Total spending grew 0.9% in June.

There’s a ‘risk on’ mood in the markets this morning after Friday’s u-turn by the US President over Mexican tariffs.

https://soundcloud.com/user-291029717/trump-ends-mexican-standoff-markets-react?in=user-291029717/sets/the-morning-call

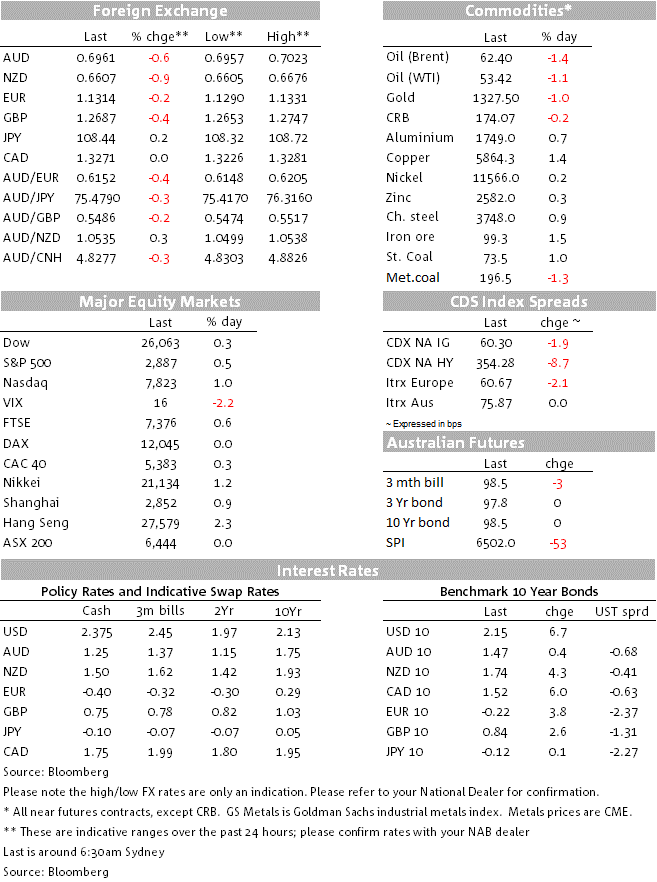

Anyone coming back into the office from a three day holiday weekend with the knowledge that Friday’s US payrolls report was all round soft, could be forgiven for expressing surprises to see US yields higher across the curve than where they were when Australia went home on Friday, and that the Aussie dollar is weaker not stronger. Less surprising perhaps to see that equities finished the week higher on heightened expectations the Fed will soon be cutting rates and has extended those gains overnight.

Higher yields and a stronger US dollar are largely the result of President Trump’s announcement after Friday’s New York market close that a deal had been reached on border control with Mexico such that he was not proceeding with the first phase of his threatened tariffs against all Mexican imports (the 5% rate was due to kick in on Monday). This news, and which also seems to have created a slither of optimism that having pulled back on this particular threat, Trump could agree not to forge ahead with lifting tariffs on the remaining $300bn of currently un-tariffed Chinese imports, has seen Treasury yields add back 5-6bps (so more than reversing Friday’s post-US payrolls slide) and pricing for Fed rate cut(s) this year pared back to around 60bp from nearer 75bps in the immediate aftermath of Friday’s non-farm payrolls release.

The latter, for the record, saw a 75k rise in payrolls last month (180k expected) with another 75k worth of downward revision to prior months. The unemployment rate was unchanged at 3.6% while average earnings rose by 0.2%, 1/10% less than expected and meaning that annual growth slipped back to 3.1% from 3.2% in April.

On US-China trade, President Trump has just said he thinks President Xi will be at G20 and that they are scheduled to talk. Earlier he told CNBC that if the meeting didn’t go ahead, he would look to increase tariffs on the remaining $300b of Chinese imports immediately. Meanwhile, the White House acting director of the Budget Office reportedly requested that the White House delay its recently announced restrictions on certain Chinese firms, including Huawei, by two years. The Budget Office said it would result in a “dramatic reduction” to the number of companies that are able to supply the US government.

On the latter, Treasury Secretary Mnuchin yesterday said that the Huawei is a national security not trade issue but couldn’t deny what his boss had earlier said, namely that a trade deal with China could include Huawei. All up, the end of month G20 meeting is gearing up to be another major ‘binary’ risk event that should keep markets very edgy in the coming days and weeks. It also complicates the FOMC meeting next week where the Fed has decide whether downside risks to US growth justify an immediate shift to a formal easing bias.

US equities pared some of the early day gain in the last hour of trade to leave the S&P up 0.5%, the Dow +0.3% and the NASDAQ +1.05%. The so-called ‘FAANG’ stocks evidently haven’t been hurt by the G20 Finance Ministers agreement that these global technology behemoths should be taxed in the jurisdictions where they generate their revenue (but so far this is just an ‘in principle’ agreement so could yet turn out to be a toothless tiger).

FX has seen the narrow DXY dollar index +0.26% but broader indices that includes Emerging Markets less strong (the BBDXY, which gives the Mexican Peso a near-10% weight, is little changed, thanks to a 2.1% rally in MXN.

AUD and NZD are down 0.6% and 0.8% versus Friday’s NY close, after AUD.USD had again clawed back onto a 0.70 handle in the wake of the US payrolls report. Higher US yields have usurped the risk-positive response to the Mexico deal news to see Aussie and Kiwi at the bottom of Monday’s G10 pack. Also weighing was yesterday’s China trade data, revealing a much larger than expected fall in imports (-8.5% y/y). This adds to pre-existing concerns that the Chinese domestic economy is slowing. Stronger Chinese export data (+1.1% y/y) was dismissed by the market as reflecting front-loading by exporters before higher US tariffs come into effect.

GBP fell 0.4% after much weaker than expected GDP and industrial production data (latter -2.7%, the weakest monthly reading in 17 years. Manufacturers had stock-piled ahead of the original March 29 Brexit leave date, but that has now seemingly gone into reverse given the Brexit extension to the end of October. The Conservative party leadership contest continues to rumble away in the background as well, with hard Brexiteer Boris Johnson still seen as a better than even chance of becoming the new Prime Minister by betting markets.

In commodities, base metals and iron ore are all stronger while oil is lower, WTI by 1% and Brent by 1.4%, to $53.42 and $62.39 respectively, so partly reversing last week’s Wed-Friday rally. Earlier Monday, Russian Finance Minister Anton Siluanov warned that oil could fall below $40 if OPEC+ countries don’t agree on an extension of production cuts (though there is little reason to think they won’).

Today’s NAB Business Survey will provide an important gauge of businesses’ post-election conditions. In addition to an update on overall conditions, the employment sub-index will be important to watch given it fell in April. These data will give a sense for whether labour market demand is likely to improve in the near- term – otherwise expectations for an August – or possibly July – follow up to last week’s 25bp Cash Rate reduction will harden.

Thursday’s May labour market report is of course equally important here, where NAB thinks election-related hiring might have sufficed to see a rise in employment (circa 40k) sufficient the unemployment rate tick down to 5.1% from 5.2%. If it doesn’t, then July will continue to be viewed as very much ‘live’ in terms of follow-up rates cut chances..

Internationally and on the week, China May activity readings promise to the highlight (Friday).The consensus is for retail sales growth to pick up to 8%, with growth steady for fixed assets and industrial production. Ongoing trade tensions are a major headwind to the outlook.

In the US following Friday’s payroll and as we head to the June 18/19 FOMC meeting, the main data are CPI on Wednesday, retail sales on Thursday and consumer confidence on Friday. Tonight’s NFIB survey will be of particular interest, since it will pick up any negative impact on small business sentiment following President Trump’s announcement on May 5th that he was increasing the tariff rate on $200bn worth of Chinse imports from 10% to 25%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.