Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

There was no new vaccine news overnight and the markets seemed a little disappointed by that, with equities down and a move to government bonds.

https://soundcloud.com/user-291029717/markets-take-a-breather-but-standby-for-more-vaccine-news?in=user-291029717/sets/the-morning-call

“My mama said, you can’t hurry love; No, you’ll just have to wait; She said, love don’t come easy; But it’s a game of give and take; You can’t hurry love; No, you’ll just have to wait”, Phil Collins 1983

You can’t hurry love was a 1966 Motown classic by The Supremes (infamously covered by Phil Collins) and has some lessons for all of us as markets attempt to trade off a very positive medium-term outlook on well-founded vaccine hopes, against the current resurgence of the virus which is likely to slow growth in Q4 and perhaps Q1. While fiscal support will buttress household and business balance sheets in Europe, in the US there still appears to be little stimulus in sight given the partisan atmosphere in the lead up to the Georgia Senate run-offs on January 5 – important in deciding who has effective control of the Senate. It is becoming clearer that it will be up to the Fed to buttress the economy until the inauguration, though Powell overnight did not say anything new on the matter.

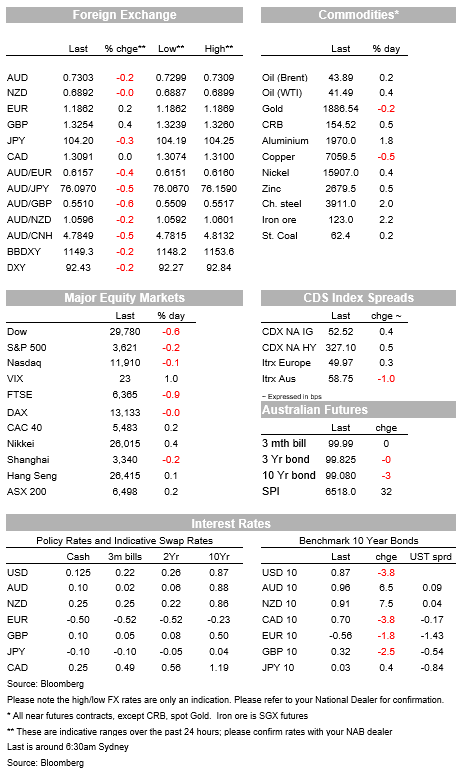

Equity markets in this atmosphere took a breather with the S&P500 -0.2% with most sectors lower. Yields fell with the US 10yr yields -3.8bps to 0.87%. Overall risk sentiment could yet be sustained with more vaccine headlines likely over coming days – Oxford/AstraZeneca results are said to be “imminent” and if similar to the efficacy seen in the other candidates will be important given the amount of shadow production and supply agreements undertaken by AstraZeneca. One stock also worth noting is Tesla which is set to enter the S&P500 on December 21 with Tesla stock surging 8.6% on the news.

FX moves were modest overall with the USD DXY down -0.2% to 92.43. GBP outperformed, up 0.5% and reaching a high of 1.3272 and now 1.3254. Yesterday media reported that a UK-EU trade agreement could occur as soon as next week with UK chief negotiator Frost telling PM Johnson to expect a deal “early next week”, reinforced overnight by Ireland’s PM who said he could see “landing zones” for the deal. We continue to remain optimistic that a deal can be inked at some point, that would push GBP higher – note GBP on a REER basis looks severely undervalued. EUR has also lifted in the wake of GBP, up 0.2% to 1.1862.

Consistent with the more cautious mood, global growth risk proxies underperformed with the AUD -0.2% to 0.7303 and NZD -0.0% to 0.6892. Yen rose with USD/Yen -0.3% to 104.20.

US data was mixed, though is consistent with the view of growth slowing in Q4, albeit with stark sectoral differences. US retail sales were softer than expected with Core Control at 0.1% m/m against 0.5% excepted. Revisions to prior months though did see the level of the retail numbers actually be 0.5% higher, even if headline growth disappointed, and it is worth noting the level of retail sales remains well above pre-pandemic levels. The below-consensus October numbers were accompanied by a +0.5% net revision to the headline, so the level of sales last month was higher than implied by the consensus. Homebuilder sentiment (NAHB) surged to a new record high of 90 in November with the housing market remaining an area of strength, as it is globally. Industrial Production also largely met expectations (1.1% m/m v. 1.0% expected), though manufacturing production remains 5% below pre-COVID levels.

Financial regulation looks like it may eased globally in an attempt to lift investment coming out of the pandemic. The BoE’s Bailey overnight said if the UK economy was going to recover successfully from the crisis, it would require business investment “on a much larger scale than we have seen in recent years”. “We live in a time where there appears to be no shortage of aggregate saving, but investment is weak ”. Bailey cited current limitations of pensions funds investing in illiquid long-term assets. Closer to home, the AFR also notes Australian Treasurer Frydenberg will tell regulators to ease up interpretation, stating overzealous intervention is hampering the recovery (see AFR for details).

The RBA Minutes yesterday shed little new light given recent speeches by Governor Lowe (note Dr Lowe is talking again today – see coming up for details). The Minutes conclude that “The Board is prepared to do more if necessary.” and the recent SoMP noted that this would likely entail more QE if necessary. Assistant Governor Chris Kent also spoke yesterday, noting the recent vaccine news improved risk sentiment in turn boosting the AUD – so once again the RBA rationalising the recent run-up in AUD.

Finally, Australian Payrolls yesterday suggest a sharp rebound in the Victorian labour market is underway following the easing of restrictions early in October. High-frequency mobility indicators suggest this should continue. Victorian payrolls rose 1.0% over the fortnight to 31 October, while payrolls also rose strongly across other states. While it is tempting to conclude that the tapering of government support such as JobKeeper has not had a continuing negative impact on the labour market, there appears to have been a significant impact for small business employment. Small business payrolls (<20 employees) fell sharply in the week to 31 October (-0.4%) and since late September are down 4.9%. In contrast, payrolls at larger firms (>200 employees) rose strongly in the week (+1.2%), more than offsetting the decline in small business payrolls. It is not clear what is driving the divergence between larger firms and smaller firms, though the divergence does align with the tapering of JobKeeper and appears to be broad-based amongst states.

Domestically we get the Wage Price Index and RBA Governor Lowe is talking on a panel. Neither should be particularly market moving given subdued wages growth is likely to remain a feature for as long as elevated labour market spare capacity remains, while Governor Lowe has given extensive remarks already this week. Offshore it is also relatively quiet with most focus remaining on the UK and whether a UK-EU trade deal is closer, while there is also more central bank speak from the BoE and Fed officials. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets.

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.