Online retail sales growth slowed in May following a fairly strong April

Insight

The markets retreated from yesterday’s optimism.

https://soundcloud.com/user-291029717/markets-retreat-as-conte-goes-but-merkel-offers-an-olive-branch?in=user-291029717/sets/the-morning-call

The 66th Italian government since the end of the WWII has just collapsed, following what the BBC describes as a blistering attack by independent PM Giuseppe Conte on coalition partner Matteo Salvini, the deputy PM and leader of the far-right, anti-immigration League party currently riding high in the polls. Conte accuses Salvini of being ‘irresponsible’ in creating a new political crisis for Italy for ‘personal and party interests’. This after Salvini had tabled a no confidence motion against Conte and said he could no longer work with his coalition partners Five Star. Whether fresh elections are triggered or a new coalition government can be formed, remains to be seen.

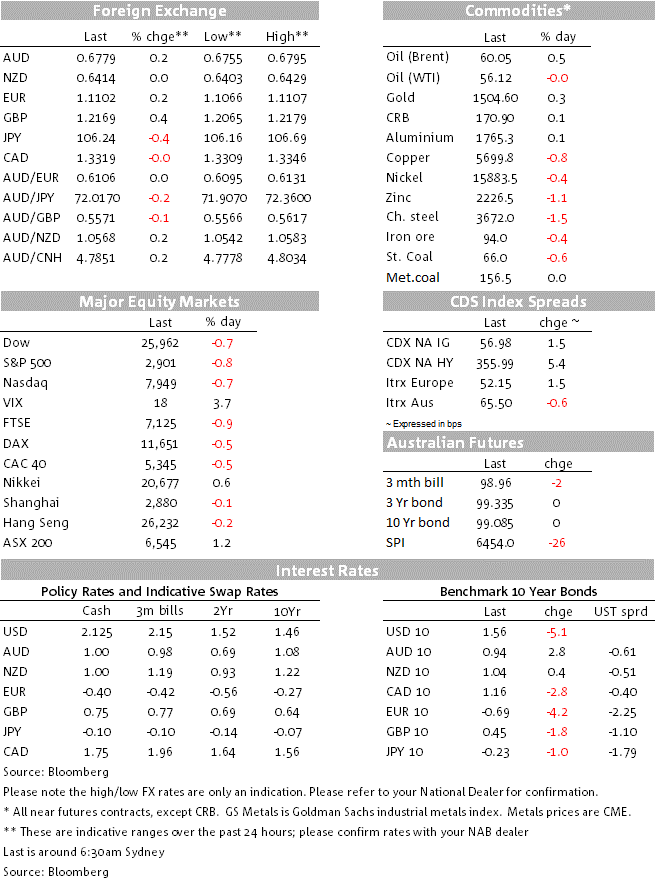

The reaction in European bond markets has been to see Italian government bond outperform all other Eurozone benchmarks, yields down 6-7bps across the Italian curve, Italy coming perilously close to re-joining the happy band of government issuers where investors pay for the privilege of lending them money. 2 year BTP are currently 1bp, down from 8bps this time yesterday. Go figure.

At least equity markets showed a modicum of concern, Italy’s FTSE MIB index down 1.1% and the second worse performing European index after Spain, in what has been a generally ‘risk-off’ night for stocks globally. US indices have finished 0.7-0.8% lower. Banks, consumer staples and materials are the worst performing sectors of the S&P, all more than 1% lower, financial presumably not liking the renewed US curve flattening – albeit not inversion – in the form of 10 year Treasuries down just over 5bps to 1.55% and 2s just under 4bps lower to 1.51%. Materials evidently haven’t liked the spectre of lower copper, aluminium and nickel prices, the base metals most synonymous with global growth sentiment. Iron ore futures on the Dalian exchange lost another 3.3% to now be 26% off their mid-July highs.

In currencies , USD/JPY is lower again, -0.4% to ¥106.23, in line with lower Treasury yields and weaker stocks. The best performing G10 currency has been GBP, +0.3% to $1.2167. The Euro is also firmer despite the Italian political news, +0.2% to 1.11. GBP was weaker earlier in the night on latest Brexit exchanges between UK PM Johnson and the EU, specifically the prompt rejection by EU President Donald Tusk to Monday’s letter from UK PM Boris Johnson demanding a renegotiation of the Irish Backstop in the Withdrawal Agreement. Tusk said that “The backstop is an insurance to avoid a hard border on the island of Ireland unless and until an alternative is found…those against the backstop and not proposing realistic alternatives in fact support re-establishing a border even if they do not admit it.” The recovery in GBP – and also the EUR – came after German Chancellor Angela Merkel adopted a more conciliatory tone, saying “we will think about practical Brexit solutions”. Johnson are Merkel are due to meet later today.

There have been no new developments on the discussion about Germany easing the fiscal purse strings to dig Germany out of a recessionary hole, though according to the Wall Street Journal US President Trump said the White House is examining proposals to bolster the economy, including various tax cuts, while maintaining that growth remains strong. Is this another ruse to pressure the Fed into more aggressive easing? In the meantime San Francisco Fed President Mary Daly has just been out saying her support for the Fed’s (July) rate cut did not reflect concern about an impending economic downturn, but merely aimed at extending the expansion, noting that the labour market remains at or near full employment.

AUD is virtually unchanged on where we left it yesterday evening at 0.6778 but this is 0.2% up on Monday’s New York close. AUD appeared to draw some support yesterday morning both from the RBA August meeting minutes, even though they contained little new relative to what Governor Lower had said before a parliamentary committee last Friday, and signs of a slight easing in Chinese monetary policy after the PBoC set its new one year Loan Prime Rate (LPR) at 4.25%, 10bps below the now-defunct 1-year loan rate. We also had source reports saying the government was considering relaxing limits on local government bond issuance aimed at financing more infrastructure spending.

A couple of snippets in the RBA Minutes that caught our (FX-trained) eyes were that, for one, the RBA said that the “recent depreciation of the Australian dollar was expected to support further growth in service and manufacturing exports” (they clearly don’t want it to go back up anytime soon). Second, was that they noted “market commentary that the US and Japanese authorities could intervene in an effort to lower the value of their currencies”. The latter of course could mean nothing, but interesting to see the RBA highlighting others talking about currency intervention and which was listed as one of the possible options for QE/unconventional monetary policy in their discussion on unconventional measures. We’d stress through that this is not a tool the RBA would be expected to adopt anytime soon. It might conceivably be forced to join an outright currency war, but it certainly is not going to start one.

The NZD is little changed on 24 hours ago. Last night’s Global Dairy Trade auction showed overall dairy prices were broadly stable (GDT Price Index down 0.2%), although with a lot of variation in the detail. Leading the positives was whole milk powder with prices perking up 2.1%, to an average price of $US3,100/T. This was better than expected and likely to bring some correction to futures pricing today against yesterday’s offer tone. On the negative side, there was weakness in fat prices with AMF falling 3.7% and butter down 3.4%.

The day ahead is a quiet one in terms of known data and events. Just Canada CPI and US Existing Home Sales tonight. FOMC meeting minutes are early tomorrow morning.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.