Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

The markets continue to ignore the US impeachment proceedings.

https://soundcloud.com/user-291029717/more-interest-in-trade-deal-than-impeachment-or-usmc-deal-australias-sideways-move?in=user-291029717/sets/the-morning-call

Do you have to, do you have to, do you have to let it linger – The Cranberries

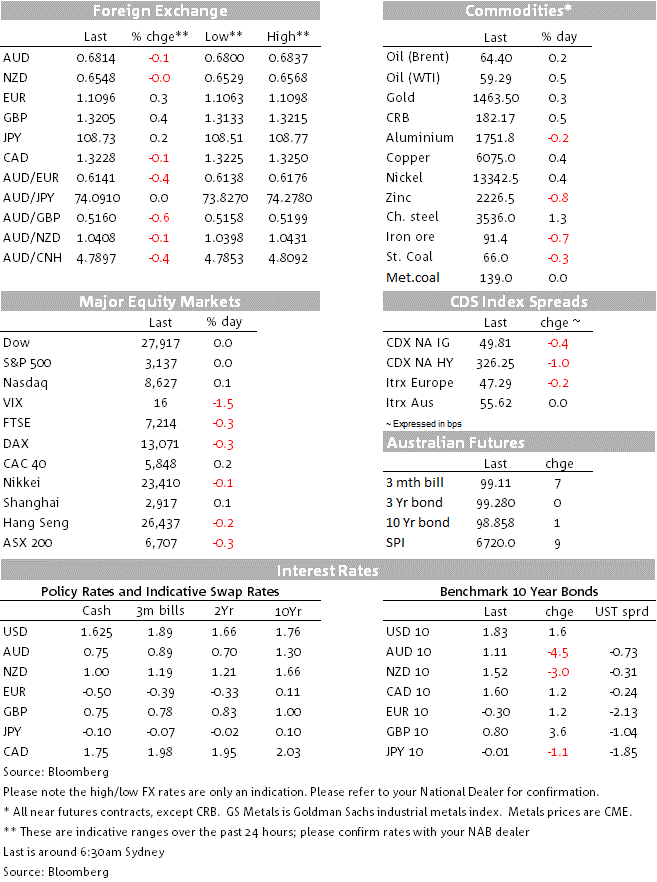

It’s been a night of fairly heavy news flows but not a whole lot of market volatility, certainly not in equities and bonds where US stocks are flitting between positive and negative readings for the main indices and Treasury yields have undergone mild bear flitting, 2s currently +3.7bps on Monday’s close and 10s +1.9bp. The DXY is -0.2%, driven by gains for EUR after a good ZEW report and GBP on further pricing in of an outright Conservative victory out of tomorrow’s general election.

The biggest ness, or perhaps that should read none news, overnight are various reports suggesting that the December 15 deadlines for the imposition of new tariffs on $160bn worth of Chinese imports is likely to be deferred, though President Trump’s economic adviser Kudlow says this is not yet agreed by Trump. Assuming it is, then trade policy uncertainty is set to linger well into the next decade (now less than three weeks away, wow). This has very been the emerging consensus heading into the weekend deadline, hence the reports have failed to spark any market volatility.

The economic news flow meanwhile has almost all been on the positive side of the ledger, and from three continents, including latest China credit data, the NFIB small business survey and the German ZEW survey.

China’s November credit and money supply data released after we went home last night shows the broad s the broad Aggregate Financing measure rising by ¥1,750bn, more than double the October rise and well above the ¥1,485bn consensus expectation. The narrower New Yuan loans measure rose by ¥1.390bn, up on ¥618.9bn last time and ¥1,200bn expected. After the weakening trend evident in both the September and October figures, then alongside recent data showing all four (official and private) PMI measures back above 50, a ‘gentle turning point’ -as RBA Governor Lowe might choose to describe it – looks like it is the process of being achieved for the Chinese economy.

The German ZEW survey, though not as influential as the IFO survey, being comprised of a survey of financial analysts (case in point – in a previous life I was a survey participant myself) saw the expectations reading jump from -2.1 to 10.7 it first positive reading since April and best since February 2018. The Current Situation reading was less impressive but still up on November, to -10.9 from -24.7. EUR/USD rallied by about 15 pips on the news, gains which have since extended to 0.3% vs. Monday’s New York close, the pair back flirting with a 1.11 handle having briefly spent time below 1.10 at the end of November.

Positive US news came courtesy of the latest NFIB Small Business Optimism survey, which at 104.7 has now fully recovered the slippages evident though the US summer and early Autumn. Not back to the tax cut juiced levels of 2018, but still very strong in absolute terms.

Included confirmation that two articles of Impeachment against President Trump would be but to the House of Reps. next week – to no-one’s surprise hence no reaction – and news that Nancy Pelosi, the Democratic Speaker of the House of Representatives, had reached a deal with US president Donald Trump to allow ratification of USMCA.

According to the FT, Ms. Pelosi’s announcement on Tuesday followed months of wrangling with Robert Lighthizer, the US trade representative, and parallel talks with officials in Canada and Mexico to secure changes to the original text. “It’s a victory for America’s workers, it’s one that we take great pride in advancing,” Ms Pelosi said, describing it as “infinitely better” than the original deal reached by Mr Trump.

This didn’t stop POTUS tweeting “America’s great USMCA Trade Bill is looking good. It will be the best and most important trade deal ever made by the USA. Good for everybody — Farmers, Manufacturers, Energy, Unions — tremendous support. Importantly, we will finally end our Country’s worst Trade Deal, Nafta!”. The FT notes Democrats successfully pushed for tighter labour standards, strengthened environmental protections and the removal of advantages for pharmaceutical companies in exchange for allowing a vote on USMCA in Congress. Ms Pelosi was able to extract enough concessions from Mr Trump for the deal to be endorsed by the AFL-CIO, the largest trade union federation. The union is highly influential in Democratic politics and has traditionally opposed trade deals. Just as we go to hit send and putting a slight dampener on the news, Senate majority leader Mitch McConnell has been on the wires saying that the Senate won’t finish USMCA this year.

GBP has slightly exceed the gains chalked up by the EUR, up 0.4% against the USD and which together with slight slippage in the AUD means that the AUD/GBP cross is now trading comfortably below 0.52 (0.5161) and its lowest level since just before the June 24 2016 Brexit Referendum result. UK data showing monthly GDP unchanged in October, industrial production up 0.1% and manufacturing output +0.2% and worse than expected trade figures, failed to stand in the way of gains as market moves to further price in an outright majority for the Conservative when the result of Thursday’s election are revealed, which should be as early as Friday morning our time.

AUD continues to exhibit poor price action, -013% to 0.6814 with only the JPY and NOK weaker in the last 24 hours. There was no reaction yesterday’s NAB business survey, which showed confidence and conditions stabilising at below par levels, or to comments from RBA’s Governor Lowe in Q&A post speech on payments. Lowe said “The surprise in the GDP data was weakness in consumption growth, given extra income from tax cuts. I’m still confident, given extra time, people will spend extra income. It’s quite possible that spending takes a little longer…in the current environment there’s a high level of debt, and households are paying down debt first. Says weakness of Q3 consumption ‘does not have any particular message for future’.

At 9:00 AEDT the final UK YouGov MRP poll is released. Remember the MRP poll released 27 Nov showed the Tories on course for a 68 seat majority at 359 seats vs 211 for Labour and 43% vs 32%. Because of the methodologies used and the large sample size, today’s poll still won’t represent most recent thinking, but will still likely nudge GBP one way or the other if better/worse.

Westpac November consumer confidence at 10:30 AEDT (97.0 in October, +4.5% on September)

The NZ government’s half-year economic and fiscal update (HYEFU) is at 11:00 AEDT 1pm, where we expect to see more colour on the “significant” fiscal stimulus that lies ahead, recently alluded to by the Finance Minister. Easier fiscal policy takes the pressure off monetary policy and is NZD-supportive, with little concern about government debt levels compared to other countries

US CPI, expected at +0.2% in both headline and core (ex food and energy) terms (2.0% and 2.3% yr/yr respectively)

FOMC concludes its two-day meeting, with the outcome, new economic projections and ‘DOTS’ due at 6:00 AEDT Thursday, followed by the Powell press conference. No change in policy is confidently expected and with the consensus, and our own expectation, for the new ‘DOTS’ that they will show a median expectation for no change through 2020.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.