NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

There’s been a swift reversal in sentiment.

https://soundcloud.com/user-291029717/markets-worried-over-longer-lockdowns?in=user-291029717/sets/the-morning-call

Can you feel it coming in the air tonight, oh Lord, oh Lord- Phil Collins

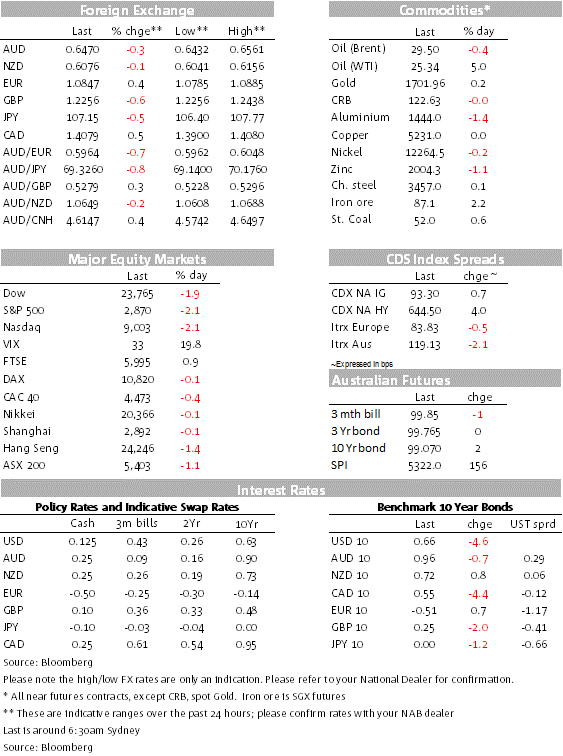

The cautious feeling in the air at the start of the week has moved up a notch in the overnight session with the tech-heavy NASDAQ index leading the decline in US equities. US Health official Facui warned of the risk of opening the economy too soon and Fed Quarles warned the central bank could curtail banks’ ability to pay dividends. UST yields lead the decline in core global bond yield with a solid 10y UST auction a supporting factor. AUD and NZD recover most of yesterday’s losses as the USD loses ground overnight and recovers later in the session.

We had a trifactor of sobering news that have played into a cautious vibe in markets. US top health official Fauci appeared before the Senate Health Committee and expressed concern about cities and states reopening without reaching “checkpoints” outlined by the administration. “I feel if that occurs, there is a real risk that you will trigger an outbreak that you might not be able to control,” Fauci said. “In fact, paradoxically it will set you back – not only leading to some suffering and death that could be avoided but it could even set you back on the road on trying to get economic recovery. That would turn the clock back rather than going forward.”

The mood was not helped either by news that Republican Senator Graham introduced a China sanctions bill that would authorise President Trump to impose sanctions on China if Beijing “fails to cooperate and provide a full accounting of the events leading up to the outbreak” of COVID19.

We also had a few Fed speakers pushing back at the notion of a negative Fed funds rate overnight (Bullard, Kashkari and Harker) although the comments had little impact on the market from pricing a negative funds rate from mid next year onwards. Fed’s vice chairman for supervision, also spoke and noted that Fed could curtail commercial banks’ ability to pay dividends by raising the amount of capital they need to maintain due to the coronavirus crisis. Fed Bullard also warned of the risk of possible depression if shutdowns are prolonged.

The news mentioned above played into the cautious tone evident in markets with tech shares joining the decline in the US. The NASDAQ and S&P 500 ended the day down just over 2% with IT, Financials, Real Estate and Energy sectors, all recording losses greater than 2%.

US Treasuries have led the decline in core global bond yields with a solid 10y UST Note auction helping UST’s performance. The US bond market is having no trouble absorbing the marked increase in supply this week, with strong demand for a record $32b of 10-year notes following on from yesterday’s strong 3-year auction, while the yield achieved was 1.2bps below market expectations. The UST curve bear flattened with the 30y Bond down 4.9bps to 1.369% compared to yesterday’s closing levels while the 10y note fell 4.7 to 0.664%.

The move lower in UST yields initially weighed on the USD, but later in the session as the move lower in US equities accelerated, the USD regained most of its early loses as risk aversion impregnated the air. The USD BBDXY index now trades at 1253.33 and the DXY index is at 100, both are little changed relative to this time yesterday’s levels

Yesterday during our APAC session the AUD came under pressure following news that that China had suspended meat imports from meat processing plants in Australia: Kilcoy plant, Beef City in Toowoomba, the Dinmore meatworks in Brisbane and the Northern Co-operative Meat Company at Casino in NSW. The meat bans come as China prepares to slap large tariffs on Australian barley as early as this Sunday. Recall last year that China reportedly had an unofficial go-slow on the unloading of Australian coal exports at Chinese ports after China was accused of hacking the Parliament House computer network.

The AUD traded down to a low of 0.6432. Initial USD weakness helped the AUD regained some ground overnight climbing to an overnight high of 0.6536, before heading down again as the USD benefited from a safety bid into the NY close. The AUD now trades at 0.6471. The NZD came under pressure yesterday morning, in sympathy with the AUD and overnight it has followed a similar path to the AUD, seeing some resistance just below 0.6125 and the pair now trades at 0.6077.

The NAB April Business survey was also release yesterday (Business conditions -34 from -22, confidence -46 from -65), but it didn’t elicit a reaction by markets.. Conditions weakened further in April and are now well below the levels seen in the GFC. Conditions fell across almost all non-mining industries, including a sharp fall in wholesale which saw a surprise increase last month. Overall conditions are now deeply negative in all industries outside of mining. Business confidence bounced in the month, but remains well below the trough of the 1990s recession after the large fall last month (indeed it’s now two times below the 1990s recession trough, rather than three times).

NOK is the G10 outperformer (+1.37%) over the past 24hr with the move up in oil prices a crucial factor. WTI oil climbed to its highest level since early April ($25.34, +4.97%) after the U.S. government lowered its output forecast for the year. The Energy Information Administration revised down its 2020 and 2021 crude output forecasts in its monthly Short-Term Energy Outlook. So although a huge over supply remains, the increase in global stockpiles is slowing.

GBP is the G10 underperformer (-0.64% 1.2256) with COVID-19 related news not helping the cause. Amid the prospect for an extended lockdown to fight the virus outbreak, UK Chancellor of the Exchequer Rishi Sunak said the government will help pay the wages of millions of workers for another four months in an effort to stop them losing their jobs amid the coronavirus lockdown. Meanwhile BoE Deputy Governor Broadbent reinforced economists’ expectations that the Bank could ramp up bond purchases as soon as next month. The central bank is keeping all its policy tools under review, including taking the benchmark rate below zero, although that risks doing more harm than good, he said in an interview with CNBC Tuesday.

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.