We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

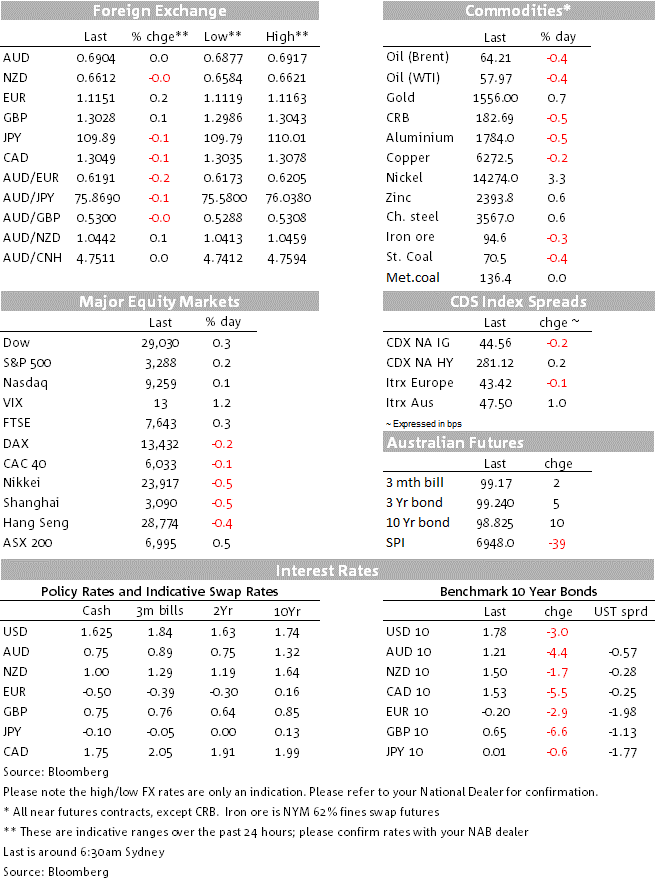

Equities have posted further gains and new record highs.

https://soundcloud.com/user-291029717/us-deal-done-new-highs-again-for-equities?in=user-291029717/sets/the-morning-call

Signing of the US-China phase 1 trade agreement was all set to take top billing overnight. In markets though it was upstaged by a big miss on UK CPI which was the weakest in three years with Core CPI at 1.4% y/y against 1.7% expected. While there were a fair share of one-offs (e.g. airline fares fell -8.5%), inflation will struggle to rebound in Q2 and pricing for a BoE rate cut at the January meeting rose to around a 70% chance from 50% previously. Comments by the BoE’s Saunders on the need for a cut also added. Moves in UK rates (10yr Gilt yields -6.6bps to 0.65%) dragged down global rates with US 10yr yields -2.3bps to 1.79%. Second tier US PPI also added to the view of a subdued global inflation picture. The signing of the US-China trade deal had little impact on markets given the build-up, though equities initially rallied to fresh highs before reversing with the S&P500 now +0.0% to 3,286. Global FX was little moved, with the USD (DXY) -0.2% with EUR +0.2% and USD/Yen -0.2%. GBP initially did break 1.30 (low 1.2986) on the soft CPI figures, but manage to claw back on USD weakness to finish +0.1% to 1.3030. AUD was little moved overnight (-0.% to 0.6900) with the signing of the trade deal having little impact on CNH (currently 6.8898).

Core CPI missed by three tenths, coming in at 1.4% y/y against 1.7% expected and prior. Headline CPI also missed at 1.3% y/y against 1.5%. While there were plenty of one-offs (e.g. airfares fell 8.5% and accommodation -2.2%), inflation is unlikely to rebound in Q2 given likely declines in electricity and natural gas prices, as well as from sterling’s modest appreciation. Pricing for a BoE rate cut at the upcoming January meeting now sits around 70%, up from 50% previously, and is fully priced by May. In recent days pricing has lifted following the comments from a number of BoE officials. Saunders was out again overnight advocating for cut (“if we defer easing near-term and, in the event of persistent economic weakness, face the need for greater easing later on, then [that] risks…a low-inflation trap”).

The US and China signed the phase one trade deal. Details of the deal are now available (it is 94 pages long, see link for details). The agreement largely confirms what was speculated about in recent days (China ramping up purchases by $200bn over two years, language on IP and forced technology transfer, removing barriers to help US financials expand in the Chinese market, and a commitment by China not to devalue its currency). President Trump called the deal a “momentous step”, though in reality the agreement is more akin to a truce for 2020 given further tariff reductions are off the table until after the November Presidential elections. US-China tensions are also likely to be an ongoing feature regardless of the occupant in the White House with leading-Democratic Presidential candidate Biden called many of the provisions in the deal as “vague, weak, or covered by previous announcements and existing agreements”. The much mooted enforcement mechanism also entails several rounds of consultations before the taking of “remedial measure in a proportionate way”.

There was limited reaction to the agreement in CNH, with most of the provisions having been well flagged previously. Lack of CNH reaction to the deal kept the AUD little moved overnight (+0.0% to 0.6905). Equities though initially rose to fresh record highs, before reversing with the S&P500 +0.0% to 3,286. Lower yields also supported. White House economic advisor Kudlow also told CNBC that the administration was working on a second round of tax cuts, aimed at the middle class – though much would depend on the outcome of the November elections and questions remain around financing given the US deficit hit 1 trillion in 2019, the highest since 2012. Financial stocks underperformed after softer than expected earnings from BofA and Goldmans.

US PPI missed expectations with Core PPI at 1.1% y/y against 1.3% expected. The Empire Fed Manufacturing survey rose slightly to 4.8 from 3.5 and remains in a narrow range overall. The Beige Book was also just released with most Fed districts reporting modest to moderate growth, while tariff and trade uncertainty weighed on some businesses. There were scattered reports of declining prices in some manufacturing industries, while labour shortages were a factor constraining growth. The Fed’s Kaplan also hit the wires stating he believed risk assets had been boosted by the Fed’s recent expansion of its balance sheet and rate cuts last year.

Industrial Production was a tad softer at 0.2% m/m against 0.3% expected, along with the Trade Balance (19.2bn against 22bn expected).

Finally, the Swiss Franc extended gains with EUR/CHF -0.3% to 1.074. The moves coming in wake of the currency manipulator watchlist tag and on the more positive risk-on backdrop.

Another quiet day domestically and internationally. This morning we get Australian home loan approvals for November which should show continued strength given strong house price figures last year. International focus is likely to be on the ECB Minutes and then onto US Retail Sales.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.