We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

For once US markets have been driven not by trade talks, but by hard numbers.

https://soundcloud.com/user-291029717/markets-positive-on-us-data?in=user-291029717/sets/the-morning-call

US equities, US bond yields and the US dollar are all modestly firmer overnight following a raft of US economic data showing the economy still rumbling along in generally okay shape amid still-benign inflation. GBP is the best performing G10 currency overnight, up in anticipation of a YouGov poll analysis due at 9:00 AEDT drawn from a 50,000 strong survey panel expected to predict an outright Conservative majority out of the December 12 General Election. There’s a smattering of AU and NZ data this morning; the US will be closed for Thanksgiving.

The US economic expansion may now be very long in the tooth, but concerns the US economy may be turning down, to the point where the Fed might have to resume policy easing next year, have been somewhat assuaged by the multitude of data releases in the last few hours. This has culminated in the just-released Fed Beige Book ahead of the December 10-11 FOMC meeting saying that most districts expanded modestly between October and mid-November, that manufacturing activity is some districts had picked up slightly since the prior survey – albeit most said it was flat – and that the vast majority of districts continued to note difficulty in hiring suitable workers. Wage pressures are intensifying for low-skilled positions, the Beige Book says.

Earlier in the night, one data point of particular interest was for weekly jobless claims. Following two consecutive weekly rises, and an uptick in the continuing claims series, there were fears that if this trend was repeated this week it would, based on past analysis, herald a weakening in the labour market and steepening in the US yield curve consisted with anticipation of a fresh central bank easing cycle. Not so, initial jobless claims fell back to 213k from 228k previously, bringing the 4-week average down slightly, while continuing claims dropped back by 57,000 to 1.64mn. So relief all round.

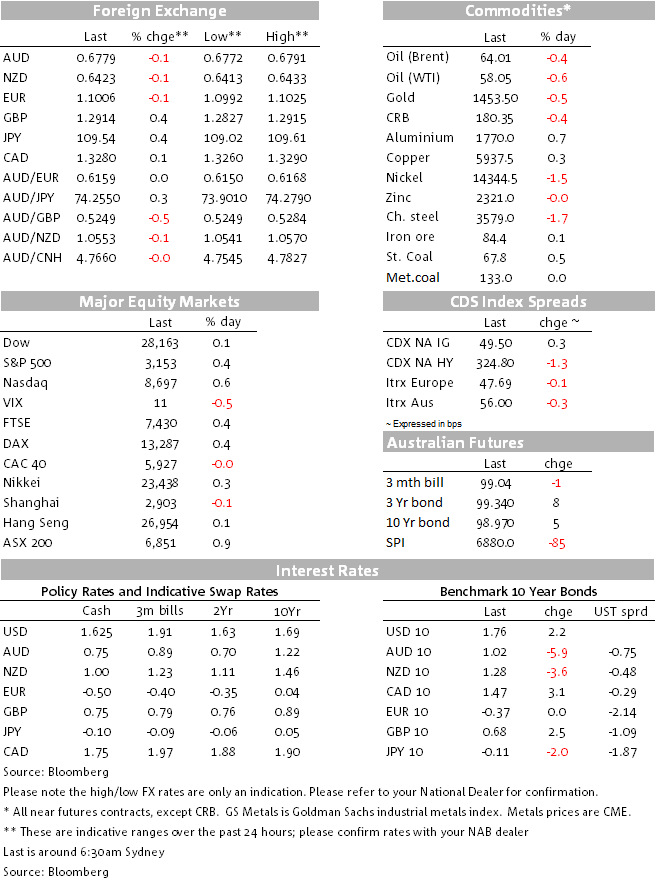

Other US data showed core durable goods orders unexpectedly recovering (+1.2% vs. -0.2% expected), suggesting that business investment might have risen after a bout of weakness. Q3 GDP was revised slightly higher to an annualised 2.1% (from 1.9%) albeit driven by inventories. On the less positive side, Personal Income was flat in October though may have been impacted by the GM strike, but spending was +0.1% against an expectation for unchanged. The core PCE Deflator – the Fed’s preferred measure of inflation – rose by 0.1% as expected, but it was a low 0.1% such that the annual rates fell back to 1.6% from 1.7% against the 1.7% consensus.

There have been no US-China trade developments overnight, not that bond and currency markets would have taken much notice had there been, unlike the US stock market which continues to grasp any excuse to justify still higher levels.

The net result of the data flow has been to see US stocks adding between 0.2% and 0.6% to Tuesday’s gains coming into the last hour of trading before Thursday’s Thanksgiving market closure (the stock market will also close early the day after – Black Friday). The S&P 500 is currently at a new record high, +0.4% 3153.

Bond market see 10 year Treasuries +2.4bps to 1.765% and 2s 4.2bp higher at 1.624%. So bear flattening as they say in the trade, the data flow diminishing any residual chance the Fed might cut rates again before Christmas.

In currencies, the AUD is still showing some of the effects of Westpac and at least one other bank shifting its RBA call yesterday to predict a low in the Cash Rates of 0.25% next year followed by QE. AUD weakness is not in isolation though, the EUR down by a similar amount, on USD strength not local Eurozone news, and with that the CHF. The JPY is the weakest currency, as it should be given that two if its key drivers, US bond yields and US equities, are both pointing up for USD/JPY.

At the other end, GBP is up a third of a percent. This is front of YouGov MRP poll to be carried by the Times and due to be announced at 09:00 AEDT. today. This poll utilises a so-called Multilevel Regression and Post-stratification technique (don’t ask) which allowed it to correctly predict in 2017 that Theresa May would lose her majority, while all other polls did not. Allegedly a US polling company called Langer Research has back-tested this methodology on the 2016 US presidential election and it correctly predicted that as well. The essential point is in the UK case it uses a much larger 50k sample size vs a typical 1-2k in most polls (which is why it isn’t conducted very often) and then this is blended with census data such as income distribution, age etc of voters in each constituency. The UK Guardian newspaper is saying it will show a significant Tory majority but that Labour’s fortunes have turned for the better and that if this were to continue, we could yet get a hung parliament.

US is closed for Thanksgiving

ANZ Nov Activity Outlook is at 11:00 AEDT (last at -3.5, Business Confidence last at -42.4). Also in NZ, this morning (08:45 AEDT) Statistics NZ will debut a new monthly employment indicators report comprising a monthly filled-jobs series and gross earnings, based on business tax data

Australia Q3 Capex is forecast by NAB to show a modest decline (0.5% q/q, mkt: 0.0%), alongside a 1% fall in equipment investment

The aforementioned YouGov poll and analysis is at 09:00 AEDT

German November CPI

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.