Total spending grew 0.9% in June.

Astra Zeneca announced the results of their trials, with efficacy up to 90 percent with a drug that is cheaper to produce and easier to distribute.

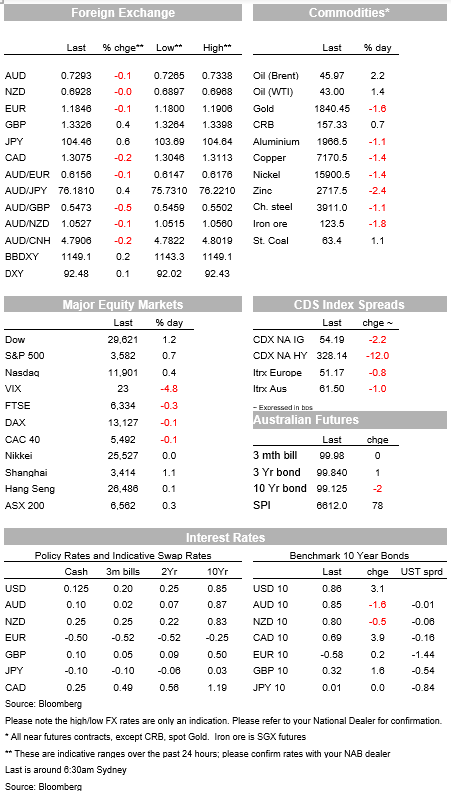

Risk sentiment received a boost, and the USD fell further, at the start of the European day Monday on news from AstraZeneca that its experimental vaccine, produced in conjunction with Oxford University, had an average success rate of 70% across all triallists, but rising to 90% when administered a certain way (i.e. half a dose initially with a full dose a month or so later). Also positive was their claim that the drug only need be stored at standard refrigeration temperatures and was cheaper than the Pfizer and Moderna versions, both of which, recall, claim success rates near 95%. Hence AstraZeneca’s immediate application to the WHO for an Emergency Use Authorisation accompanied by the suggestion the vaccine be designated for less well-off countries. An hour or so ahead of the NYSE close, equity gain are nevertheless quite modest and led by the previously out of favour industrials, airlines and other travel related stocks and financials, seen as relative beneficiaries of the successful deployment of vaccines next year. Hence the Dow is currently up 1.3%, the S&P 0.6% and NASDAQ 0.5% (all rallying as I write).

Notwithstanding the AstraZeneca news, suggesting that a lot of positive vaccine-related news is now in the price. There was also not much support from news that social distancing restrictions will be eased in time for the Christmas holiday period. In England, the stay-at-home order will be lifted on 2 December, to be replaced by a tiered system of regional restrictions. In France, tomorrow President Macron will detail a gradual end to the second lockdown.

There was not a whole lot of reaction to the incoming stream of European PMI data that, in the Eurozone, shows a slowing in the rate of expansion in manufacturing but not by as much as expected but an outright slowing in service sector activity by more than expected. Thus at the pan-Eurozone level, the manufacturing PMI slipped to 53.6 from 54.8 (53.2 expected) and services to 41.3 from 46.9 against 42.0 expected. German manufacturing hardly slipped at all, 57.9 from 58.2 while services fell to 46.2 from 49.5. Activity in France, which has been subject to broader and more stringent lockdowns than most other European countries, fell by more – manufacturing coming in at 49.1 from 51.3 and services slumping to 38.0 from 46.5.

In contrast, UK PMI data surprises by its strength, manufacturing rising to 56.7 from 52.1 while services were hit hard due to the near-nationwide lockdown that has been in place for about two weeks at survey time, falling to 45.8 from 51.4, though this was better than the 43.0 expected. Sterling didn’t benefit much from this, having already been riding high ahead of the data on ongoing optimism toward a UK-EU trade deal being struck as early as this week, albeit hard evidence that this will be so remain lacking, and then fell away alongside broad based USD strength following the release of the US equivalent PMI data.

Markit US PMIs have to date always played a (poor) second fiddle to the more established ISM series, but no so overnight where the undeniable strength in both the manufacturing and services readings couldn’t be ignored. Manufacturing rose to 56.7 from 53.4 and services to 57.7 from 56.9, both comfortably in excess of the 53.0 and 55.0 consensus estimates for manufacturing and services respectively. It your country is not locked down to anything like the extent of elsewhere in the world, your activity will be stronger, is the perhaps blindingly obvious take-away from the US data, though in the face of weakening labour market statistics, it is also testament to the fact household are for the most part still cashed up (plus of course, employment did rise sharply in October, though frequency data suggest this trend won’t survive year-end).

There was significant market impact from the US data, much more evident in currencies than equities or bonds. The Latter does though sees US 10-year Treasuries up 3.3bps in yield terms to 0.857 with a couple of hours to go in the NY session. This shows up in a stronger USD/JPY, up 0.6% to Y104.50 and the biggest G10 mover of the week so far. GBP still leads the G10 pack but is well back from its intra-day high of $1.3398 at 1.3325. CAD is also a touch firmer helped by firmer oil prices (Brent +$1 to $45.94, WTI +$0.57 to $42.98) while all other G0 pairs are softer. AUD is back from an intra-night high 0.7338 to 0.7294 – a move which further highlights the 0.7340 level as currently important technical resistance.

Not helpful to the AUD’s cause in so far as it helped produce a weakening in USD/CNH from 6.55 to above 6.58, was a Dow Jones report that Senior Trump Administration officials are pushing for new hard-line measures against China, possibly creating an informal alliance of Western nations to jointly retaliate when China uses trading power to coerce countries. The officials said that the plan was sparked by recent Chinese economic pressure on Australia. This followed an earlier report by Reuters that the Trump Administration was close to issuing a list of 89 Chinese aerospace and other companies that would be unable to access US technology exports due to their military ties.

News just in courtesy of the Wall Street Journal is that former Fed chair Janet Yellen, fired as Fed chair by President Trump remember, is to be Biden’s pick for US Treasury Secretary. A strong spirit of cooperation between the Fed and Treasury is one thing of which we can now be assured.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.