On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

March data out of the US is bad and the share market has taken it badly.

https://soundcloud.com/user-291029717/markets-might-have-overaccentuated-the-positive?in=user-291029717/sets/the-morning-call

With my lightnin’ bolts a glowin’, I can see where I am goin’

With my lightnin’ bolts a glowin’ I can see where I am go-goin’

You better look down below – Arcade Fire

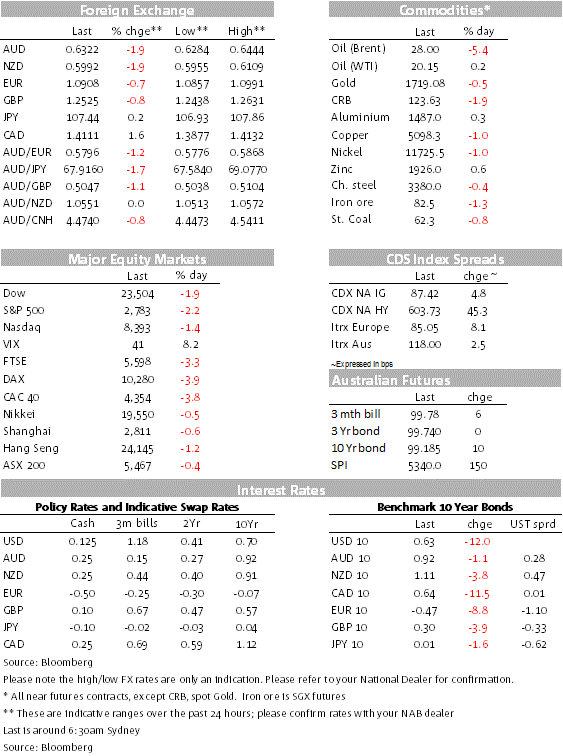

Well ahead of a tricky reporting season US equity markets looked always looked vulnerable following the huge gains recorded since the March 23 lows ( S&P 500 up ~30% since) and so overnight equity bulls got a wake-up call/ reality check following a batch of disappointing earnings results and dire US data releases. Declines in UST yields were led by the back end of the curve while the USD was stronger across the board with the AUD and NZD the big underperformers in G10.

Energy shares have led the decline in both Europe and the US following a collapse in oil prices (~6%) after the International Energy Agency (EIA) reported the biggest weekly increase in US crude inventories (19.25m barrel vs 12,024 exp.). The IEA also released a bleak demand outlook warning about the impact of Covid-19 quarantines on demand for the commodity, saying demand in April is down by 29 million barrels per day, swamping the impact of 9.7 million bpd of production cuts announced by the OPEC+ group last week. WTI traded to a new 18 year low of of $19.34, before recovering late in the session. Also late in the session, headlines hit the screen noting the US Energy department is considering a plan to pay US oil producers to leave crude in the ground. Bloomberg notes the unprecedented plan would require billions of dollars in appropriations from Congress.

Bank of America and Citigroup shares dropped after their earnings reports, even as they recorded strong trading profits, joining other banks in provisioning for big loan losses. A new accounting standard requires banks to set aside provisions earlier in a cycle. The S&P 500 financial sector closed 4.36% lower while in Europe the STX Europe 600 financial sector ended the day -5.07%.

The overnight batch of US economic data releases also painted a dire picture of a collapse in activity as a result of COVID-19 containment measures. The data releases revealed massive falls in US industrial and manufacturing production and retail sales, the numbers are for March and given containment measures were not fully implemented then, bigger falls are expected in April. Retail sales collapsed by a record 8.7% m/m in March, driven by autos, industrial production plunged 5.4% m/m in March and business survey indicators also showed record plunges, with the Empire State index (NY) down to minus 78 and the NAHB housing index dropping to 30. The only positive take-out was the control measure of retail sales that feeds into GDP increasing, as panic buying saw a 25% increase in food sales. The Fed’s Beige Book reported that “economic activity contracted sharply and abruptly across all regions”.

True to form the broad risk of mood has helped the USD performed across the board with JPY and CHF, the other to FX safe havens not far behind. The DXY index now trades at 99.56 (+0.56%), although midway through the overnight session the index almost touch 100. The Broader BBDXY is up 0.87% while the EMCI index is -1.09 ( EM FX).0.6319 and 0.5991

Unsurprisingly the risk sensitive AUD and NZD are at the bottom of the pile, down ~1.8% to 0.6319 and 0.5991 respectively. The AUD traded to an overnight low of 0.6284 while the NZD fell to 0.5955 before recovering somewhat later in the session. Our model for both antipodean currencies suggest recent gains and previous falls are largely explained by a decline and then improvement in risk sentiment. On a medium term basis we have a positive outlook for both currencies, but near term both currencies look vulnerable to a correction in equity markets following the impressive rebound since late March. The US reporting season is going to be an important test before we can confidently declare the current cycle lows for both the AUD and NZD are behind us.

CAD is not far behind in the big underperforming group, USDCAD +1.46% to 1.4080. The Bank of Canada left its policy rate at the historical low of 0.25% but expanded its plans to purchase investment grade bonds and provincial bonds, with the objective of bringing more order to financial markets. Governor Poloz’s comments on QE were interesting. He noted that it was pointless to implement large scale QE now to drive longer term interest rates lower – it is better left until during the recovery phase of the cycle. The economy is expected to be 15-30% smaller by the end of Q2 compared to the end of 2019.

The risk aversion emanating from equities has helped core bonds perform with UST yield declines led by the back end of the curve. Relative to yesterday’s levels this time, the 30y bond is down 13bps to 1.26% while the 10 note is -11.6bps to 0.6316%.German Bunds have led the decline in Europe with the 10y tenor down 10.7bps to -0.472%. Meanwhile EU peripheral have come under renewed pressure. 10y Italian BTPS jumped 10bps top 1.878% while Spanish Bonos climbed 2bps to 0.853%. The lack of a solid and united European fiscal plan clearly hurting EU peripheral bonds.

The COVID-19 headlines continue to paint a grim picture with global infections now climbing above the 2m mark while the death toll has risen to 133k. In New York Governor Cuomo ordered people to start wearing masks in public ( not sure where you can buy those) while encouragingly the EU commission has drawn a plan to for a partial lifting of restrictions but importantly the Commission also warned that some restriction will remain until a vaccine or cure is found. This is a similar message coming from Asian countries and Australia too. Meanwhile President Trump remains on a mission to reopen the US economy.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.