Total spending grew 0.9% in June.

Equities have bounced back in a big way on hope that countries will start to ease restrictions and get more people back to work.

https://soundcloud.com/user-291029717/monumental-hope-from-markets-but-british-pms-condition-worsens?in=user-291029717/sets/the-morning-call

Heal the world, Make it a better place,

For you and for me And the entire human race – Michael Jackson

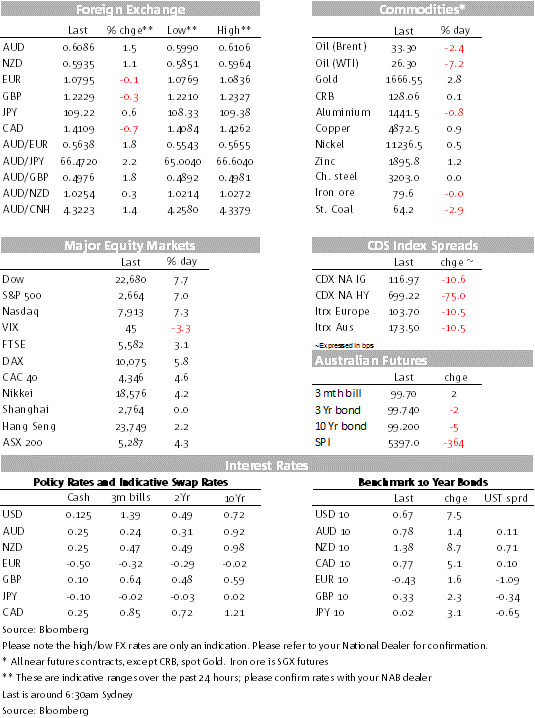

Risk assets had a good night buoyed by news that Covid-19 infections may be peaking while some European countries opened the door to the prospect of lifting some containment measures. US and European equities are higher while core yields have also moved up with the UST curve bear steepening. NOK and AUD have led the charge in G10 currencies with the latter up 1.45% and now trading at 0.6088.

We had positive Covid-19 night with stats coming out from Europe and the US suggesting the rate of infection may be peaking. Spain, which has the most cases in Europe, reported its lowest number of new cases in a fortnight and a fall in the number of deaths for the fourth day running. New cases and deaths in Italy continue to trend lower as well. In New York Governor Andrew Cuomo said the state’s virus-related death rate had been effectively flat for two days. However when we look at the US as a whole infection numbers are still rising, that said as we have seen in other parts of the world, social distancing measure should eventually result in a decline in the rate of infection.

Markets have also been buoyed by the prospect of an ease in some containment measures. Austria plans to allow small shops, DIY stores and garden centres to open from next week. Depending on the results, Austria might then allow certain other types of stores, such as hairdressers, to open from May 1st, although schools remain closed for now. Spain extended the lockdown of the country for another fortnight, to April 26th, but said restrictions on some non-essential industries would be softened after Easter. Spanish Prime Minister Sanchez said the country planned to expand its Covid-19 testing to those with no symptoms.

But the removal of social distancing measures need to be put in context. Austria, for instance, is talking about uplifting restriction to levels where Australia is at the moment, so a significant portion containment measures will remain in place. There are hopes New Zealand will lift some of its restriction, but again compared to Australia current restrictions are quite severe, as Jason Wong BNZ Market strategist will tell you, he can’t wait to get out and play round of golf!

Also the risk of a second virus outbreak should not be underestimated. Asian countries, such as Japan and Singapore, that have been successful in containing COVID-19 are now re introducing some restrictions as the risk of a new round of infection rises. So the conclusion then is that an uplift in containment measures is great news, but in all likelihood, the removal of containment measures will be very slow and the full economic impact remains unknown.

The risk assets have embraced the good news with the US leading the charge in equity markets, all major indices have ended the day up just over 7%. Gains in Europe have been a little bid modest in relative terms, but still pretty decent. The Euro Stoxx 50 is up 4.99% , the FTSE 100 closed at 3.08% and the DAX was 5.77%. Worth noting too that gains in both in Europe and the US were broad based with the energy sector also managing to end the day with gains despite new declines in oil prices (see more below).

The uplift in sentiment has also resulted in a move up in core global bond yields. The UST curve has bear steepened with the 10y Note up 7bps to 0.67%.

The Federal Reserve has announced another (yes, another) new facility. In conjunction, with the US Treasury, the Fed will provide term loans to banks backed by small business loans made under Paycheck Protection Programme (a scheme which provides loans to small businesses which keep employees on their books and helps keep cash flow running).

PM Abe announced a record and much larger-than-expected ¥108 trillion (~20%/GDP) fiscal package. Further details will be provided today. The package will reportedly include ¥6 trillion (~1%/GDP) in direct cash payments to households and ¥26 trillion (~5% of GDP) in tax deferrals and more social spending.

Risk and pro-growth currencies have unsurprisingly had a good day. We also had good news coming from the IMF with Managing Director Kristalina Georgieva confirming the Fund is preparing to offer short-term dollar loans to countries that lack enough Treasuries to participate in a Fed program which enables foreign central banks to temporarily exchange US debt for dollars.

The USD is little changed in index terms, but in G10 it has lost ground against commodity linked currencies with NOK leading the charge, up 1,78%, again not withstanding the move lower in oil prices. Safe haven curremcies, such as JPY have lost some of their appeal with USD/JPY now trading at 109.22 (+0.55%)

AUD has not been far behind, up 1.45% relative to levels this time yesterday. The AUD has been on a steady rise over the course of the overnight session, trading to a high of 0.6106 before easing a bit to now trade at 0.6088. Meanwhile in a similar patter, The NZD is up around 1% and trades this morning at around 0.5946.

The oil market remains in focus amidst uncertainty around whether Saudi Arabia and Russia can agree to supply cuts. An OPEC+ meeting originally scheduled to take place overnight was pushed out to Thursday amidst reports of renewed squabbling between the two countries. There will be a meeting of the G20 energy ministers on Friday, where Saudi Arabia and Russia hope to convince other major oil producing countries, including the US and Canada, to participate in supply cuts. Oil prices opened 11% lower yesterday morning but they have retraced some of that fall overnight. Brent crude oil is down 6% on the day, at around $28 per barrel. That’s still much higher (~35%) than the lows reached mid-last week.

Offshore credit markets continue to show signs of improvement, although spreads remain at crisis-like levels. In an encouraging development, the leveraged loan market looks set to reopen, with Laundry’s Inc – an owner of casinos and restaurants – offering a $250m loan. The funding won’t come cheap for the company, with pricing set at Libor + 14%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.