Online retail sales growth slowed in May following a fairly strong April

Insight

There was renewed hope a phase one trade deal could be reached between the US and China by Christmas.

https://soundcloud.com/user-291029717/new-week-new-hope?in=user-291029717/sets/the-morning-call

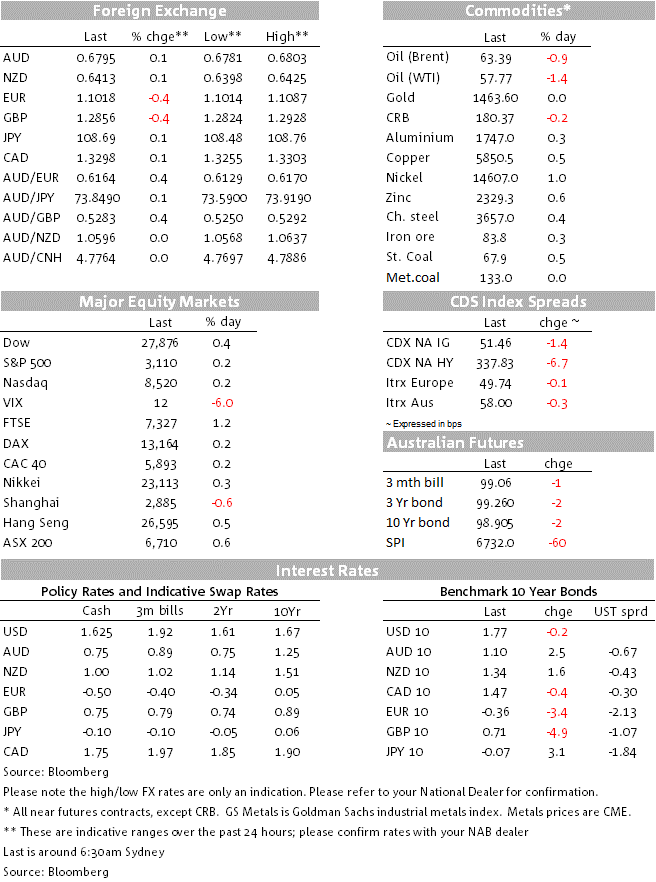

Europe dominated Friday’s action with a poor Eurozone Services PMI and a truly awful set of UK PMIs seeing both Bunds and Gilts rally, with GBP and EUR both lower. German 10yr Bund yields fell -3.4bps to -0.36% and 10yr Gilt yields fell -4.9bps to 0.71%. Yields in the US though shook off the moves with US economic data much better than expected and continuing to illustrate the US economy is the least dirty t‑shirt in the global laundry basket. The USD (DXY) correspondingly rose 0.3% to 98.27, driven by weakness in EUR (-0.4% to 1.1018) and GBP (-0.3% to 1.2859), while USD/Yen was broadly unchanged at 108.69. In equities, the FTSE outperformed on GBP weakness, +1.2% while the S&P500 was little changed at +0.2% to 3,110. As trade opens for the week the AUD is up +0.1% to 0.6795 with mildly positive weekend trade headlines – the latest being Beijing has said it will raise penalties on violations of intellectual property rights, one of the ongoing issues in the US-China trade dispute. Europe’s dominance of price action is inspiration for today’s song title, “From Paris to Berlin” – the 2005 Eurodance hit from Danish group Infernal. Fun fact, a cover was also recorded called “From Taipei to Beijing” in 2006.

A lot of numbers, but the important takeaway was the ongoing decline in the manufacturing sector is now spreading to the larger services sector, a worrying sign for the global economy. The Services PMI fell to 51.5, from 52.2 (well below the 52.4 expected) and dragging the overall composite down to 50.3. For those looking for a silver lining the Manufacturing PMI was slightly better than expected at 46.6 against the 46.4 consensus, driven by better reads from France (Manufacturing PMI 51.6 v 50.9e) and Germany (Manufacturing PMI 43.8 v 42.8e). However, that also means that the rest of the region likely slipped into decline for the first time since 2013. No surprise then to see the ECB’s Lagarde call for a pick-up in public investment. Also potentially important for the outlook was the ECB President flagging a strategic policy review, the first review of the ECB’s objectives and tools since 2003. In terms of what to expect, the Bundesbank’s Weidmann said he would oppose any shift to a more symmetrical inflation target that accepted a period of above target inflation.

The UK PMI’s were even weaker with Manufacturing at 48.3 and Services at 48.6. Both of these reads are consistent with mild recessionary conditions in the UK – a mapping equation would point to a 0.2% decline in Q4 GDP from these figures. While significant, the data does not add anything new to the notion of what the UK economy needs is certainty, something that is unlikely until after the December 12 election. On the election, latest polls have the Conservatives at 42 and Labour trailing at 30. Interestingly while Brexit remains the number one concern for voters, the polls now have Health and the Economy being a close second – something that Labour is banking on.

There was little in terms of new news. President Trump said there is a “very good chance” of reaching a trade pact with China, but he’s “not anxious to make it” given the unrest in HK: “We have to stand with HK but I’m also standing with President Xi, he’s a friend of mine, he’s an incredible guy.”. On the weekend, China said it will raise penalties on violations of intellectual property rights, interpreted as an attempt to address one of the sticking points in trade talks with the US. China also said it would look into lowering the thresholds for criminal punishments for those who steal IP, according to guidelines issued by the government on Sunday.

Highlighting again the resilience of the US economy and that while global growth has slowed, the US economy remains the least dirty t-shirt in the laundry basket. The US Manufacturing PMI came in at 52.2 against 51.4 expected, while Services also beat at 51.6 against 51.0 expected. Consumer Sentiment also beat the flash estimate at 96.8 against 95.7 expected, while tariff impacts are a less of a concern with consumers with only 24% negatively mentioning tariffs compared to 36% two months ago.

AUD has opened the week +0.1% to 0.6795 on those mildly positive weekend trade headlines. It will be an important week for the AUD with RBA Governor Lowe speaking on “Unconventional Monetary Policy: Some Lessons from overseas” on Tuesday, while key pre-GDP partials are also released in the week (see Coming Up for details).

Domestically the week ahead is very busy with RBA Governor Lowe speaking on “Unconventional Monetary Policy: Some Lessons from Overseas” on Tuesday at the annual ABE Dinner. Also speaking the same day is Deputy Governor Debelle on “Employment and Wages”. Dr Lowe’s keynote speech will provide an opportunity to outline the RBA’s view on various unconventional policy options and, perhaps, at what point the RBA thinks such a programme would be warranted. The RBA has previously said that international experience suggests unconventional policy is most effective when a package of measures is used. The Governor comments to date suggests his preference is for QE in the form of buying government bonds, and not negative rates which he describes as being very unlikely. With that backdrop NAB has recently published a cross-asset note on what a QE program may look like in Australia and the potential impact of such a program (please email Tapas.Strickland@nab.com.au if you would likely a copy). Briefly, looking at international analysis we estimate a QE programme of about 6% of GDP (or $115bn of bond purchases) would be needed to lower unemployment towards NAIRU of 4.5% and to lift inflation to target. Focusing on the impact that could have on financial markets, we estimate it could reduce 10yr government bond yields by roughly 35bps (range 10-70bps) and lower the exchange rate by around 1.8% (range 0.5-3.5%). As for how likely such a program is we will have to listen closely to what Governor Lowe says on Tuesday.

The key GDP partials of Construction Work Done (Wednesday) and Capital Expenditure (Thursday) are due, likely to confirm another soft GDP print that will be released on 4 December. Anecdotes and surveys have recently pointed to some delays in infrastructure investment, while building approvals continue to point to further falls in dwelling construction – NAB looks for downside risks in both prints.

We get the German IFO and the Fed’s Powell today, US PCE inflation on Wednesday and the Eurozone CPI on Friday. A reminder too that the US has the Thanksgiving Holiday on Thursday (bond and equity markets are closed).

It is mostly quiet domestically with no significant data scheduled. Overseas focus will be on the German IFO and a speech by the Fed’s Powell:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.