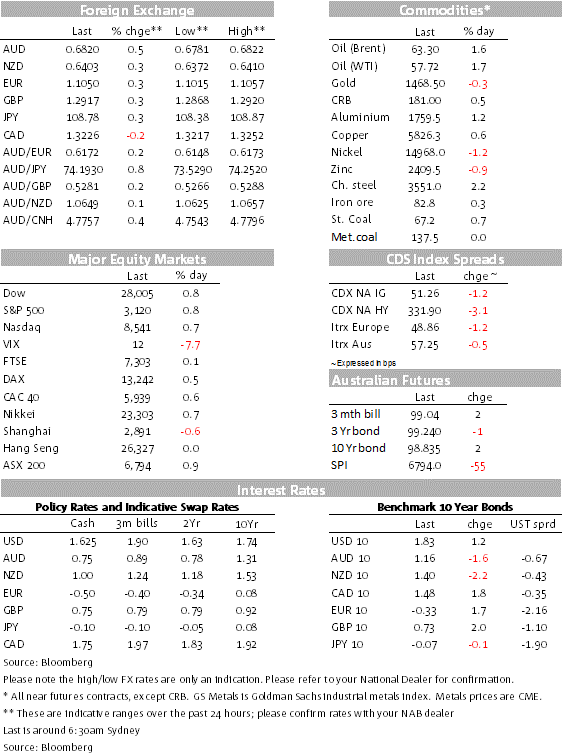

The hot and cold vibes from US-China trade tensions remains the dominant theme in markets with underwhelming US data releases on Friday only playing a secondary role. White House Advisor Kudlow’s comments early our Friday suggesting the US and China were close to finalising the first phase of a trade deal, eventually carried the day with Global equities ex China closing the week on a positive note. Despite soft US data releases, UST yields still managed to close higher while the USD was broadly softer with commodity linked currencies the main beneficiaries. The AUD climbed back above 68c, but it still ended as the G10 underperformer on the week while NZD was the top performer.

After some concerning reports on Thursday suggesting the US and China were struggling to complete a “phase one” deal to halt their trade war, early on Friday White House Advisor Kudlow said that the Phase-One trade deal was “coming down to the short strokes” and the “mood music is pretty good”. Later on US Commerce secretary Wilbur Ross said there would be a deal “in all likelihood” although he cautioned that “the devil is always in the details and we’re down to the last details now.” Supporting this narrative over the weekend, China’s Xinhua News Agency reported that Vice Premier Liu He had had a constructive phone discussion with his American counterparts Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer.

Global equity markets loved the positive trade vibes with major indices in Asia ex China, Europe and the US all recording decent gains on Friday. US equities led the charge within major equity markets with the S&P 500 and NASDAQ up between 0.7% – 0.8%, both indices also recorded fresh new highs in the process. Healthcare stocks (+2.2%) led gains on the S&P500 after the Trump administration released a plan to improve price transparency in the sector, with the market reaction suggesting that investors had feared worse. The VIX continues to hover near its lowest levels of the past year, at around 12, suggesting that the markets expect low volatility to persist (and showing few signs of concern that the trade talks might fall over again).

Soft US data releases only had temporary negative effect on US equities while US treasury yields still managed to close the day higher. Of note 10y UST yields rose 1.2bps to 1.83%, breaking the downtrend evident in the previous four days. Looking at the week, however, UST yields were lower along the curve with the decline led by the 30y bond, down 12bps to 2.305% while the 10y tenor was 11bps lower.

US retail sales rebounded in October (0.3% vs 0.2% exp.), after recording a negative print in September, however details of the report were not as encouraging. Net revisions were to the downside, the headline number was flattered by a 0.5% lift in Auto sales ( in contrast to the 3.4% drop in unit sales reported by automakers) while seven of 13 major categories posted declines. The control group increased by 0.3% as projected, but the data still show a decline in sales momentum, control-group sales have increased an annualized 4% over the latest three months compared with a 6.3% rate in the same period through September.

The USD was broadly weaker with JPY the only USD underperformer while commodity linked currencies were the G10 outperformers, reflecting the risk on backdrop evident in equity markets. USD indices were a touch softer on the week with the DXY index just managing to stay above the 98 mark while BBDXY closed at 1.202.18.

The AUD climbed back above the 68c mark ( +0.46%), but after its post labour market report decline on Thursday, the pair ended the week as the G10 underperformer ( down 0.67% on the week). IMM data release early our Saturday showed that speculator increased their AUD short positioning by 14k to -41k, ending a reversing trend that was in place since the start of October. Speculators also reduced their CAD longs by 12k, probably reacting to the more dovish tone by the BoC in the previous week. Against a softer USD backdrop, CAD was a tad higher on Friday and unchanged on the week.

A decent rebound in the NZ PMI and comments by RBNZ Governor Orr and Assistant Governor Hawkesby supported a modest rise in the NZD on Friday. The NZD was the top performing G10 currency last week, rising 1.2% against the USD, mainly reflecting the surprise on-hold decision at the November MPS. The NZD ended the week just above 0.64 against the USD while the AUD/NZD cross finished the week at 1.0643 .

The PBoC released its Q3 Monetary report with the Bank noting China’s economy faces greater difficulties as investment growth slows and industrial production remains sluggish. Relative to its August report, the PBoC noted an increase in economic challenges while also expressing renewed concern over higher inflation. In particular the Bank noted the increase in pork prices, remarking that the situation “must be drawn to attention and properly handled,” since it can affect people’s cost of living, adding that it expects inflation pressure to gradually decline in the second half of next year. The report concluded that Monetary policy will “properly handle the short-term pressure,” making sure not to offer excessive funding, while keeping an eye on the risk of expectations that (higher) inflation may spread.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.