Online retail sales growth slowed in May following a fairly strong April

Insight

Despite a big jump in confidence in the Conference Board numbers for the US, there’s not much optimism in the markets today.

https://soundcloud.com/user-291029717/no-more-heroes-anymore?in=user-291029717/sets/the-morning-call

Dear Mr. President, Come take a walk with me, Let’s pretend we’re just two people and, You’re not better than me, I’d like to ask you some questions if we can speak honestly – Pink

US stocks have traded with a more cautious tone following two days of gains either side of the weekend.

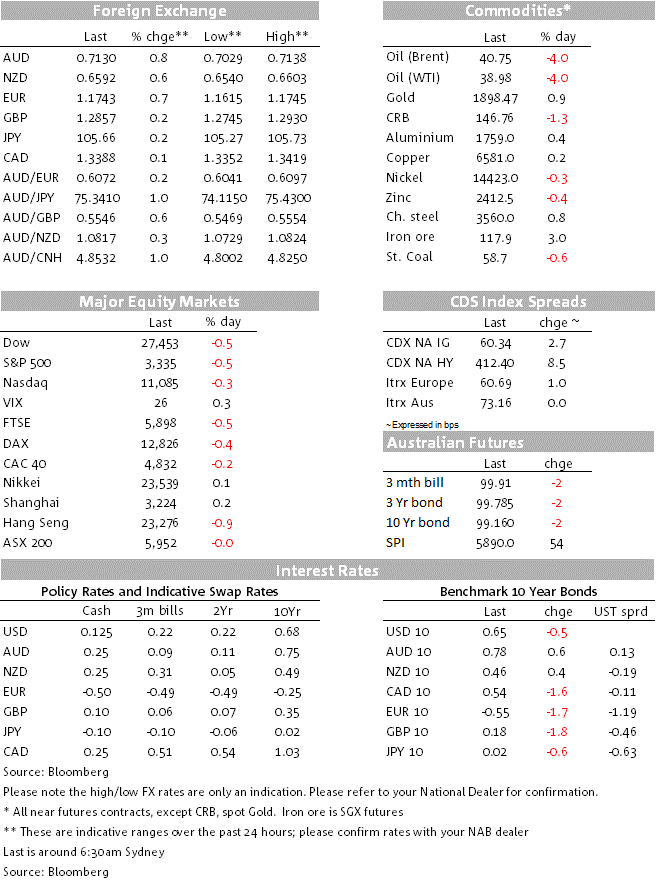

The Dow and S&P 500 have both finished down 0.5% and the NASDAQ 0.3% lower. The S&P loss puts the month to date change at -4.7%, which from an AUD FX perspective could – though may well not – mean some AUD supply tonight and tomorrow due to hedge-related rebalancing from asset managers finding themselves slightly over-hedged on their US equity holdings.

The USD is modestly softer (e.g. the BBDXY index -0.22% and the narrower DXY -0.42%) showing the negative correlation between US equity performance and FX – on a day to-day basis at least – not to be completely perfect. Indeed the normally highly risk sensitive AUD is the best performing G10 currency of the last 24 hours, currently +0.8% on this time yesterday at around 0.7130.

The market technicians among us will have a keen eye on tonight’s month-end closes among other indicators, and where a close nearer to 0.7150 would temper some of the otherwise outright bearishness that this month’s price action has instilled.

The Scandinavia currencies have done almost as well as AUD, the NOK despite a drop of as much as 4% in crude oil prices, seemingly on demand concerns after major independent traders noted at a conference that would it take 18-24 months to get demand back to pre-COVID levels.

Yesterday’s tabling of a $2.2tn fiscal support package hasn’t drawn any favourable response as yet from the Republican side even though House speaker Nancy Pelosi and US Treasury secretary Steve Mnuchin are said to still be talking. Trump’s economic advisor Kudlow said that the true cost of the Democrat’s package is more like $2.6 trillion and about one-third of it looks like not being strictly tied to the pandemic. Talks are expected to continue but confidence in a deal before the pre-election Congressional recess is not running high.

US consumer confidence rose by the most in 17 years, blasting up well above market expectations to reach 101.8 on the Conference Board measure, seemingly reflecting the impact of the pre-September surge in stock prices and bigger than expected drop in the unemployment rate last month. Confidence remains well below pre-COVID levels and while the jobs hard-to-get versus jobs-plentiful spread nudged higher, this labour market indicator remained consistent with a sluggish recovery.

With the advanced release on the goods side rising to a record $82.9b, driven by higher imports. To a large extent this reflects payback for the sharp drop in imports on supply chain disruptions during the early months of the pandemic, but is hardly a good look in terms of the ‘success’ of the US tariff actions against China in reducing US trade deficits. Let’s see if that comes up in the debate this morning.

Euro-area economic confidence rose for a fifth consecutive month and by more than expected, albeit remaining well below pre-COVID levels. German CPI fell by 0.4% y/y, the lowest rate in more than five-years, boosting the case for further monetary and fiscal stimulus. This failed to harm the EUR however, up 0.7% and one of the better performing g10 currencies.

GBP has slightly extended beginning week gains on optimism a EU-UK trade deal can be struck in time, at the same time Bank of England Governor Bailey has kept the market guessing on whether a negative rates policy will be adopted. He noted the groundwork currently being done, but continued to indicate that it would just be another possible tool in the toolbox. He said he can’t easily put a date on the end of the negative rate review – it depends on technical factors to work through regarding implementation – which gives the impression that the tool wouldn’t be ready for some time yet.

The UK has reportedly submitted draft legal text to the EU on five areas (fisheries, level playing field – which includes state aid, law enforcement, energy/mobility and social security coordination). EU reaction to this is now awaited in coming days.

In the meantime, Irish Foreign Minister Simon Coveney said he saw a “good chance” of a trade deal, striking his most upbeat note over the prospects for an accord since a controversy erupted over Prime Minister Boris Johnson’s plan to re-write the Brexit withdrawal agreement. “The obstacles are not insurmountable” to an agreement before the end of the year, Coveney said in an interview with Bloomberg Television on Tuesday. “Not agreeing a trade deal would be an enormous failure. The stakes are very high here.”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.