NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The markets reacted positively to indications from President Trump that a trade deal with China could be close.

https://soundcloud.com/user-291029717/new-trade-hope-no-smoking-gun-more-brexit-noise?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s Market Research support please let your company’s representative know.

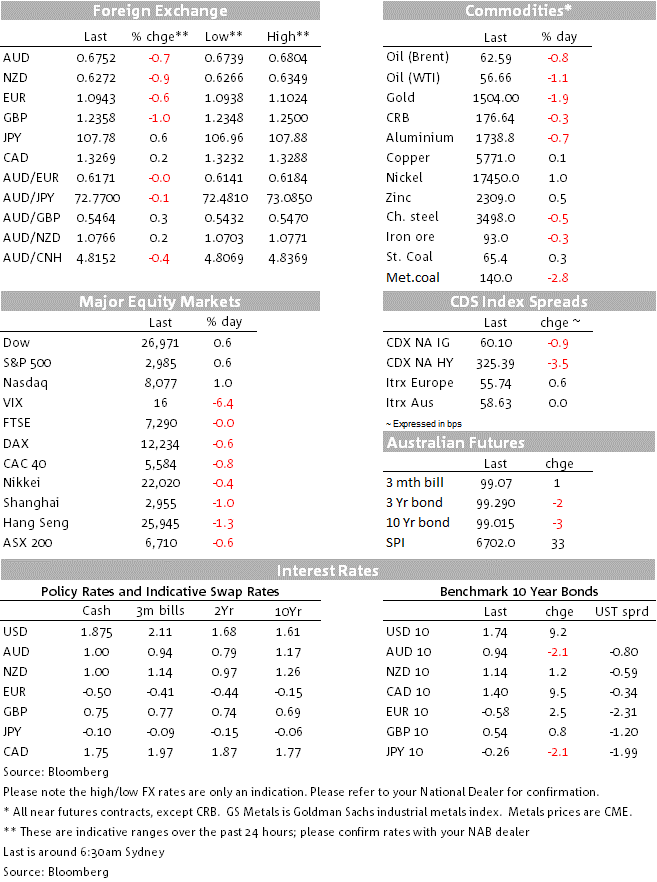

“You Need to Calm Down” is the message that markets took from political developments overnight with release of the Trump-Ukraine call report showing no smoking gun for impeachment – though is still enough to keep an impeachment inquiry alive. The release of the call report also timed in with Trump talking up prospects of a China deal, stating a deal “could happen sooner than you think…we are getting closer and closer…there is a good chance US and China will make a deal”. Both the USD and yields popped higher on the news, with USD (DXY) +0.7% to 99.01 and US 10yr yields +9.0bps to 1.74%. USD gains were across the board with EUR -0.6%, USD/JPY +0.6%, AUD -0.7% and NZD -0.9%. Sterling was the biggest loser with GBP –1.0% to 1.2356 as the UK Parliament re-convened after the court decision, but with PM Johnson remaining defiant. The other major development was in oil where a large inventory build has seen WTI retrace all the Saudi-led moves with WTI -1.4% to $56.50. Equities are unsurprisingly higher on the positive news with the S&P500 +0.6% to 2,985.

The call notes (note they are not explicit transcripts) contained little direct evidence of Trump saying he would explicitly cut foreign aid to pressure the Ukrainian President. However, importantly the notes also said Trump did urge Ukraine to work with Attorney General Barr to investigate Biden and his son (for more analysis see Politico). The later will likely keep Democrats pursuing their impeachment inquiry, but with little chance of success – especially given the Republican controlled Senate. Either way, impeachment talk will likely distract the US administration at least to the end of the year.

Coinciding with the call notes, President Trump talked up the prospects of a near-term US-China deal, stating a deal “could happen sooner than you think…we are getting closer and closer…there is a good chance US and China will make a deal”. A cynical person would say those comments were aimed at deflecting attention away from the Ukraine situation. Nevertheless, over the past couple of days there have been a number of positive movements on the Chinese side and yesterday it was reported Chinese companies are preparing to purchase more US pork. The next high-level trade meetings are likely to take place around 10-11 October.

The USD popped higher with DXY +0.7% to 99.01 and touching 2019 highs. There appears nothing to stop to the grind higher in the USD given US economic outperformance, continued trade rhetoric from Trump, and a Fed hesitant to cut rates further for fear of encouraging the Administration in its trade war escalation (see Fed comments below). The gains in the USD were broad-based, though Sterling was the underperformer with GBP -1.0% to 1.2358. The UK Parliament resumed yesterday, and amid the chaotic scenes there was little headway with PM Johnson remaining defiant and arguing the court was “wrong” in its ruling and again sought a general election (note 2/3rds of MPs need to vote for an election and they have been unwilling to do so unless the Brexit date is extended).

Fed speak continues to point to the Fed not taking aggressive action, but rather drip feeding rate cuts as necessary. The Fed’s Evans (dove, voter) indicated that while he is “open minded to additional action if the data comes in that way…But at the moment we are well positioned” and also noted his forecasts do not include another cut. The Fed’s Brainard (voter) took a more cautious view, noting that trade policy uncertainty has “a material negative impact on the health of the economy”, while Kashkari (non-voter) repeated his dovish leaning stating “I could easily see justifying 50bps lower than it is today”. Overall though the comments we have had over recent days points to a Fed pushing back on pressure to take dramatic action – harking back to what former-NY Fed Dudley argued on the choice that officials face (where to “enable the Trump administration to continue down a disastrous path of trade war escalation, or send a clear signal that if the administration does so, the president, not the Fed, will bear the risks”).

The repo market continues to be an issue, but the Fed at least is taking action. Overnight they got $92bn submitted for a repo cap of $75bn. In reaction the Fed has announced it will increase Thursday’s overnight repo operation to $100bn and hold a $60bn one for a 14-day term repo (upsized from an initial $30bn). The Fed’s Evans stated that the repo issues could be sign that balance sheet is tighter than anticipated and the Fed may be able to avoid future repo problems by increasing its balance sheet, while Kashkari continues to argue for a standing repo facility.

Data was sparse with only US New Home Sales overnight of note. Home Sales were much better than expected at 7.1% m/m against 3.8% expected, though merely reverses the sharp -8.6% fall seen last month. The data though was released around the same time as the Trump-Ukraine and Trump-China headlines and likely added to the positive tone.

Another German official has resigned from the ECB in protest over bond purchases with Lautenschlager resigning overnight; for those with a long memory her moves echo Jürgen Stark’s resignation in 2011 over sovereign bond purchases in response to the European debt crisis. The news had little market reaction, but emphasises the divisions on the ECB board.

Yesterday the RBNZ kept rates on hold as expected, noting “new information since the August Monetary Policy Statement did not warrant a significant change to the monetary policy outlook”. The Statement was neutral, though it is widely expected the RBNZ will cut rates in November, especially if the RBA cuts rates by then. The NZD did initially rise on the news as some were perhaps expecting a more dovish statement, but has more than reversed with the NZD -0.9% to 0.6271 overnight. My colleagues at BNZ not only pencil in a November cut, but also one for February.

While there was little news in Australia, RBA pricing has moved higher with around a 73% chance of an October rate cut after it had fallen to 60% following Governor Lowe’s speech earlier this week. Late yesterday a number of journalists have come out hinting Martin Place is pencilling in an October cut. The AFR’s Karen Maley emphasis the role of the exchange rate, staying if the RBA fails to match rate cuts overseas then the exchange rate would strengthen and reduce competitiveness of its exports and dampen domestic economic activity (see link for details). The Australian/Dow Jones’ James Glynn is more explicit stating Lowe has set the scene for an October cut (see link for details). Finally an unusual article by the SMH’s Jessica Irvine may hint of the RBA contemplating negative rates being in its unconventional arsenal (see link for details).

The AUD largely moved in sync with the USD, with AUD -0.7% to 0.6752. There is little on the horizon domestically to shift the AUD, with moves in AUD likely to be driven by any developments in US-China discussions.

Finally, the oil price has largely unwound its moves following the Saudi drone attack with WTI at $56.66 and Brent at $62.56. Overnight US oil inventories rose 2.4m barrels compared to an expectation of a draw of 250k. The reversal in the oil price has seen also seen US 10yr break-evens given up their earlier oil price moves with breakevens now 1.59%

A mostly quiet session ahead with little to move markets scheduled.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.