NAB pushes out first rate cuts to May 2025 as “lower for longer” strategy plays out

Insight

Last week was a choppy week as markets tried to balance out positive economic news against rising concerns about COVID-19 infections.

Divided states of America, Divided states of the world, If we don’t all stand together, we will fall – the Script

A positive APAC day for risk sentiment on Friday extended into the European day and start of the US session, where the S&P opened 1.3% higher. One helpful headline here was that ‘China planned to step up its purchases of US farm good after talks’ (in which respect reports over the weekend were that China committed to purchase some $38bn worth of agriculture, which represents its whole commitment for 2020 under the Phase 1 trade deal signed in January).

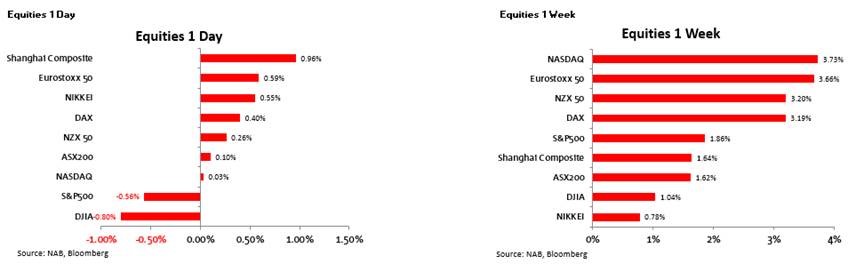

The S&P down as much as 1% in early NY afternoon trade and the NASDAQ -0.7% before the S&P recovered to finish down 0.56% and the NASDAQ about flat. Souring the mood – but seemingly helping the share prices of Amazon and Netflix and accounting for NASDAQ outperformance – was news of the high and rising infection rates in several US states and where the potential economic ramifications were brought home by Apple announcing the renewed closure of some of its stores in Arizona, Florida and the Carolinas. Saturday’s pan-USA numbers were the highest since June 8 with particularly alarming rates of increase noted in Florida, Texas and Arizona. In the last couple of hours, California has reported its highest daily infection rate to date. At his rally in Tulsa on Saturday night, President Trump told the crowd he had done a ‘phenomenal job’ with the pandemic and said he asked officials to conduct fewer coronavirus tests to keep case numbers down.

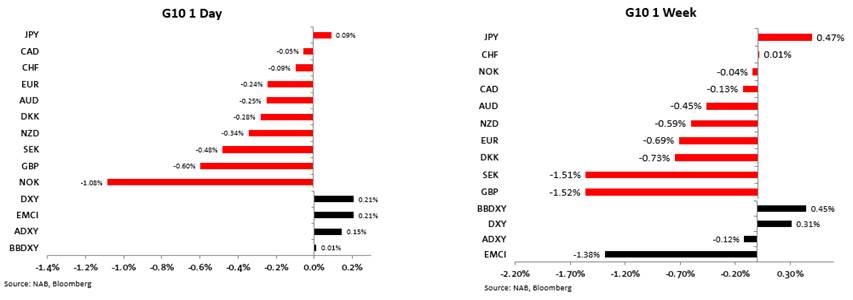

The USD also flipped between negative and positive in the NY afternoon, to end the day close to unchanged on the BBDXY index. On the week though, some note needs to be taken of the fact that it was an up week for stocks (S&P +1.9%) but also an up week for the USD (BBDXY +0.45%). This marks a break with recent tradition where the negative correlation between the S&P and USD had in the past 30 days been its strongest since 2016.

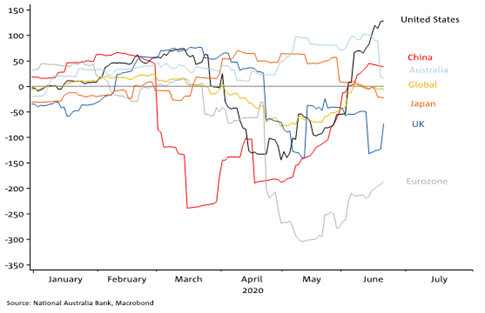

We don’t read too much into this, though do note that incoming US economic data has surprised more to the upside than any other big country of late (see Chart of The Day below). As we saw by way of negative GBP reaction to the underwhelming BoE policy actions last Thursday, FX markets currently seem to be rewarding upside economic surprises or policy actions that are seen to capable of improving economic outcomes. Let’s see then whether the weekend reports in the UK Times of plans to temporarily cut the VAT (GST) rate from 20%, broaden the scope of goods and services not subject to VAT and other measures aimed at reducing employment costs for firms, are greeted positively in the GBP FX market.

Earlier during our day, preliminary Australian retail sales rose by a hugely impressive 16.3% in May (no consensus but much stronger than the ~5% NAB had expected). Food retailing rose by 7.2% from already high levels, but unsurprisingly there were large rises for clothing and eating out as restrictions were lifted during May. Also, large rises in household goods retailing. This puts the level of total retail sales about 4% above the February level, prior to the panic buying that occurred in March and 6% lower in Q2 to date after a 3% rise in Q1.

UK retail sales on Friday also comfortably exceeded expectations rising by 10.1% (ex-auto fuel) against the 4.1% consensus, but unlike in Australian where sales were back above their February level, in the UK they are still some 13% below, doubtless reflecting the far more limited relaxation of social distancing restrictions last month. On this, July 4 is now being billed as ‘Independence day’ after media reports that this date will see the current 2-metre social distancing rule relaxed to 1-metre.

Canada’s retail sales – for April not May – fell by almost twice as much as expected, -22.0% (ex-autos) against the -12% consensus.

Central bank speak from various Fed official on Friday was consistent in stressing the likely slow pace to full economic recovery and the extreme uncertainty surrounding the outlook. By way of example, Minneapolis Federal Reserve Bank President Neel Kashkari warned on Friday that the economic recovery from the COVID-19 pandemic in America will likely take longer than many have predicted and that if a second wave of novel coronavirus cases does surge forth, it will likely push unemployment figures even higher than they’ve been thus far. He said he believes the true figure of unemployed Americans is actually larger than is being reported, estimating it to be at about 20%.

Fed Vice-Chair Rich Clarida telling Fox Business network “We’ve taken very aggressive, proactive action,” and that “There’s more that we can do and we will.” Asked if he saw unintended consequences or new bubbles stemming from the massive Federal Reserve policy response to the coronavirus pandemic, Clarida replied: “I certainly don’t.”

Nothing substantive came out of the EU virtual Summit on Friday called to discuss the European commission’s proposed EUR750bn Rescue and Recovery Fund. A deal was never expected on Friday, but leaders agreed to progress talks quickly, Council President Michel announcing an in-person summit in mid-July, saying “it is essential to take a decision as soon as possible.” Council President Von der Leyen said she hoped a deal could be secured before August, admitting differences remain on the size of the package, how the money will be distributed and the balance between grants and loans. German chancellor Merkel said all 27 member states had agreed to the German and French proposal for the EU to raise money on the financial markets (originally for EUR500bn, recall) and spend it across Europe, but stressed that the road ahead was tricky and that large compromises were needed.

Tuesday’s ‘flash’ Markit PMI data for the Eurozone in particular, promise to be among the week’s data highlights (also the German IFO survey on Wednesday).

Today, RBA Governor Phil Lowe speak on a panel titled ‘Global Economy and COVID-19’ starting at 9:00 AEST. Then at 11:30 we’ll get the monthly PBoC announcement on the 1 and 5 year Loan Prime Rates, which notwithstanding last week’s cut to the 14-day reverse repo rate are expected to be unchanged at 3.85% and 4.65% respectively.

We have Eurozone consumer confidence, seen improving to -15.0 from -18.8 in May, and US May Existing Home Sales, seen -5.6% after falling by 18.8% in April.

ECB Vice president Luis de Guindos and Chief Economist Philip Lane are both due to speak in the early hours of our Tuesday morning.

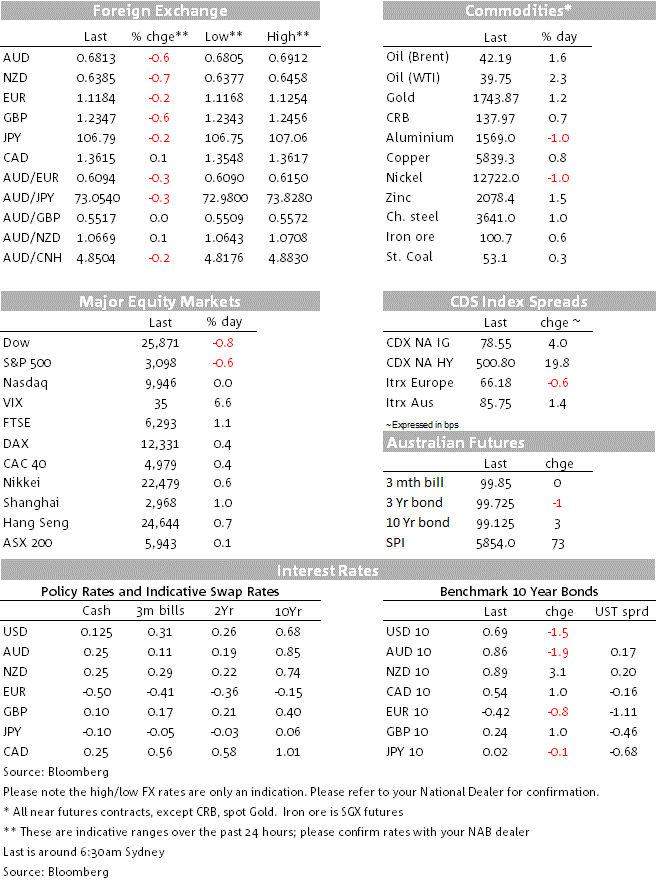

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB pushes out first rate cuts to May 2025 as “lower for longer” strategy plays out

Insight

The NAB Rural Commodities Index continued its upwards momentum and increased 1.4% month-on-month in May. The index is around levels seen in February 2023.

Report

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.