We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Month-end has seen a broad sell-off of the US dollar.

https://soundcloud.com/user-291029717/month-end-less-growth-fewer-jobs-more-loans?in=user-291029717/sets/the-morning-call

US stocks have just closed out April with small falls on the day but gains of 12.7% on the month for the S&P 500 – its best monthly showing since January 1987. The Dow is +11.1% and the NASDAQ an even more impressive 15.5%. Today’s title, from my musical heroine Patti Smith and featuring some exquisite guitar playing from the unique Tom Verlaine (he of Marquee Moon fame) is dedicated to those who chose to fight the Fed last month.

Amazon posting revenue of $75.4bn on the quarter and giving guidance of $75-81bn for Q2 versus the street consensus of $77.9bn. Its stock is nevertheless currently down about 4% after hours (profits dropped in the quarter) but having rallied hard into the close it is only back to where it was on Tuesday.

Apple has just reported revenue of $58.31bn, well above its $54.25bn estimate and EPS of $2.55 ($2.44 est.) and says it has seen a pick-up in sales activity in the latter part of April. Its stock did jump 2.5% straight after the results but the gains have seen been fully retraced.

Clothing retailer J Crew is reported to be set to file for bankruptcy.

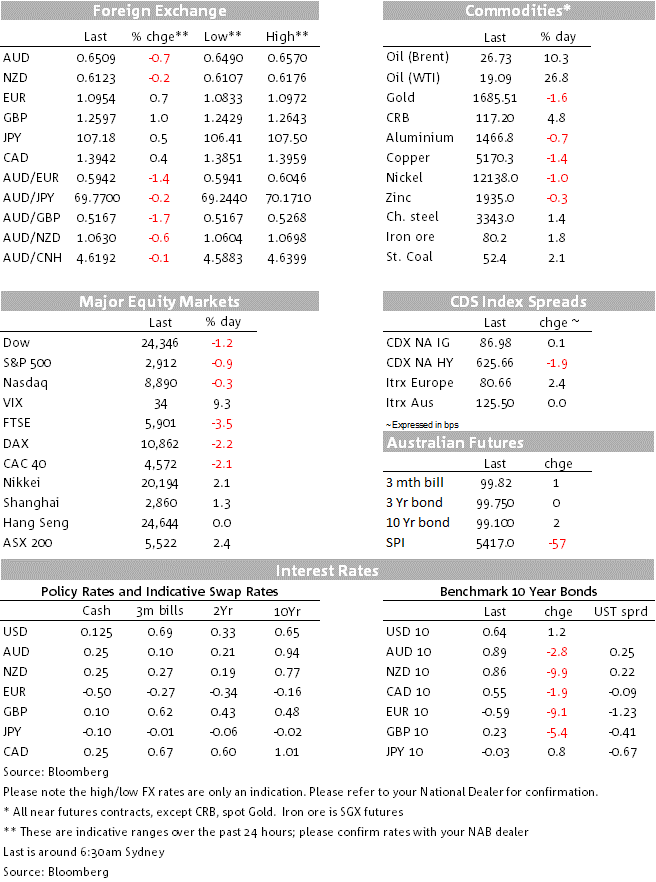

FX markets have, unsurprisingly given the April equity moves, seen some quite intense volatility around the 4pm London fix and which is most evident in GBP, AUD and NZD, all seeing excess demand and so spikes higher. Unlike GBP which held the fixing related gains to be the best performing G10 currency on the day (+1%) AUD is the worst performing (-0.7%) with some decent selling seen a few hours before the fix – and subsequently. The loss on the day can’t though obscure its outstanding performance on the month, +6.25% and leaving all other G10 pairs in their wake (next best performing has been the NZD, +3% and EUR the worse, down 0.7%). the USD is overall not much changed in April, the Bloomberg BBDXY index just -0.3%.

Yesterday we noted that May is traditionally a poor month and also that it falls more often than not the month after it post gains of 6% or more. Caveat emptor.

The ECB made no change to its bond buying programme (worth over €1000b through to the end of the year) but ECB President Lagarde said that the Bank was fully prepared to increase the size of the programme and to adjust its composition by as much as necessary and for as long as needed. The Bank cut the cost of funding for banks in the TLTRO – enabling them to borrow from the ECB at a rate as low as minus 1% for lending to businesses and households

The Eurozone economy contracted by 3.8% in the March quarter, activity already 3.3% down on year earlier levels. The contraction in Q1 is already larger than the worst quarter in the GFC and during the subsequent Euro debt crisis. It is the largest since Eurostat quarterly estimates started in 1995. Individual country estimates came from France (-5.8% QoQ) Spain (-5.2%) and Italy (-4.7%) and which highlight in particular the already well-known damage to particular sectors such as tourism but also business investment (e.g.-11.4% in France) . Even though this is the largest recorded quarterly contraction, there is much worse to come in Q2, where a 7.6% decline is the current consensus. Germany’s ‘flash’ Q1 GDP is not out until May 15 but presumably will not be down quite as much as France Italy and Spain if the Eurozone as a whole was ‘only’ down 3.8%.

The GDP data and ECB announcement helped support a rally in European bonds, seeing Germany’s 10-year rate down 9bps to minus 0.59%. EUR initially fell after the ECB was out of the way, but rallied hard into the London 4pm fix and has held up since, around 1.0950.

The Fed expanded the scope and eligibility for the Main Street Lending Programme, now including larger companies with up to 15,000 employees or up to $5b in revenue (more than 40% of the S&P500), while the minimum loan size was halved to $500k. The programme can support lending of up to $600b. Alongside European bonds, US Treasuries were well supported earlier in the session, seeing the 10-year rate fall back below 0.60% to a low of 0.58%, but it has since risen to 0.64% (fall of 5bps on the month).

Following yesterday’s reported bigger than expected 4.8% contraction in (annualised) Q1 US GDP (their much bigger hit is Q2) March Personal Income came in at -2% and Personal Spending -7.5% with the core PCE deflator at -0.1% as expected. Initial jobless claims last week rose by 3.8m, showing further evidence of moderating over recent weeks, but still taking the running six-week total past 30m. And ahead of tonight’s April Manufacturing ISM report, the Chicago PMI recorded 35.5 from 47.8, close to the 36.8 expected and the worse reading since March 2009.

The wild ride that is the oil market shows no signs of abating, WTI crude up 27% or $4 to $19.10. Brent is up 10% or $2.45 to $26.70. Other commodities haven’t fared as well, e.g. the LMEX index of base metals is off 1%, though iron ore futures are up 1.8%. Gold is -1.6% to $1,686.

On today’s economic calendar is the AiG Manufacturing PMI for Australia, ANZ NZ April Consumer Confidence and tonight, the US manufacturing ISM (consensus 36 from 49.1)

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.