Online retail sales growth slowed in May following a fairly strong April

Insight

US stocks have rebounded after a day when they were hit hard over concerns on the spread of the coronavirus.

https://soundcloud.com/user-291029717/markets-rethink-coronna-risk-aussie-cpi-today

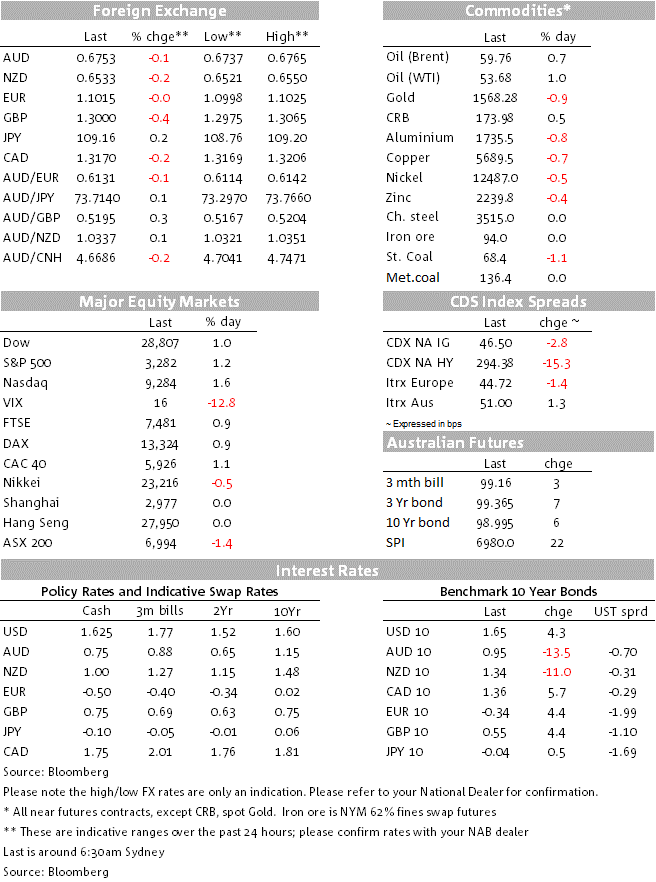

Since those APAC centres that were open yesterday went home, there has been news of more travel bans into and out of China (from the Hong Kong and UK governments to name two) but no new statistics on the official state of play with regards to coronavirus related fatalities and infection numbers. These stood at 107 deaths and around 4,500 confirmed cases. Unfortunately, the statistics are being reported as of the end of the prior day (i.e. the ones quoted here are from Monday). So we can expect updated numbers this morning and which run the risk of undoing some of the overnight moves, which include a decent bounce back in US equities, by 1.2% for the S&P 500 and 1.5% for the NASDAQ (the latter ahead of Apple’s results due straight after the 8:00 AEDT market close).

US Treasury yields are back higher (10s by 4bps to 1.65%) while in currencies the DXY dollar index is 0.1% higher but primarily because Sterling took a hit on news that the UK government is to permit Huawei into parts of the UK 5G network build out, news that is seen to complicate forthcoming negotiations vis-à-vis a US-UK post-Brexit Free Trade Agreement. Oil prices are a little firmer, which has helped NOK and CAD recoup a little of their recent loses, but gold and industrial metals are all down, which has kept the AUD on the back foot (down another 0.13% to 0.6752 and an o/n low of 0.6737). NZD is also lower and indeed underperforming AUD but for no obvious reason.

We’ve had some mixed US data overnight in the form of Durable Goods Orders, Consumer Confidence (Conference Board vintage) and The Richmond Fed Manufacturing Index. Durable goods orders was all over the place thanks to a jump in defence aircraft orders but predictable slump in Boeing orders (the former holding up the headline reading relative to expectations, so 2.4% against 0.3% consensus). The key core number is therefore orders excluding defence and aircraft, which fell by 0.1% against 0.3% expected and 0.1% previously. The trend here is mildly negative, but not worryingly so.

In contrast the US consumer still looks to be in rude health, Consumer Confidence up to 131.6 from 128.0. Still off its July 2019 local highs but a second successive monthly rise and in line with the recent improvement in the University of Michigan survey. A rampant US stock market (until the last week that is) and ongoing 100k+ monthly employment gains are more than enough to justify the recent strengthening in sentiment.

The Richmond Fed Manufacturing Index jumped to 20 in January from -5 in December and which together with other regional surveys released to date offers some hope for a recovery in the manufacturing ISM next week (after a fairly flat Markit reading last Friday)

Yesterday’s NAB Business Survey, which showed conditions down 1 point to 3 and confidence down 2 points to -2, related to December so will have not have picked up the full effect on business confidence and conditions from the bushfires that were at their most severe in early January. The January survey is in less than two weeks (Feb 11) so should be more revealing. The message from yesterday’s survey was that business activity stabilised in Q4 but at below average levels, with forward looking indicators (forward orders, capacity utilisation, capex) still weak.

Q4 CPI is due at 11:30 ET. NAB forecasts headline at 0.7% q/q, 1.8% y/y (consensus 0.6%/1.7%) and Trimmed Mean (core) at 0.4%, 1.6% y/y (in line with consensus). We revised up our forecast for headline CPI following a stronger than expected NZ CPI (0.5%) and where the tradeables component is correlated with the Australian CPI and which was a bit stronger than expected. This also suggests some upside risk to our Trimmed Mean inflation forecast. Any upward impact on headline inflation from food prices related to supply destruction and transport bottlenecks is more likely a Q1 2020 than Q4 2019 story.

The main event (at 6:00am Thursday ET) is the FOMC’s first interest rate decision of the year and subsequent press conference from Fed chair Powell. This looks like being one of the least market sensitive meeting outcomes of recent times, with no change in rates universally expected given the Fed’s likely assessment that has been no material change to their economic outlook – a stated precondition for changing rates – and no new economic forecast or ‘dot plot’.

Elsewhere we get Germany GfK consumer confidence, US Advance goods trade and Pending Home Sales

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.