Online retail sales growth slowed in May following a fairly strong April

Insight

Markets flipped from Friday’s share and bond sell-off, with more optimism a day or two out from what is expected to be a Biden victory.

https://soundcloud.com/user-291029717/markets-turn-green-on-hope-of-a-blue-victory?in=user-291029717/sets/the-morning-call

Overview: Election time

“Alternative energy or oil in your SUV, Tell me what you’re looking for, we about to have a poll, Gun Control, Infrastructure, agriculture, manufacturer, Hip Hop Be My Culture, Tell me what you think about us Technology and foreign policy, I need the bailout money to stimulate the economy…” – Wyclef Jean

Prophetic lyrics from the Haitian rapper who was ruled ineligible to stand in Haiti’s 2010 presidential election, inspired he says by the ‘We don’t need no education’ mantra in Pink Floyd’s ‘Brick in the Wall’. So there

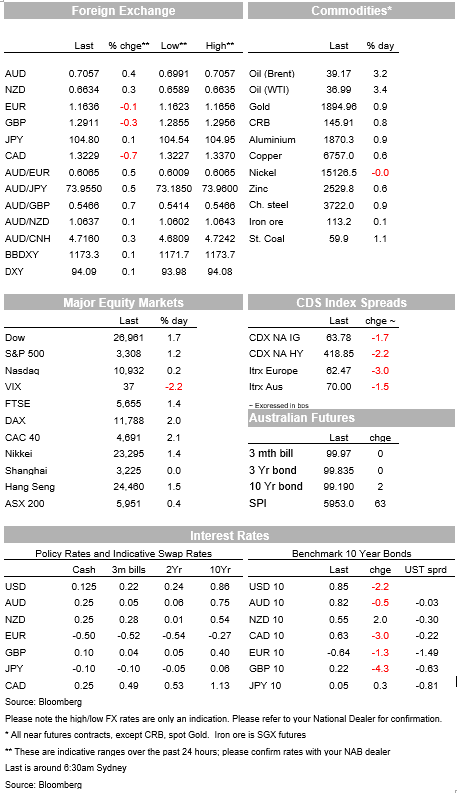

The sell-off in risk assets since the middle of last week, and (of late atypical) accompaniment by smartly higher US bond yields, has at least partially reversed overnight, stocks recovering somewhat and Treasury yields lower in front of the two-day Fed meeting starting tomorrow. Growth/cyclical currencies have done better in this environment, led by CAD on higher oil prices, with AUD pulling back up are a brief visit sub-0.70 yesterday.

Equities have closed with the S&P up 15%, the Dow 1.6%, while the NASDAQ has ended flat. Arguably these moves are consistent with increased confidence in a Joe Biden election victory this week (whether or not we know the results as early as tomorrow evening our time) with no significant narrowing his polling lead over President Trump since the end of last week, and what that potentially means for ‘Big Tech’ from a regulatory standpoint, following on from evident disappointment about sales guidance and demand from China in last week’s Q3 results from Apple as well as the social media giants.

A good start to the Wall Street day – following from earlier gains in futures markets during the APAC and Europe session – was given an added boost by the US manufacturing ISM index, comfortably exceeding expectations with a jump to 59.3 from 55.4, its highest since September 2018 and led by a surge in New Orders to 67.9 from 60.2. Why so strong? The most obvious reasons are that: 1) US ISM typically lags prior strength in China equivalents and strong credit growth (tick); 2) Household have remained cashed up from earlier Pandemic Unemployment Assistance and other handouts from the CARES Act (tick); and 3) Unable to spend as freely on various services, consumer have been loading up on good, such as cars (tick). On the latter point, Wednesday’s ISM services may well tell a different story from the manufacturing numbers.

Bond markets have shown something of a pull back (in yield terms) after the back up in 10-yar Treasuries from around 75bps to 88bps at the end of last week, down almost 3bps to 0.8470. Market will now be keen to hear the messaging out of this week’s FOMC meeting and whether Chair Powell inspire confidence that the Fed will not allow the recent run-up to gather undesired momentum that will then entail some risks to the economic recovery, on top of myriad other factors of course.

FX has seen the USD slightly firmer, notwithstanding it being a mostly positive night for risk, with the DXY and BBDXY indices both up about 0.1%. A slightly softer EUR and GBP are the culprits and where on the latter yesterday’s seemingly positive news (c/o Bloomberg) that compromises had been seen on the thorny (if largely symbolic) matter of fishing rights, the overnight news doesn’t look quite so encouraging (evidently still work to be done here). Commodity/growth sensitive currencies have fared best with CAD leading the way helped by a reversal of the weakness we saw in Asia yesterday (WTI and Brent currently both up by about $1.30). Here, reports that Russian oil companies were meeting with their oil minister to discuss delaying planned relaxation of production curbs until Q1 next year, appears to have been helpful.

Ahead of the RBA, AUD has lifted to back above 0.7050 after spending time briefly below 0.70 yesterday. The latter followed the risk-negative start to the APAC day, as well as more disconcerting news on China-Australia trade, with lobsters now subject to import restraint (China claiming on biosecurity grounds) and later in the day reports of bans on timber imports from Queensland and, overnight, suggestion that copper ore and concentrates and sugar could be next cabs off the ranks.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.