Online retail sales growth slowed in May following a fairly strong April

Insight

There’s a little apprehension in the markets this morning because the US China trade deal might not be a done deal.

https://soundcloud.com/user-291029717/more-talk-before-truce?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s research support please let your company’s representative know.

Well, I woke up this morning with the cold water, With the cold water, with the cold water – Tom Waits

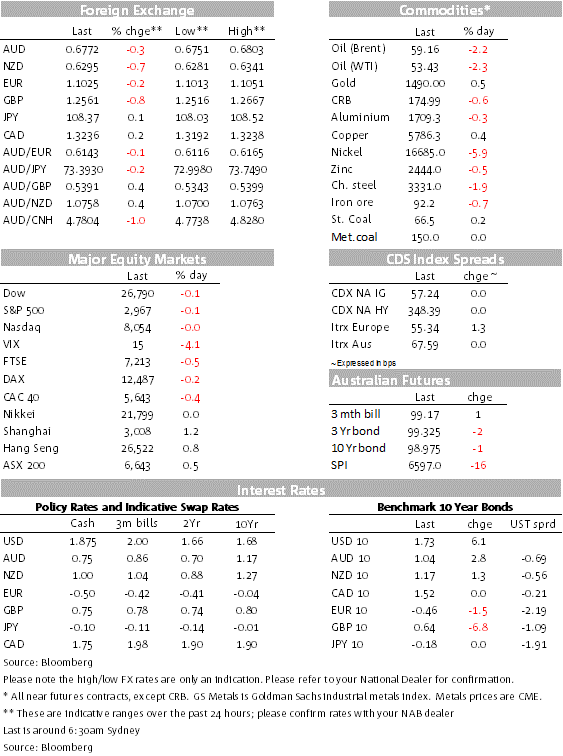

There is a Justin Beiber/Major Lazer song titled Cold Water out there which my colleague Tapas Strickland might have been inclined to use today (given his popish tendencies). Instead I have gone with Tom Waits’ Cold Water, not only the lyrics capture the mood from the overnight session, but Waits’ voice also gives you that feeling of someone dealing with a massive hang-over after a messy night. So, after a week that ended with three solid gains in major global equity markets and a decent rise in core global yields, we have started the new week in a more cautious mood with the US-China trade vibes now starting to show some signs of friction. China wants more talk time to iron out details and it also wants the tariff stick to go away, but overnight comments from Treasury Secretary Steven Mnuchin suggests otherwise. Light holiday trading in US equities don’t reflect the risk off tone evident in European equities and the commodity space. The USD is stronger across the board with GBP the big underperformer amid doubts over a potential Brexit breakthrough.

It may well be that a fair bit has been lost in translation, after President Trump upbeat version of events not only showcasing the huge amount of agricultural products that China was now going to buy from the US, the President also left us with the impression that a deal was essentially a done thing, barring the not so inconsequential need to write a legal document. Media and official reports from China have been less emphatic with a China’s Ministry of Commerce statement merely noting that “the two sides have made substantial progress” and “agreed to work together in the direction of a final agreement.”. Now Bloomberg reported overnight that China has requested more talk time iron out details of the deal including asking for the removal of the planned tariff hike in December in addition to the hike scheduled for this week.

Bloomberg also suggested Vice Premier Liu He, China’s top negotiator, could travel the US again in order to finalise the written deal. On the positive side there is still evidence from both side willingness to strike a deal. But speaking to CNBC overnight, Treasury Secretary Steven Mnuchin said that if a deal was not written over the coming weeks, then the planned tariffs on $160bn will go ahead starting December 15th. For now there is no evidence the US is planning to remove its tariff leverage and we have a been here before where previous US-China ‘agreements’ have subsequently broken down amidst misunderstandings among the two sides. So caution is warranted.

The US and Japanese have been on holiday on Monday, so trading activity has been lighter than usual. US equities did trade overnight, but the light trading environment suggests that the muted price action which ended with the S&P 500 down 0.14% and the NASDAQ -0.10% probably doesn’t truly reflect the actual market sentiment. The US Treasury market was closed while the implied yield on the 10 year Treasury note future points to a 2bp decline in rates.

A risk off tone is more evident with all major European equity indices closing down between 0.30% and 0.40%. Moves in the commodities space also reflect a cautious mood with oil prices down over 2%, while lead is -2.34% and the LMEX index is -0.51%.

The USD is mildly stronger across the board with the DXY index +0.18% while BBDX is +0.14%. Looking at G10 FX GBP is the big mover down 0.71% to 1.2553 as market participants start to question whether there is enough time for the two sides to do a deal ahead of the EU Summit that takes place on Thursday. On this score Finland’s PM, Antti Rinne, whose country holds the EU’s rolling presidency, said that he didn’t think it’s possible for the bloc and the UK to agree on the terms of a Brexit deal in time for the summit of leaders that starts Thursday. The EU plans to decide on Wednesday whether there will be a deal for leaders to sign during the summit and has ruled out negotiating during the actual meeting of leaders.

The AUD and NZD have also lost ground against the USD, down 0.26% and 0.60% respectively. AUD now trades at 0.6774 and NZD is at 0.6295, both antipodean currencies underperformed on the back of weaker than expected Chinese trade data, although the CNY itself is actually stronger on the day.

The only major global data released overnight was the Empire manufacturing survey, the first of the regional Fed surveys to be released for October ( out a day earlier than expected). It bounced to 4 in October from 1 the previous month, although it remains at subdued levels, consistent with weakness in the broader manufacturing sector.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.