Online retail sales growth slowed in May following a fairly strong April

Insight

President Joe Biden and Treasury Secretary Yellen are about to give the details of their long-awaited infrastructure spending plan.

https://soundcloud.com/user-291029717/markets-rally-ahead-of-bidens-philly-talk

“You wanna know if I can dance; Yes sir, already told you in the first verse and in the chorus; But I will give you one more chance; Ooohh! Yes sir, I can boogie”, Baccara 1977

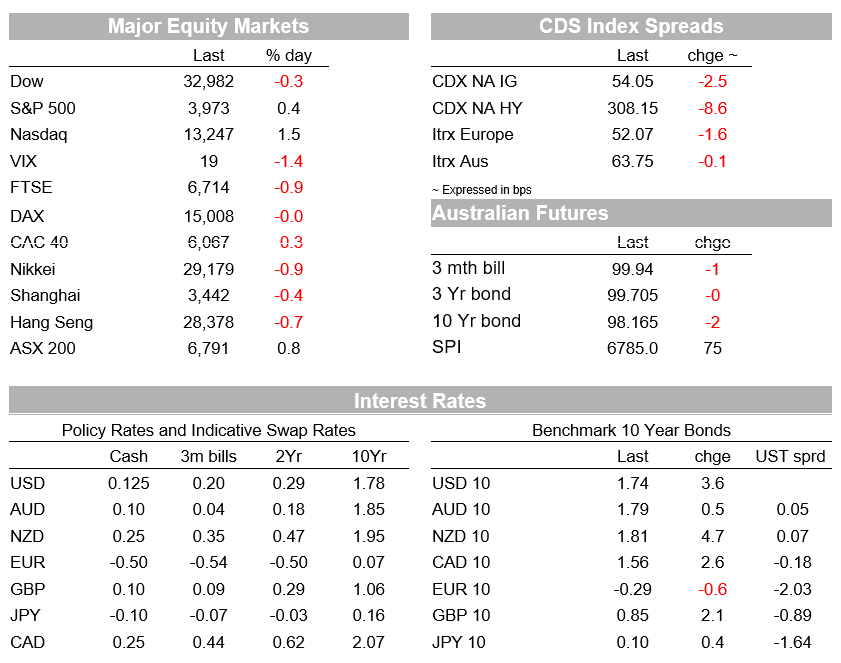

President Biden’s proposed infrastructure package was the main focus of the overnight session with Biden due to outline his infrastructure proposal in Pittsburgh later this morning. The Whitehouse has already briefed media on details, with headlines mostly as expected (an initial infrastructure package worth around $2.25 trillion, followed by another package worth more than $1 trillion to be announced in April). Equities rose to an intra-day record high with the S&P500 up 0.9% at one point, though have eased back a little to be up 0.4%.

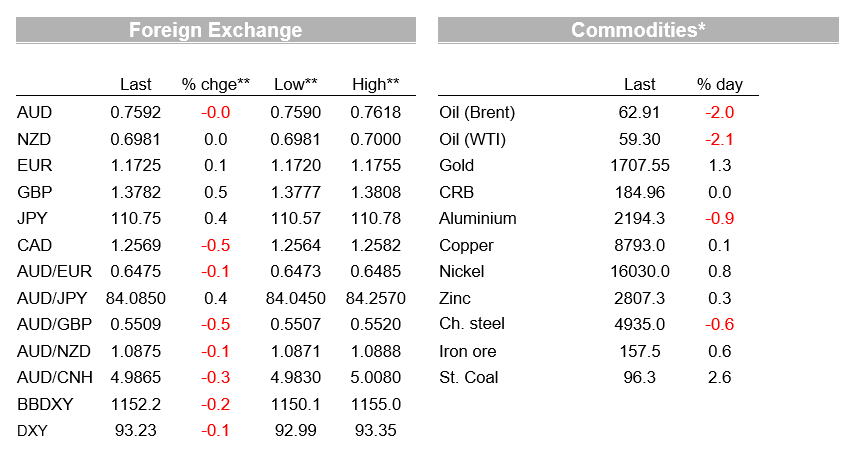

Interestingly industrials (-0.1%) and materials (-0.2%) have underperformed, suggesting a small ‘buy the rumour sell the fact’ dynamic at play. IT outperformed with the NASDAQ up 1.9%. Yields have largely consolidated with the US 10yr +2.5bps to 1.73%. Month-end/Quarter-end flows may be acting to restrain the move in yields given some notion balanced funds may need to re-balance to maintain asset allocation weights given the underperformance of bonds and outperformance of equities. The USD (DXY) is marginally softer, down -0.1% with the biggest moves in GBP (+0.5%) and USD/YEN (+0.4%). The AUD currently trades at 0.7598 with a lot of second-tier data on the radar.

As for Biden’s infrastructure package, the details reported by media is for a $2 trillion proposal over eight years and would be paid for over 15 years by raising the corporate tax rate to 28% from 21% and increasing taxes on companies’ foreign earnings to 21% from 10.5%. Importantly the tax increase proposal would still keep taxes lower than were they were prior to Trump when they were at 35% and could be seen as a carrot to try and gain Republican support for the package in the Senate. On the spending side, the proposal includes 621bn for transport infrastructure, 300bn for manufacturing, 213bn for affordable housing and $100bn to expand broadband access.

Politico reports that Democrats ultimately expect the infrastructural package to pass through budget reconciliation given a lack of Republican support, so the eventual passing of an infrastructure package may take time and the Whitehouse is advising by the Summer. As second package worth in excess of $1 trillion will be unveiled in April, which is said to focus on child care, healthcare and education. Higher individual taxes are likely to be part of that funding mix.

Bonds largely consolidated recent moves with the US 10yr up 2.5bps to 1.73%. A WSJ article noted the large bond moves on Tuesday likely came from Japanese investors locking in returns ahead of the end of their financial year. Notably the implied inflation breakeven continues to lift, up 2.7bps to 2.37% and around the highest level in almost eight years.

Data out overnight reinforced the inflation narrative with the Chicago PMI prices paid index increasing for the seventh straight month to its highest level since August 2019. The overall Chicago PMI also smashed expectations at 66.3 v. 61.0 expected and is at its highest level since July 2018. The regional manufacturing indexes for March suggest another strong ISM Manufacturing print today.

Other US data was more mixed. ADP Payrolls rose 517k, a bit below but close enough to the consensus at 550k. Pending home sales did fall sharply in February by 10.6% m/m and well below the -3.0% expected, but the severe winter storms were the likely factor there.

Elsewhere, Chinese PMI data was stronger than expected with the Manufacturing PMI at 51.9 v. 51.2 expected and the Non-manufacturing PMI at 56.3 v. 52.0 expected.

In FX, it was a tale of mild USD weakness with the DXY -0.1%. Month-end/Quarter-end flows may be a factor given rebalancing was expected to lead to some selling of the USD. Most FX pairs are little moved apart from GBP (+0.5%) and USD/Yen (0.4%). The AUD is little changed at +0.1% to 0.7598.

The European growth rebound is likely to continue to be delayed French President Macron announcing a four-week nationwide lockdown starting Saturday, which will include school closures and a ban on traveling between cities. Italy is expected to extend its current lockdown restrictions until the end of the month. The slow vaccine rollout is a factor. In contrast in the US, the CDC report that 73.5% of those aged 65 years have received one vaccine dose and 50.8% have received their full two doses. Accordingly it is likely the US will continue to ease restrictions, which should enable a strong rebound in activity.

Also in Europe, ECB President Lagarde pushed back on the recent moves in yields, stating that the market “can test us as much as they want.” ECB officials recently disclosed that the Eurosystem bought an average of €20 billion of debt a week over the past two weeks to keep financing conditions for governments, companies and households favourable. The coments had little impact on the EUR, which was up 0.1% overnight to 1.1727.

Finally in Australia, an MNI sources piece yesterday suggests the RBA could discuss whether to “effectively trim its guidance period for very low interest rates” as soon as the April meeting (presumably referring to the 3yr YCC and whether to extend the target to the November 2024 bond, or keep the target at the April 2024). However, a decision is unlikely to be made yet with “the central bank is still unconvinced unemployment can come down sufficiently to drive wages growth and inflation to the 2 to 3% target range under three years… ”. The sources piece echoes comments made by Deputy Governor Debelle in Senate Testimony where he said NAIRU is “pretty much certainly it’s a number lower than that [5%]; how much lower, we have an open mind on… But it would be great if that is a number in the low 4s or even in the high 3s as the governor said earlier.”

As for possible macro-prudential tightening, yesterday’s subdued investor housing credit will be a comfort to the RBA and APRA with strong investor activity previously flagged as having potential to amplify the housing cycle. APRA Chair Byres continues to push back on any near-term tightening, stating in a speech recently that “at an aggregate level, lending statistics do not show major signs of a return to higher risk lending” and in relation to the recent rise in house prices that “ we have no mandate to target the level of housing prices, or act to improve housing affordability. For us, housing prices are a risk factor, not a goal”. (see APRA Chair Wayne Byres – Speech to the 2021 AFR Banking Summit for details). Note today we get house price data for March with the AFR having been briefed that the five-capital city index is up some 2.8% m/m which annualises out to 33% y/y.

A big day for Australia ahead of the Easter long-weekend (note Friday and Monday are public holidays in Australia). On the calendar are Job Vacancies, House Prices, Housing Loan Approvals, Trade Balance and Retail Sales. Offshore the final versions of the Manufacturing PMIs are out along with the Caixin Manufacturing PMI. In the US the ISM Manufacturing and Jobless Claims will be of note. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.