Online retail sales growth slowed in May following a fairly strong April

Insight

Market sentiment has done a complete U-turn.

https://soundcloud.com/user-291029717/no-time-no-place-no-momentum?in=user-291029717/sets/the-morning-call

The positive US-China trade vibes that have of late been largely responsible for the updraft in risk markets, higher bond yields, support for the RMB and with that AUD and NZD, have been stifled in the last few hours by a Reuters report saying that a Trump-Xi meeting to sign a trade deal could be delayed until December, as discussions continue over the terms of a deal and the venue for its ceremonial signing.

Reuters reports that the US is considering scheduling a Trump-XI meeting to sign an interim deal in London in early December after the NATO Summit, but that no decision has yet been made.

One could take the view that by not committing to meet the original deadline for signing the so-called Phase 1 agreement (i.e. the since-cancelled Nov 17-18th APAC meeting) it gives more time for a somewhat more comprehensive agreement to be thrashed out – potentially involving a US commitment to wind back some existing tariffs. But markets have understandably jumped the other way, exhibiting a slight loss of confidence that anything more substantial than an agreement not to further lift tariffs, in return for some increase in US agricultural purchases, can be agreed by way of an initial deal. The latter we would argue, was already fully priced into markets more than a week ago.

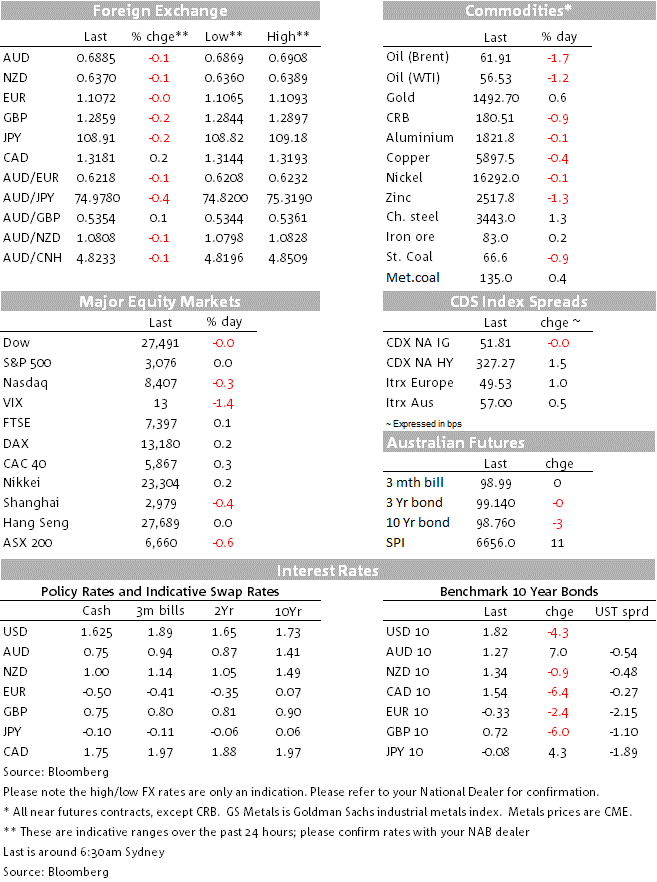

We had seen some support for the EUR, Bund yields and Eurozone equity markets from first much better than expected Germany Factory Orders data (+1.3% m/m versus 0.1% expected) quickly followed by final EZ PMI data, showing services at 52.2 versus the 51.18 ‘flash’ estimate and the Composite reading up to 50.6 from 50.2. Within this, it was upward revisions to Germany’s initial services readings that drove the improvement (51.6 from 51.2) while Italy – for whom no flash estimates are published – came in stronger than expected at 52.2 up from 51.4 for services (51.0 expected) and 50.8 up from 50.6 last time for the Composite reading (50.2 expected).

US data that has attracted a bit of attention overnight was the unexpected 0.3% fall in non-farm productivity in Q3 (+0.9% expected) and which means that the Unit Labor Cost jumped by 3.6%, not the 2.2% expected. The ‘gig economy’ is being blamed for this, (perhaps a lot more Uber drivers on the streets idling around looking for a fare?). The data is noisy and prone to revision, despite which it didn’t go completely unnoticed.

Overnight Fed speak came from NY President John Williams (one of the three FOMC big hitters along with Powell and Clarida) who said monetary policy is now slightly accommodative (the same as Kashkari yesterday) and Chicago President Charles Evans, who said the three rate cuts this year have left the economy in a good place

US Congressional Democrats have announced the first public hearings next week in the impeachment enquiry into President Trump.

US equities are coming into the last hour of trade very narrowly mixed but with lower oil prices (Brent -$1.14) weighing heavily on the energy sub-sector of the S&P500 (-2.2%).

Bond markets have seen US Treasuries supported both by the trade deal delay news and a strong 10-year Note auction, with the weighted average yield coming in 1bp below the prevailing 1pm secondary market yield. 10s are just over 4bps down on the day at 1.82%, 2s -2bps at 1.61%. Earlier in the night, European bond yields finished 2-3bp lower on average, save for a bigger 6bp drop in 10-year gilt yields ahead of the Bank of England tonight (amid some expectation of a ‘dovish hold’).

A notable mover has been USD/CNH, which after spending time below 7.00 since Tuesday, popped back up above 7.01 on the trade news. This in turn pulled AUD/USD down from above 0.6890 to briefly below 0.6870, having earlier spent the evening idling between 0.6890 and 0.6900. In general, it’s the commodity currencies faring worse over the past 24 hours (CAD, AUD and NZD down by 0.1-0.2%) along with the GBP (-0.23% and currently bottom of the G10 scoreboard, with JPY and SEK at the top (+0.2-3%), the former on lower US treasury yields.

A YouGov poll for Sky News has the Conservatives at 36%, ahead of Labour at 25%, Liberal Democrats at 17% and the Brexit Party at 11%. The probability of an outright Tory majority on Dec 12th continues to flit between plus and minus 50% in the bookies.

Australia’s trade surplus is forecast to shrink in September. NAB forecasts a lower surplus of $5.1b (consensus also $5.1b) reflecting a further fall in export values of 2%, driven by a fall in iron ore volumes and commodity prices. In contrast, total imports are largely unchanged as stronger fuel imports are offset by a pull-back in non-monetary gold.

Other than trade, just the AiG Performance of Construction PMI on the AU/NZ calendar

The Bank of England meeting should be a non-event (political opinion polls and what they say about the prospect for a Tory majorly or hung parliament being the main source of UK market volatility at present).

Germany publishes industrial production, expected at -0.4% m/m but after yesterday’s much better than expected factory data, the whisper number will be higher.

The US data calendar is empty.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.