We expect growth in the global economy to remain subdued out to 2026.

Insight

US and EU equities have closed with modest gains while core yields extended Friday’s rise. The Fed Senior Loan Officer revealed a modest deterioration in lending standards alongside a drop in demand for loans, so no evidence of an imminent credit crunch. The USD is little changed with NZD leading a modest outperformance by pro-growth currencies.

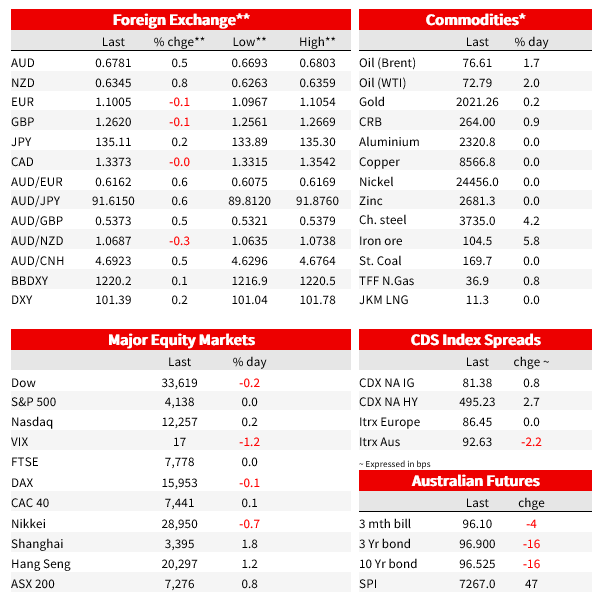

AU: NAB business conditions (net%), Apr: 14 vs. 16 prev.

AU: Building approvals (m/m%), Mar: -0.1 vs. 3.0 exp.

GE: Industrial production (m/m%), Mar: -3.4 vs. -1.5 exp.

It has been a quiet start to the new week. US and EU equities have closed with modest gains with the S&P 500 essentially flat on the day. Core yields have extended Friday’s rise with the UST curve bear flattening, issuance and pairing of Fed rate cut expectations factors at play. The Fed Senior Loan Officer (SLOOS) revealed a modest deterioration in lending standards alongside a drop in demand for loans, so no evidence of an imminent credit crunch. The USD is little changed with NZD leading a modest outperformance by pro-growth currencies. AUD starts the new day at 0.6781.

The much-anticipated Fed’s Senior Loan Officer Survey was Monday’s major calendar event and in the end details in the report were not as bad as some may have expected. The survey revealed a modest deterioration in lending standards to business at a rate that was slightly higher than in January . But, after concerns over the health of US regional banks, the good news is that the survey did not (yet) reveal evidence of a major credit crunch. Of note, the drop in demand was significant and standards are expected to tighten further. Overall and like many other leading indicators of the US economy details in the survey (supply/demand metrics) are consistent with a weaker economy ahead.

After trading in and out of positive territory, the S&P 500 ended the day little changed, up 0.05% on the day. Communication Services was the outperforming sector, gaining 1.27% while Real Estate and Industrials were the underperforming ones, down 0.68% and 0.37% respectively. In company news, Tyson Foods, fell 16% on a weak profit result and reduced sales guidance, with the company experiencing challenging market conditions across all three of its core protein categories, a combination of rising costs and consumers trading down to cheaper foods. The tech heavy NASDAQ closed the day 0.18% higher with AI-capable chipmakers Advanced Micro Devices and Nvidia leading the day’s gains alongside Alphabet. Earlier in Europe the EuroStoxx 600 index climbed 0.35% with most regional indices closing the day with modest gains.

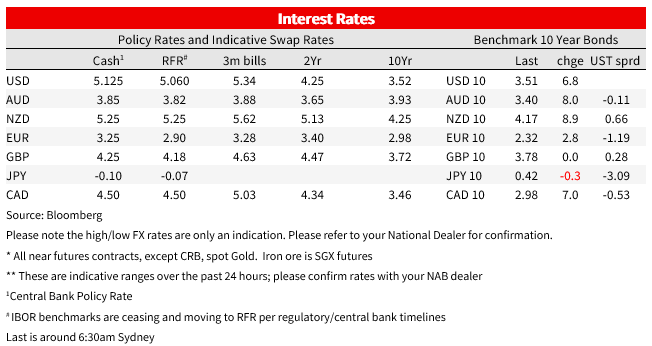

Core global bonds extended the move up in yields recorded on Friday with the UST curve again showing a bear flattening bias. The move up in UST yields has been spurred by expectations of corporate bond issuance (~$30bn) alongside $96bn in UST planned issuance for this week. Front end yields have led the move up in yields with pairing in Fed rate cut expectations also fuelling the move. For instance, compare to Friday’s level, the market now sees the Fed funds ending the year at 4.39%, 8bps higher on the day. The 2y note also climbed by a similar amount edging back above 4% while the 10y Note gained 7bps to 3.50%. Earlier in Europe, 10y Bunds climbed 3bps to 2.32% while Italian BTPS gained 5bps to 4.24%. On Sunday, Governing Council member Klaas Knot said the ECB needs to continue raising interest rates amid a “too high” underlying inflation rate

In economic news, the NY Fed Consumer Expectations survey revealed short-term inflation expectations of consumers easing somewhat during April . Consumers see prices rising 4.45% over the next 12 months, following an expected rise of 4.75% in March. Inflation expectations at three-year horizon rose to 2.89% from 2.78%. Notably too, perceptions of current credit access and expectations of future availability of credit were mostly unchanged.

German industrial production slumped 3.4% m/m in March, led by the auto sector, following the strong gains in the first two months of the year. A weak run of data for March raises the chance of downward revisions to the early estimate of GDP (which was flat q/q) and may mean the economy didn’t in fact escape recession over Q4/Q1. Furthermore, the weak end to the quarter sets up a weak base effect for Q2.

Moving onto FX, the USD is little changed in index terms with modest moves seen amongst the majors. At 101.39, the DXY index continues to trade close to the bottom edge of its recent trading range, the index is very close to its 100.8 mid-April low, a support level that may including we, are watching. A clear break would set up further downside pressure on the USD. The Euro is 0.14% softer but starts the new day holding on to the 1.10 handle while USD/JPY continues to pivot around the ¥135 mark.

Pro-growth currencies are showing modest gains against the USD with NZD leading the charge. The Kiwi is up 0.83% to 0.6345 and after trading to an overnight high of 0,6804 the AUD is up 0.5% over the past 24 hours to 0.6781 . Reflecting an improvement on the global growth outlook commodities also had a good start to the new week with iron ore up 6.7%, copper +1% and oil prices up between 1.9 and 2.15%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect growth in the global economy to remain subdued out to 2026.

Insight

Financial institution issuance has recorded another high-volume year in the Australian dollar bond market, with some key questions still to explore ahead of a fast start in 2025.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.