Total spending grew 0.9% in June.

US equities have partially reversed their declines.

https://soundcloud.com/user-291029717/markets-resting-on-hope-of-a-tariff-delay?in=user-291029717/sets/the-morning-call

The market mood has stabilised overnight, despite confirmation that the administrative arrangements have been put in place to activate the increase in US tariffs from the end of this week. Presumably that’s on the basis that a deal is not struck and it’s back to square one with even higher tariffs risking further trade and economic dislocation. The talks are of course about to commence and the market will be watching developments closely.

Overnight, Reuters ran a piece exploring why trade talks had broken down over the past week between the US and China, sources stating China backtracked on a range of legal issues throughout the text of the proposed 150-page trade agreement, reversing the key points of agreement on US demands. Seen in this light, it is understandable why the US side has become very agitated.

Not only was the necessary paperwork done to ratchet up tariffs on $200bn of Chinese imports to 25% on Friday, Trump further taunted the Chinese with another tweet extolling the revenue benefits of higher tariffs:

Trump’s Press Secretary said that the White House has gotten an indication that China wants to make a deal, while China’s Commerce Ministry warned the government will “have to adopt necessary countermeasures” if tariffs are increase.

That uncertainty remains and it’s a long way from the expectation of recently as a week ago that the two sides had almost agreed on the document and this week more a formality rather than another meaty round of negotiations. It’s still not done and it could easily go pear-shaped again.

Stocks have been relatively steady overnight in both Europe and the US, European bond yields little changed, US Treasury yields one to three basis points higher along the curve, yields remaining lower for the week. An overnight $27bn auction of 10 year Treasuries did not go well, the bid cover ratio the lowest in a decade.

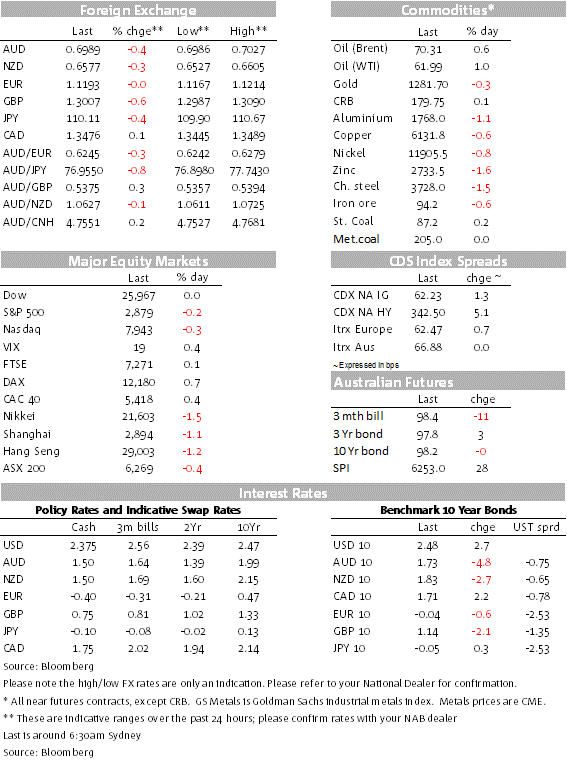

On the commodity front, oil prices have backed up somewhat, WTI us 0.94% to $61.99/bbl after the EIA reported a 4mb decline in inventories (against an expected rise) and with the Iran situation more tense.

Base metals were lower, the LMEX down 0.67% and copper by 0.56%. Bulk commodity prices remain relatively steady, iron ore in the low 90s and met coal futures at $205/t. Port Hedland iron ore shipments recovered in April after the Cyclone Veronica March disruptions. Gold is little changed, down 0.30% to $$1281.7/oz, $A1832.64.

Trump also upped the ante on Iran further, imposing sanctions on iron, steel, aluminium, and copper. He said “ Today’s actions targets Iran’s revenue from industrial metals – 10% of its export economy – and puts other nations on notice that allowing Iranian steel and other metals into your ports will no longer be tolerated.” Europe is urging Tehran to continue complying with the terms of the 2015 Accord.

Currency movements have been relatively contained, the DXY not making new moves either way, trading in the top segment of its range so far this week. That tinge of risk off has seen the AUD sit back at just below 0.70 this morning, down 0.44% from late APAC time yesterday, the NZD faring better, down 0.25%, AUD/NZD this morning at 1.063 pretty much where it was before the RBNZ cut yesterday. The NZ OIS market has shifted rate cut pricing for the cycle from 40 to 46 bps, a relatively modest move.

In that context, we note that Governor Orr has not sounded especially dovish about the outlook for the economy and rates, that the uncertainty factor is large, hinting of an insurance nature to the move. Another is partially priced in the months ahead in sympathy with the RBNZ rate track. The Bank indicated there is now “a more balanced outlook for interest rates”.

As for Brexit news, the UK Parliamentary 1922 Committee has met and determined not to change the leadership challenge rules so May lives on. The press is suggesting that the talks with the Labour Party are close to ending without a deal. PM May has told the head of the 1922 Committee Graham Brady that she is working toward getting a deal passed through Parliament before the European elections.

Of course, the press is full of the news of the new royal baby’s name, Archie Harrison Mountbatten-Windsor, and without a title.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.